Yahoo Finance

Yahoo Finance Is Ergomed (LON:ERGO) A Risky Investment?

Some say volatility, rather than debt, is the best way to think about risk as an investor, but Warren Buffett famously said that 'Volatility is far from synonymous with risk. So it might be obvious that you need to consider debt, when you think about how risky any given stock is, because too much debt can sink a company. As with many other companies Ergomed plc (LON:ERGO) makes use of debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Part and parcel of capitalism is the process of 'creative destruction' where failed businesses are mercilessly liquidated by their bankers. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. By replacing dilution, though, debt can be an extremely good tool for businesses that need capital to invest in growth at high rates of return. The first step when considering a company's debt levels is to consider its cash and debt together.

View our latest analysis for Ergomed

How Much Debt Does Ergomed Carry?

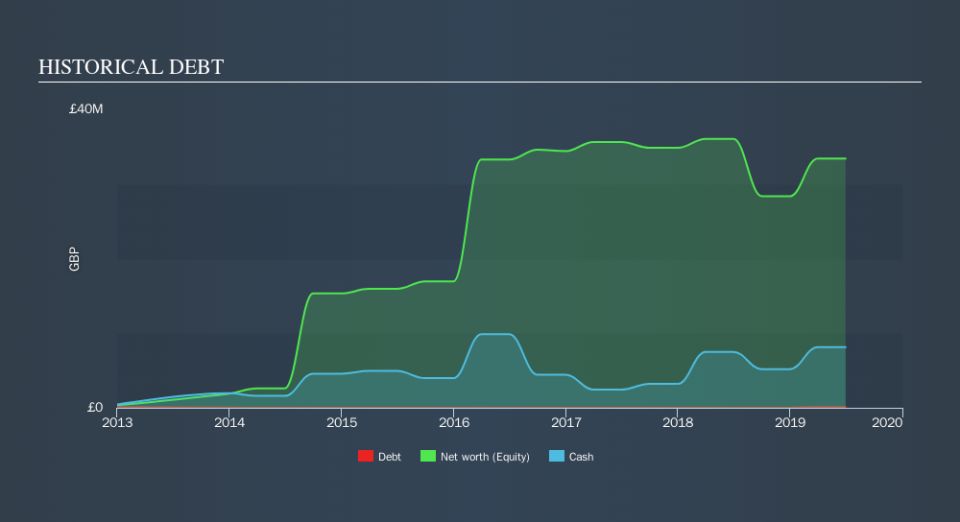

As you can see below, at the end of June 2019, Ergomed had UK£99.0k of debt, up from UK£12.0k a year ago. Click the image for more detail. But it also has UK£8.13m in cash to offset that, meaning it has UK£8.03m net cash.

How Strong Is Ergomed's Balance Sheet?

Zooming in on the latest balance sheet data, we can see that Ergomed had liabilities of UK£14.8m due within 12 months and liabilities of UK£5.27m due beyond that. On the other hand, it had cash of UK£8.13m and UK£17.2m worth of receivables due within a year. So it actually has UK£5.21m more liquid assets than total liabilities.

This short term liquidity is a sign that Ergomed could probably pay off its debt with ease, as its balance sheet is far from stretched. Succinctly put, Ergomed boasts net cash, so it's fair to say it does not have a heavy debt load!

Although Ergomed made a loss at the EBIT level, last year, it was also good to see that it generated UK£5.7m in EBIT over the last twelve months. There's no doubt that we learn most about debt from the balance sheet. But ultimately the future profitability of the business will decide if Ergomed can strengthen its balance sheet over time. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. Ergomed may have net cash on the balance sheet, but it is still interesting to look at how well the business converts its earnings before interest and tax (EBIT) to free cash flow, because that will influence both its need for, and its capacity to manage debt. In the last year, Ergomed's free cash flow amounted to 21% of its EBIT, less than we'd expect. That weak cash conversion makes it more difficult to handle indebtedness.

Summing up

While it is always sensible to investigate a company's debt, in this case Ergomed has UK£8.03m in net cash and a decent-looking balance sheet. So we are not troubled with Ergomed's debt use. Of course, we wouldn't say no to the extra confidence that we'd gain if we knew that Ergomed insiders have been buying shares: if you're on the same wavelength, you can find out if insiders are buying by clicking this link.

If you're interested in investing in businesses that can grow profits without the burden of debt, then check out this free list of growing businesses that have net cash on the balance sheet.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.