Yahoo Finance

Yahoo Finance Ericsson (ERIC) Focuses on Core Businesses, Risks Remain

On May 10, we issued an updated research report on telecom services provider, Ericsson ERIC.

Ericsson is pursuing three main areas, namely core business growth, targeted growth and cost & efficiency to maximize growth. In terms of “core business growth”, it is focusing on deployment of 4G and fostering 5G. The company constantly seeks to seize business opportunities as operators shift toward 4G deployments and prepare grounds for the forthcoming 5G revolution. Secondly, the company plans to focus more intently on software sales and recurring business that complements its thriving Professional Services business in terms of “targeted growth” investments. With such concerted efforts, Ericsson expects to be better-equipped to address the varied needs of its customer segments and tap on market opportunities for faster growth.

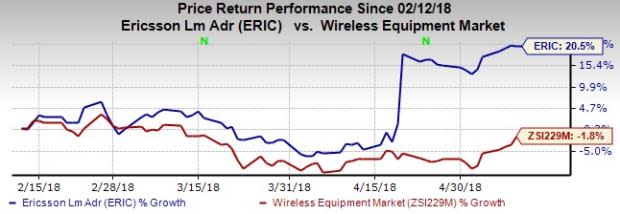

To help it realize its goals, Ericsson has entered into collaboration with communications technology behemoth Cisco Systems, Inc. (CSCO), inking a global business and technology partnership to create futuristic networks. The Ericsson-Cisco duo extends routing, data center, networking, cloud, mobility, management and control, and global services capabilities to clients across the globe. It appears that this collaboration is shaping up well, with the companies jointly procuring more than 60 deals in IP (routing and transport) and services. At present, they enjoy 250 active customer engagements and remain optimistic that these will lead to award wins, going forward. Over the past three months, Ericsson has outperformed the industry with an average return of 20.5% against a decline of 1.8% for the latter.

Ericsson is focusing on 5G system development and has undertaken many notable endeavors to position itself for market leadership on 5G. The company believes that standardization of 5G is the cornerstone for digitization of industries as well as broadband. Moreover, Ericsson foresees mainstream 4G offerings giving way to 5G technology in the future. Meanwhile, the impending deployment of 5G networks in 2020 is expected to boost the adoption of IoT devices with technologies like network slicing gaining more prominence. The Ericsson Mobility report suggests that almost 90% of smartphone subscriptions are on 3G and 4G networks today but they will be upgraded to 5G networks when it becomes commercially available in 2020. Ericsson has already introduced pre-standard 5G networks. 5G will accelerate the digital transformation in many industries, enabling new use cases in areas such as IoT, automation, transport and Big Data. The report also forecasts 550 million 5G subscriptions in 2022, with North America expected to lead the way. Such positive industry trends are expected to boost the company’s long-term growth.

However, Ericsson’s business is prone to be impacted by the political and economical uncertainties in its operating countries. Particularly, uncertainty in the financial markets, reduced consumer telecom spending and delayed auctions of spectrums pose significant threats for Ericsson. The company’s revenues and gross margins continue to take a beating from adverse industry trends. Persistent low investments in mobile broadband in certain markets and lower managed services sales have harmed sales of Networks segment while lower legacy product sales have hurt IT & Cloud revenues. Lower IPR licensing revenues and an unfavorable mix between coverage & capacity and services are adding to the company’s concerns. Moreover, it has been facing investment headwinds in network developments in Mediterranean, Northern Europe and Central Asia (especially Russia) regions as well as in Latin America and the Middle East. In addition, the ongoing uncertainty surrounding the Brexit referendum may prove to be a spoiler for Ericsson, stalling major investment decisions.

Soft mobile broadband demand and challenging macroeconomic conditions in the emerging markets are acting as deterrents to major investments by telecom equipment behemoths, and this has significantly dented Ericsson’s performance. These factors manifested in the company’s poor sales. Overall, it expects the negative industry trends and business mix in mobile broadband to prevail this year as well. Europe and Latin America — the markets with the biggest impact — are likely to have an increasingly challenging investment environment. The China market will likely continue to contract due to declining LTE investments, even as North America enjoys a positive momentum. Further, spectrum crunch has become a major issue in the U.S. telecom industry that has a saturated wireless market. The situation has worsened with the growing popularity of iPhone and Android smartphones as well as rising online mobile video streaming, cloud computing and video conferencing services. In addition, the company’s cash flow could be materially hurt by market and customer project adjustments. Though the company is working diligently to improve the situation, tangible results are yet to materialize.

Nevertheless, we remain impressed with the inherent growth potential of this Zacks Rank #3 (Hold) stock. Some better-ranked stocks in the industry are Motorola Solutions, Inc. MSI, PCTEL, Inc. PCTI and SITO Mobile, Ltd. SITO, each carrying a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Motorola has a long-term earnings growth expectation of 8%. It surpassed estimates in each of the trailing four quarters with an average positive earnings surprise of 12.1%.

PCTEL has surpassed estimates twice in the trailing four quarters with an average positive earnings surprise of 17.9%.

SITO Mobile has a long-term earnings growth expectation of 25%.

Looking for Stocks with Skyrocketing Upside?

Zacks has just released a Special Report on the booming investment opportunities of legal marijuana.

Ignited by new referendums and legislation, this industry is expected to blast from an already robust $6.7 billion to $20.2 billion in 2021. Early investors stand to make a killing, but you have to be ready to act and know just where to look.

See the pot trades we're targeting>>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Ericsson (ERIC) : Free Stock Analysis Report

Motorola Solutions, Inc. (MSI) : Free Stock Analysis Report

PC-Tel, Inc. (PCTI) : Free Stock Analysis Report

SITO Mobile, Ltd. (SITO) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research