Euronext Amsterdam Showcases Basic-Fit And Two More Growth Stocks With High Insider Ownership

As global markets navigate through a period marked by rising trade tensions and shifts in investment trends, the Netherlands' stock market remains a focal point for investors seeking stability and growth potential. Amidst these conditions, companies like Basic-Fit with high insider ownership stand out as they often exemplify strong commitment and confidence from those closest to the business. In today's investment climate, stocks with substantial insider ownership can be particularly appealing. This characteristic suggests that company leaders are willing to align their interests closely with those of their shareholders, potentially leading to more prudent management and robust growth trajectories.

Top 5 Growth Companies With High Insider Ownership In The Netherlands

Name | Insider Ownership | Earnings Growth |

BenevolentAI (ENXTAM:BAI) | 27.8% | 62.8% |

Ebusco Holding (ENXTAM:EBUS) | 33.2% | 114.0% |

Envipco Holding (ENXTAM:ENVI) | 36.7% | 68.9% |

MotorK (ENXTAM:MTRK) | 35.8% | 105.8% |

Basic-Fit (ENXTAM:BFIT) | 12% | 65.2% |

PostNL (ENXTAM:PNL) | 35.8% | 23.9% |

Here's a peek at a few of the choices from the screener.

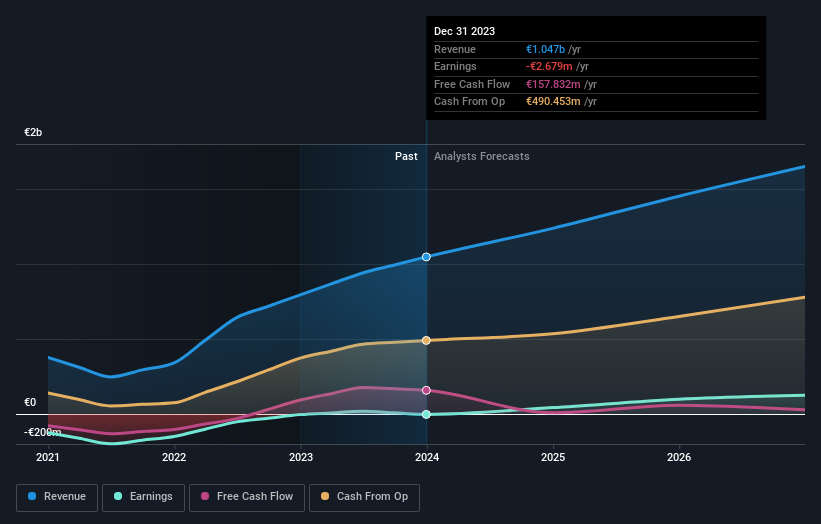

Basic-Fit

Simply Wall St Growth Rating: ★★★★★☆

Overview: Basic-Fit N.V. operates a chain of fitness clubs across Europe, with a market capitalization of approximately €1.45 billion.

Operations: The company generates revenue primarily from its fitness clubs in two key regions: the Benelux countries (€479.04 million) and a combined segment of France, Spain, and Germany (€568.21 million).

Insider Ownership: 12%

Earnings Growth Forecast: 65.2% p.a.

Basic-Fit, positioned in the Netherlands, is on a trajectory to profitability within the next three years, outpacing average market growth expectations. With earnings expected to surge by 65.22% annually and revenue projected to increase at 14.8% per year—faster than the Dutch market rate of 10.1%—the company shows promising financial health. Insider activities reinforce this positive outlook as more shares have been purchased than sold recently, though not in significant volumes, highlighting sustained confidence from those closest to the company's operations. Analysts anticipate a potential price increase of 49.7%, suggesting an undervaluation based on current trajectories.

Delve into the full analysis future growth report here for a deeper understanding of Basic-Fit.

Upon reviewing our latest valuation report, Basic-Fit's share price might be too optimistic.

MotorK

Simply Wall St Growth Rating: ★★★★★☆

Overview: MotorK plc operates as a provider of software-as-a-service solutions tailored for the automotive retail industry across Italy, Spain, France, Germany, and the Benelux Union, with a market capitalization of approximately €267.12 million.

Operations: The company generates its revenue primarily from the software and programming segment, which amounted to €42.94 million.

Insider Ownership: 35.8%

Earnings Growth Forecast: 105.8% p.a.

MotorK, a growth-oriented company in the Netherlands, is forecasted to outperform the Dutch market with an expected revenue growth of 24% per year. Despite recent shareholder dilution, the company's earnings are projected to increase significantly by 105.85% annually. MotorK is anticipated to achieve profitability within three years, a rate considered above average compared to market expectations. However, it currently lacks profitability and has seen no substantial insider trading activity in the past three months. The appointment of Zoltan Gelencser as CFO could bring fresh strategic insights from his extensive global finance experience.

Click here and access our complete growth analysis report to understand the dynamics of MotorK.

The valuation report we've compiled suggests that MotorK's current price could be inflated.

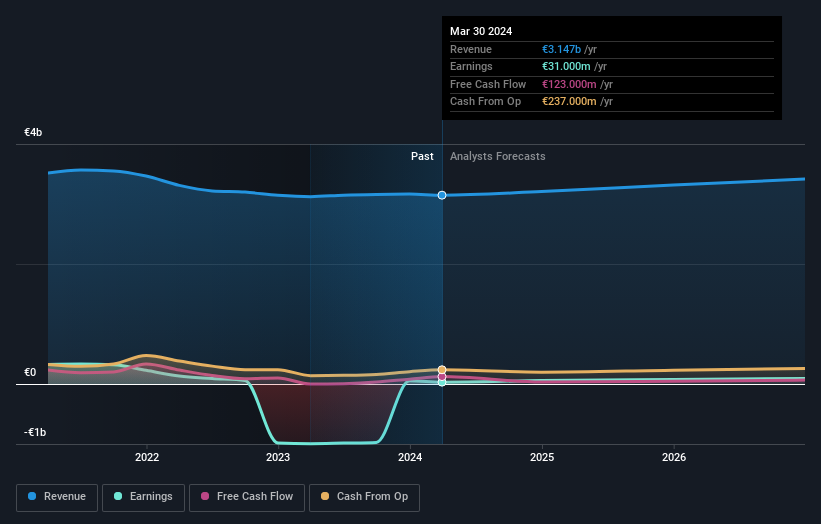

PostNL

Simply Wall St Growth Rating: ★★★★☆☆

Overview: PostNL N.V. offers postal and logistics services across the Netherlands, Europe, and globally, with a market capitalization of approximately €0.70 billion.

Operations: The company's revenue is generated from two main segments: Packages (€2.25 billion) and Mail in The Netherlands (€1.35 billion).

Insider Ownership: 35.8%

Earnings Growth Forecast: 23.9% p.a.

PostNL, a Dutch company with high insider ownership, is trading at 51.8% below its estimated fair value, indicating potential undervaluation. Despite a recent net loss of €20 million in Q1 2024 and unstable dividend history, PostNL's earnings are expected to grow significantly by 23.9% annually over the next three years. However, it has a high debt level and its revenue growth forecast of 3.3% per year lags behind the broader Dutch market's growth rate of 10.1%.

Get an in-depth perspective on PostNL's performance by reading our analyst estimates report here.

Our valuation report unveils the possibility PostNL's shares may be trading at a discount.

Taking Advantage

Unlock our comprehensive list of 6 Fast Growing Euronext Amsterdam Companies With High Insider Ownership by clicking here.

Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

Unlock the power of informed investing with Simply Wall St, your free guide to navigating stock markets worldwide.

Interested In Other Possibilities?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Find companies with promising cash flow potential yet trading below their fair value.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.The analysis only considers stock directly held by insiders. It does not include indirectly owned stock through other vehicles such as corporate and/or trust entities. All forecast revenue and earnings growth rates quoted are in terms of annualised (per annum) growth rates over 1-3 years.

Companies discussed in this article include ENXTAM:BFIT ENXTAM:MTRK and ENXTAM:PNL.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com