Yahoo Finance

Yahoo Finance Euronext Paris Stocks Estimated To Be Undervalued In June 2024

As of June 2024, the French stock market is showing signs of resilience, with the CAC 40 Index recently climbing by 1.67% amid easing political uncertainties and a more favorable outlook for monetary policy across Europe. This buoyant environment may present opportunities for investors to identify undervalued stocks poised for potential growth. In such a market climate, understanding the fundamentals that contribute to a stock being considered undervalued—such as strong company financials relative to its current share price or sectoral prospects outpacing market expectations—becomes crucial.

Top 10 Undervalued Stocks Based On Cash Flows In France

Name | Current Price | Fair Value (Est) | Discount (Est) |

Airbus (ENXTPA:AIR) | €134.78 | €239.99 | 43.8% |

Vente-Unique.com (ENXTPA:ALVU) | €15.35 | €29.87 | 48.6% |

Kaufman & Broad (ENXTPA:KOF) | €27.75 | €53.02 | 47.7% |

Lectra (ENXTPA:LSS) | €27.95 | €43.20 | 35.3% |

Wavestone (ENXTPA:WAVE) | €52.30 | €88.74 | 41.1% |

MEMSCAP (ENXTPA:MEMS) | €5.41 | €8.58 | 37% |

Vivendi (ENXTPA:VIV) | €9.846 | €15.57 | 36.8% |

Tikehau Capital (ENXTPA:TKO) | €21.60 | €32.44 | 33.4% |

Thales (ENXTPA:HO) | €155.05 | €254.94 | 39.2% |

Groupe Airwell Société anonyme (ENXTPA:ALAIR) | €3.86 | €6.74 | 42.8% |

We'll examine a selection from our screener results

Antin Infrastructure Partners SAS

Overview: Antin Infrastructure Partners SAS is a private equity firm focused on infrastructure investments, with a market capitalization of approximately €2.07 billion.

Operations: The firm generates revenue primarily through its asset management segment, totaling approximately €282.87 million.

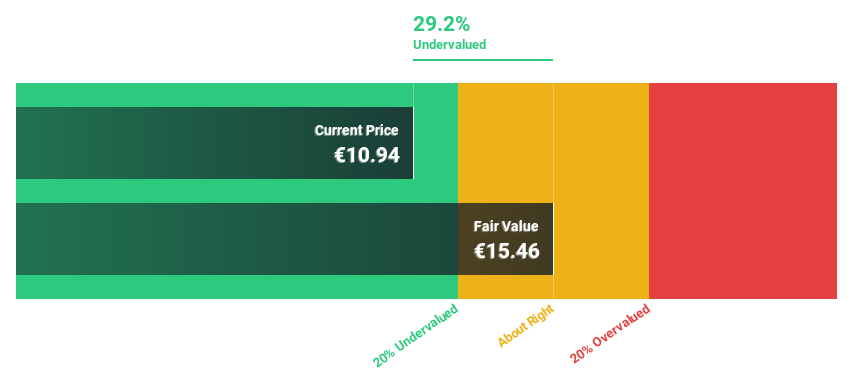

Estimated Discount To Fair Value: 25.9%

Antin Infrastructure Partners SAS, trading at €11.54, is perceived as undervalued with a fair value estimate of €15.57 based on discounted cash flows, indicating a 25.9% undervaluation. Despite recent dividend distributions totaling €0.71 per share for the year, the dividend coverage by earnings and cash flows remains weak. The company's revenue and earnings are expected to grow annually by 12.7% and 25.9%, respectively, outpacing the French market projections significantly in both areas; however, shareholder dilution over the past year poses a concern for potential investors.

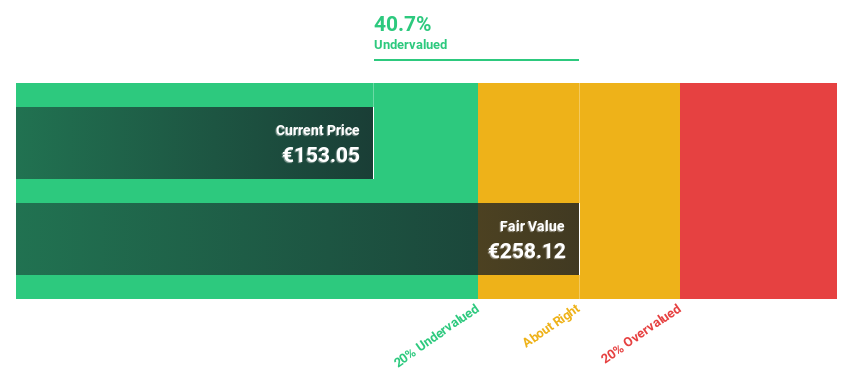

Thales

Overview: Thales S.A. is a global company offering solutions in defense, aerospace, digital identity and security, and transportation sectors, with a market capitalization of approximately €32.04 billion.

Operations: Thales generates revenue from four primary segments: Aerospace (€5.34 billion), Digital Identity & Security (€3.42 billion), and Defense & Security excluding Digital I&S (€10.18 billion).

Estimated Discount To Fair Value: 39.2%

Thales, priced at €155.05, is currently valued below its estimated fair value of €254.94, suggesting a significant undervaluation based on discounted cash flow analysis. Recent strategic alliances and product launches underline its active expansion in global markets and sectors like cybersecurity and satellite-based surveillance, potentially enhancing future cash flows. However, it carries high debt levels and has shown an unstable dividend track record, which could concern risk-averse investors. Despite these challenges, Thales's revenue is expected to grow by 6.3% annually, slightly above the French market forecast of 5.8%.

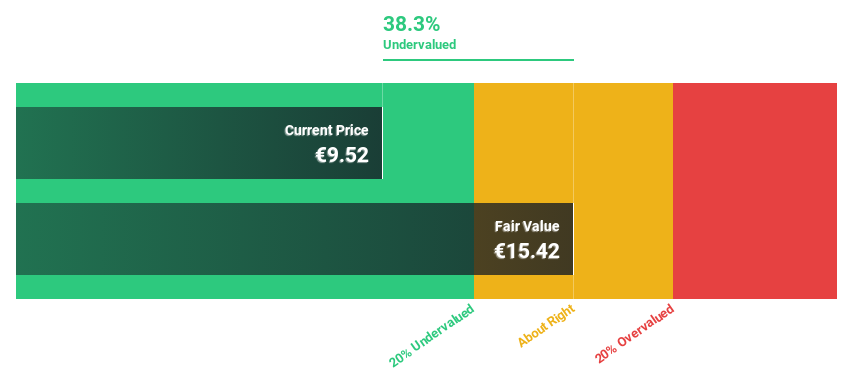

Vivendi

Overview: Vivendi SE is a France-based entertainment, media, and communication company with operations spanning Europe, the Americas, Asia/Oceania, and Africa, boasting a market capitalization of €10.09 billion.

Operations: The company's revenue is primarily generated through six segments: Canal + Group (€6.06 billion), Havas Group (€2.87 billion), Lagardère (€0.67 billion), Gameloft (€0.31 billion), Prisma Media (€0.31 billion), and Vivendi Village (€0.18 billion).

Estimated Discount To Fair Value: 36.8%

Vivendi, trading at €9.85, appears undervalued with its price significantly below the fair value of €15.57 determined by discounted cash flow analysis. It recently reported a substantial revenue increase to €4.27 billion in Q1 2024, up from €2.29 billion the previous year, signaling strong sales momentum. Despite this positive trend, its Return on Equity is expected to remain low at 6%, and it has an unstable dividend history with a recent affirmation of a €0.25 per share payout for fiscal 2023. Analysts forecast Vivendi's earnings to grow by 29.26% annually, outpacing the French market projection of 11% growth per year.

Next Steps

Explore the 14 names from our Undervalued Euronext Paris Stocks Based On Cash Flows screener here.

Shareholder in one or more of these companies? Ensure you're never caught off-guard by adding your portfolio in Simply Wall St for timely alerts on significant stock developments.

Take control of your financial future using Simply Wall St, offering free, in-depth knowledge of international markets to every investor.

Ready To Venture Into Other Investment Styles?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include ENXTPA:ANTIN ENXTPA:HO and ENXTPA:VIV.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com