Yahoo Finance

Yahoo Finance Evercore (NYSE:EVR) Is Increasing Its Dividend To US$0.72

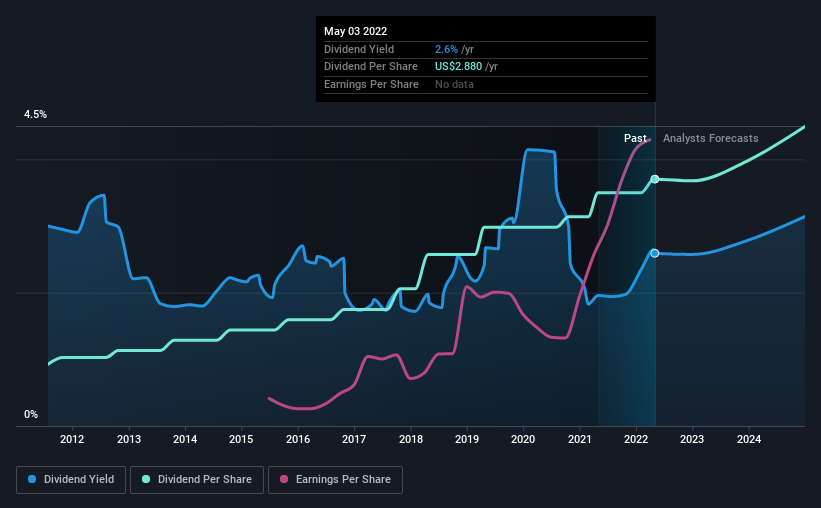

Evercore Inc. (NYSE:EVR) will increase its dividend on the 10th of June to US$0.72. The announced payment will take the dividend yield to 2.5%, which is in line with the average for the industry.

Check out our latest analysis for Evercore

Evercore's Payment Has Solid Earnings Coverage

Unless the payments are sustainable, the dividend yield doesn't mean too much. However, Evercore's earnings easily cover the dividend. This means that most of what the business earns is being used to help it grow.

EPS is set to fall by 36.2% over the next 12 months. Assuming the dividend continues along recent trends, we believe the payout ratio could be 30%, which we are pretty comfortable with and we think is feasible on an earnings basis.

Evercore Has A Solid Track Record

The company has been paying a dividend for a long time, and it has been quite stable which gives us confidence in the future dividend potential. Since 2012, the dividend has gone from US$0.72 to US$2.88. This works out to be a compound annual growth rate (CAGR) of approximately 15% a year over that time. So, dividends have been growing pretty quickly, and even more impressively, they haven't experienced any notable falls during this period.

The Dividend Looks Likely To Grow

Investors could be attracted to the stock based on the quality of its payment history. We are encouraged to see that Evercore has grown earnings per share at 29% per year over the past five years. Earnings have been growing rapidly, and with a low payout ratio we think that the company could turn out to be a great dividend stock.

We Really Like Evercore's Dividend

In summary, it is always positive to see the dividend being increased, and we are particularly pleased with its overall sustainability. The distributions are easily covered by earnings, and there is plenty of cash being generated as well. If earnings do fall over the next 12 months, the dividend could be buffeted a little bit, but we don't think it should cause too much of a problem in the long term. All in all, this checks a lot of the boxes we look for when choosing an income stock.

Investors generally tend to favour companies with a consistent, stable dividend policy as opposed to those operating an irregular one. However, there are other things to consider for investors when analysing stock performance. Case in point: We've spotted 2 warning signs for Evercore (of which 1 is concerning!) you should know about. Is Evercore not quite the opportunity you were looking for? Why not check out our selection of top dividend stocks.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.