Yahoo Finance

Yahoo Finance Expectations for Goldman Sachs (NYSE:GS) are low, but so is the Valuation

This article originally appeared on Simply Wall St News.

Shares of The Goldman Sachs Group, Inc. ( NYSE:GS ) have fallen sharply this week following the release of the group’s fourth quarter results. The results were weaker than expected and the market was surprised at the large increase in compensation expenses. While the company’s outlook appears subdued, the low valuation may be offering long term investors an opportunity.

Fourth quarter results highlights:

GAAP EPS of $10.81 down 10.5% year on year and well below the $11.93 consensus estimate

Trading revenue of $4 bln was lower than expected ($4.2 bln)

Compensation and benefits expenses at $17.7 bln, up 33% for the year and higher than expected.

Check out our latest analysis for Goldman Sachs Group

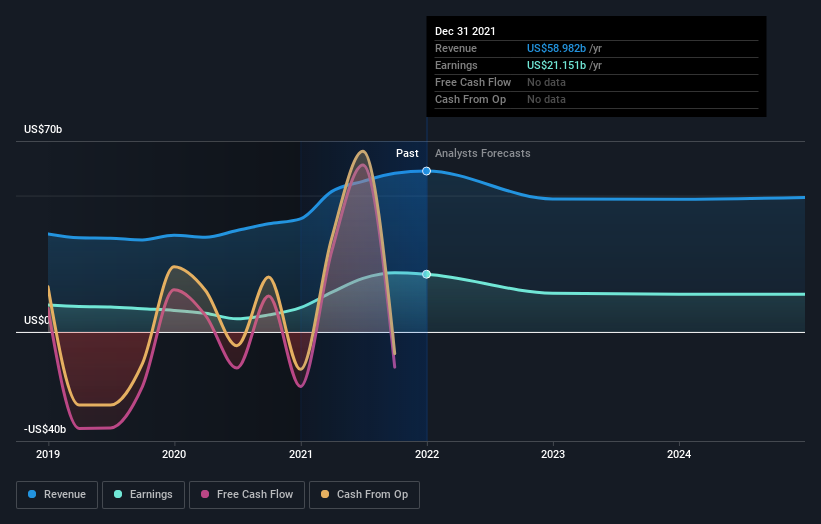

What kind of growth will Goldman Sachs Group generate?

Goldman Sachs has delivered impressive EPS growth over the last two years, but as the following chart illustrates, analysts are not expecting this growth to continue. In fact, EPS are expected to fall by 19% over the next few years. Analysts don’t always get it right, but it’s still worth knowing what they are expecting.

What is Goldman Sachs Group worth?

Goldman Sachs is currently trading on a price-to-earnings ratio of 5.48x, well below the industry average of 15.16x, and the market average of 16.9x. So, while expectations for growth are low, the price is also reflecting very low expectations.

In addition, Goldman’s P/E ratio is the lowest it has been since 2010. For most of the last decade it has been in the low teens, but it has been as high as 30.

Some investors believe the price-to-book ratio is more appropriate for banks. In Goldman’s case, the P/B ratio is now 1.1x, compared to an industry average of 37x and a market average of 2.1x. The P/B ratio is not as low historically as the P/E ratio, but is well below the recent highs.

Finally we can look at the Simply Wall Street fair value estimate for Goldman Sachs . This estimate is calculated by discounting expected cash flows, so it’s sensitive to consensus cash flow estimates and the discount rate used. The estimate for fair value is now $688, which implies the share is 49% undervalued. So, while earnings are expected to fall, the share may still be undervalued.

Is this an opportunity?

Goldman Sachs has seen a dramatic increase in profitability over the last two years. This set of results was disappointing compared to the last few quarters, but EPS are still well ahead of where they were two years ago.

The immediate outlook doesn’t look very exciting, as is reflected by the current valuation. On the other hand, if the outlook was better it’s unlikely the valuation would be this low. So, for long term investors wanting to invest in a leading investment banking group, this may be an opportunity.

This article is not intended to be a comprehensive analysis on Goldman Sachs, but rather to highlight the current valuation and outlook. If you are interested in understanding the company at a deeper level, take a look at our Goldman Sachs Group page on Simply Wall St.

If you are no longer interested in Goldman Sachs Group, you can use our free platform to see our list of over 50 other stocks with a high growth potential.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com

Simply Wall St analyst Richard Bowman and Simply Wall St have no position in any of the companies mentioned. This article is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.