Exploring Three Stocks Estimated to Trade Below Intrinsic Value With Discounts Up to 31%

As global markets exhibit a mix of promising advances and nuanced economic signals, investors are keenly watching for opportunities that might be undervalued in such a complex environment. Identifying stocks trading below their intrinsic value could be particularly compelling now, offering potential for appreciation as market conditions evolve.

Top 10 Undervalued Stocks Based On Cash Flows

Name | Current Price | Fair Value (Est) | Discount (Est) |

Beijing Kawin Technology Share-Holding (SHSE:688687) | CN¥22.86 | CN¥45.50 | 49.8% |

Nusco (BIT:NUS) | €0.962 | €1.91 | 49.6% |

Calnex Solutions (AIM:CLX) | £0.485 | £0.97 | 49.9% |

Radici Pietro Industries & Brands (BIT:RAD) | €1.10 | €2.19 | 49.8% |

Compagnia dei Caraibi (BIT:TIME) | €1.02 | €2.03 | 49.7% |

Power and Water Utility Company for Jubail and Yanbu (SASE:2083) | SAR62.70 | SAR124.34 | 49.6% |

Terveystalo Oyj (HLSE:TTALO) | €9.50 | €18.98 | 49.9% |

Tilray Brands (NasdaqGS:TLRY) | US$1.93 | US$3.85 | 49.9% |

BlueNord (OB:BNOR) | NOK519.00 | NOK1029.60 | 49.6% |

TAL Education Group (NYSE:TAL) | US$10.00 | US$19.91 | 49.8% |

Here we highlight a subset of our preferred stocks from the screener.

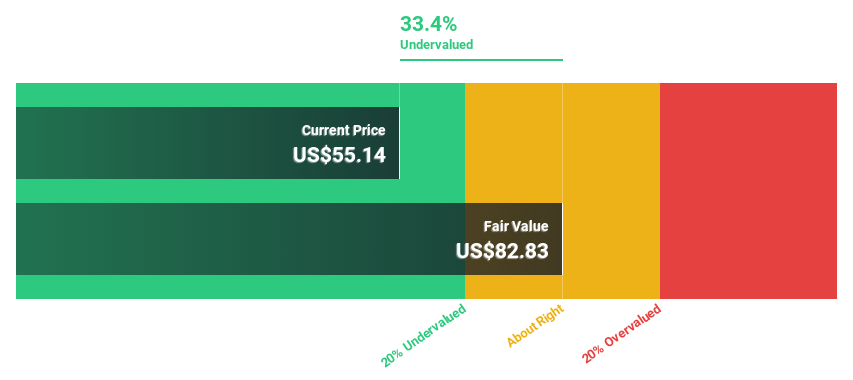

DocuSign

Overview: DocuSign, Inc. offers electronic signature solutions both in the United States and internationally, with a market capitalization of approximately $11.69 billion.

Operations: The company generates its revenue primarily from its software and programming segment, totaling $2.81 billion.

Estimated Discount To Fair Value: 30.9%

DocuSign, currently priced at US$56.9, is significantly undervalued based on discounted cash flow analysis with an estimated fair value of US$82.32, reflecting a 30.9% discount. Despite slower revenue growth projections at 5.8% annually compared to the broader US market's 8.7%, DocuSign's earnings are expected to outpace the market with a robust annual increase of 27%. The company's strategic partnerships and product enhancements, such as the recent integration with Sandbox Banking’s Glyue™ and upcoming Docusign Connector for SAP Ariba solutions, underscore its commitment to expanding its technological capabilities and market reach.

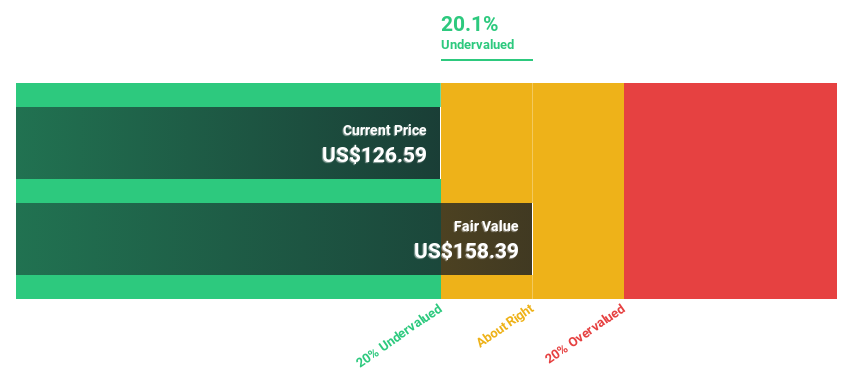

Repligen

Overview: Repligen Corporation specializes in developing and commercializing bioprocessing technologies and systems for biological drug manufacturing across North America, Europe, the Asia Pacific, and internationally, with a market cap of approximately $6.85 billion.

Operations: The company generates its revenue primarily from the medical products segment, which brought in $607.45 million.

Estimated Discount To Fair Value: 21.9%

Repligen, trading at US$135, is considered undervalued by over 20% against a fair value estimate of US$172.81 based on discounted cash flow analysis. Despite recent executive changes and a significant product launch with Ecolab, concerns linger due to a notable drop in net profit margin from 21.6% to 2.4% year-over-year and lower-than-expected Q1 earnings. However, the company's revenue growth forecast at 13.7% annually outpaces the US market prediction of 8.7%, with earnings expected to grow by an impressive 38.29% annually.

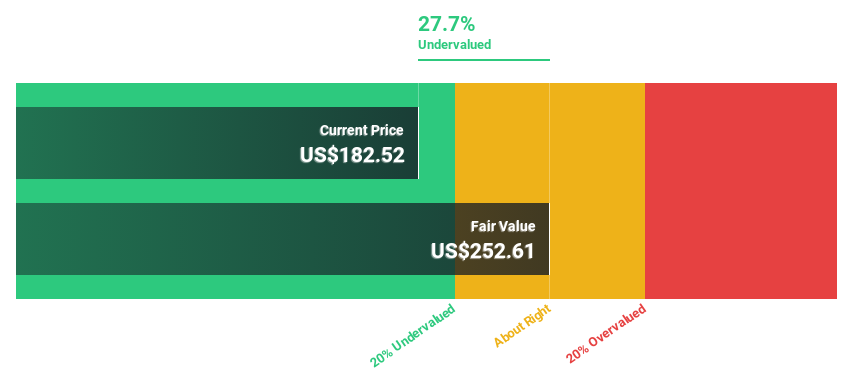

Zscaler

Overview: Zscaler, Inc. is a global cloud security company with a market capitalization of approximately $30.91 billion.

Operations: The company generates $2.03 billion from subscription services to its cloud platform and related support services.

Estimated Discount To Fair Value: 31%

Zscaler, currently priced at US$203.12, is perceived as undervalued, trading 31% below its estimated fair value of US$294.34 based on discounted cash flow analysis. Despite recent insider selling and shareholder dilution over the past year, Zscaler's financial outlook appears robust with an anticipated profitability within three years and a projected annual profit growth of 50.92%. Revenue growth is expected at 18.1% per year, surpassing the U.S market average of 8.7%, supported by strategic partnerships and expanding service offerings like the recent collaboration with Wipro for cybersecurity enhancements.

Make It Happen

Discover the full array of 958 Undervalued Stocks Based On Cash Flows right here.

Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

Join a community of smart investors by using Simply Wall St. It's free and delivers expert-level analysis on worldwide markets.

Want To Explore Some Alternatives?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include NasdaqGS:DOCU NasdaqGS:RGEN and NasdaqGS:ZS.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com