Yahoo Finance

Yahoo Finance Can Favorable Trends Aid Diageo (DEO) Despite Cost Woes?

Diageo plc DEO has been gaining from effective marketing and exceptional commercial execution, which boosted the fiscal 2022 results. The company has been benefitting from a sustained recovery in the on-trade channel, strong consumer demand in the off-trade channel and market share gains. Diageo expects to invest strongly in marketing and innovation, and leverage its revenue growth management capabilities, including strategic pricing actions. This is likely to support the company’s momentum in the near and long terms.

However, continued inflationary pressures and currency headwinds are concerning. Higher commodity costs, particularly agave, energy expenses and supply disruptions, have been key headwinds. As a substantial portion of Diageo’s business comes from international operations, exchange rate fluctuations have been hampering its sales.

The Zacks Consensus Estimate for the Zacks Rank #3 (Hold) company’s current financial year’s sales and earnings suggests growth of 15.7% and 7.7%, respectively, from the year-ago period’s reported numbers.

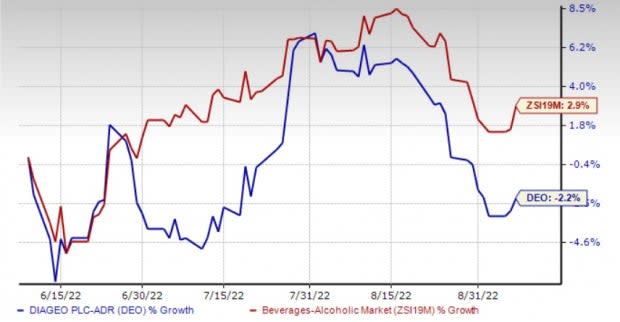

Shares of Diageo have lost 2.2% in the past three months against the industry’s growth of 2.9%.

Image Source: Zacks Investment Research

Factors to Aid Growth

Diageo is anticipated to retain the strong business momentum on continued premiumization efforts and favorable industry trends, particularly in the spirits category. The company’s organic net sales were up 21.4% year over year in fiscal 2022. Recovery in the on-trade channel in North America and Europe, and the partial recovery in Travel Retail have been aiding price/mix. The company’s positive mix is also the result of the robust performance of super-premium-plus brands, particularly scotch, tequila and Chinese white spirits.

The company’s largest market, North America, witnessed sales growth of 17% in fiscal 2022, while organic sales were up 14%. This was driven by the recovery in on-trade, resilient consumer demand in the off-trade, market share gains and spirits taking a share of total beverage alcohol.

DEO’s margin trends were favorable in fiscal 2022, owing to its premiumization efforts, recovery in markets, pricing actions and supply productivity savings, which mostly offset the cost inflation. The company delivered £380 million of productivity savings in fiscal 2022, driven by COGS productivity and marketing effectiveness. The company’s operating profit improved 18.2% in fiscal 2022, driven by robust organic operating profit growth.

Although Diageo expects the operating environment to be challenging in fiscal 2023, it remains confident in the resilience of its business and its ability to navigate through the headwinds. The company is confident about the long-term growth potential of the total beverage alcohol sector and expects to expand its value share by 50% in the sector to 6% by 2030.

DEO is on track to deliver on its medium-term guidance for fiscal 2023-2025, wherein it targets organic sales growth of 5-7% and organic operating profit growth of 6-9%.

For fiscal 2023, the company expects net sales growth across North America, Europe and the Asia Pacific. However, the growth rate is likely to moderate from the fiscal 2022 level due to the robust on-trade recovery witnessed in fiscal 2022. It anticipates continued organic operating margin growth in fiscal 2023, driven by strong premiumization trends and operating leverage despite continued investment in marketing. It expects an effective interest rate of 3.5% for fiscal 2023.

Headwinds to Overcome

Diageo has been witnessing inflationary pressures, driven by higher commodity costs, particularly agave, energy expenses and supply disruptions. Although the company reported organic operating margin growth, it was partially offset by increased marketing investments, adverse category mix and inflationary pressures from agave.

In fiscal 2023, the company expects to invest continually in marketing and innovation, particularly in North America. Moreover, it expects continued impacts of rising inflationary pressures to partly hurt margins.

The company also remains susceptible to adverse currency rates. While the weakening of sterling against the U.S. dollar and some impacts of emerging market currencies look favorable, Diageo expects adverse currency impacts of hyperinflationary economies, primarily Turkey.

Stocks to Consider

We have highlighted some better-ranked stocks from the broader Consumer Staples space, namely Fomento Economico Mexicano FMX, Carlsberg CABGY and General Mills Inc. GIS.

Fomento Economico Mexicano, alias FEMSA, has exposure in various industries, including beverage, beer and retail, which gives it an edge over its competitors. It currently has a Zacks Rank #2 (Buy). FMX has a trailing four-quarter earnings surprise of 18.9%, on average. Shares of FMX have lost 9.1% in the past three months.

You can see the complete list of today's Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for FEMSA’s current financial-year sales suggests growth of 11.3% from the year-ago period's reported figures. FMX has an expected EPS growth rate of 11.4% for three-five years.

Carlsberg produces and sells beer and other beverage products in Denmark. It currently has a Zacks Rank #2. Shares of CABGY have gained 3% in the past three months.

The Zacks Consensus Estimate for Carlsberg’s current financial-year sales suggests growth of 8.8%, while the same for earnings per share indicates a decline of 9.8% from the year-ago period’s reported figures. CABGY has an expected EPS growth rate of 9.1% for three-five years.

General Mills is a global manufacturer and marketer of branded consumer foods sold through retail stores. It currently has a Zacks Rank #2. The company has an expected EPS growth rate of 7.5% for three-five years. Shares of GIS have rallied 12.3% in the past three months.

The Zacks Consensus Estimate for General Mills’ current financial-year sales and earnings per share suggests growth of 1.9% and 1.5%, respectively, from the year-ago period’s reported figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

General Mills, Inc. (GIS) : Free Stock Analysis Report

Fomento Economico Mexicano S.A.B. de C.V. (FMX) : Free Stock Analysis Report

Diageo plc (DEO) : Free Stock Analysis Report

Carlsberg AS (CABGY) : Free Stock Analysis Report

To read this article on Zacks.com click here.

Zacks Investment Research