Yahoo Finance

Yahoo Finance Four Insights on Crypto Liquidity From Binance US and FTX

The Takeaway

Trading fees are going to come down

Dinky coins matter to bitcoin liquidity

Market data is never reliable

Nothing in crypto is “institutional grade”

Fragmented markets are a salient feature of the crypto asset class. Nowhere else does a single asset trade across so many small pools of liquidity.

Bitcoin itself could be considered a thinly traded asset, and this market structure makes it difficult to agree upon a bitcoin price–let alone to prevent manipulation or move large amounts of the asset without paying slippage costs.

To get at the heart of this problem, CoinDesk Research’s webinar series brought in the chief executives of two young crypto exchanges. Catherine Coley is CEO of Binance US, the US arm of one of the largest crypto spot exchanges by liquidity and volume. Sam Bankman-Fried is CEO of Alameda Research, a quantitative trading firm based in Hong Kong that earlier this year started up FTX, a crypto derivatives exchange. Both exchanges have shown some fast early growth and attracted attention from crypto pundits and traders.

Related: Microsoft Collaboration News Fuels 50% Rally for Enjin’s Cryptocurrency

Here are four takeaways from our conversation with Sam and Catherine. Get the full presentation on CoinDesk’s YouTube channel (and embedded at the end of this article), and sign up for our next webinar, in which we’ll talk with two fund managers about whether bitcoin should be treated as an interest-earning asset.

1. RIP good times (for exchanges)

Ask anyone to list the top firms on Wall Street, and what names would you expect to hear? ICE, the firm that operates the NYSE, is an admirable company, but you’d be surprised to hear it named on that list.

In crypto, it’s exactly the opposite, Bankman-Fried pointed out during our conversation. Exchanges are the biggest, the deepest-pocketed and among the most influential crypto firms operating today. In part, that’s because bitcoin and ethereum aren’t firms. In part, it’s because of crypto’s immaturity: speculating on the speculative activity of others is the only use case that’s really been proven; it’s turtles, all the way down, as the old theological joke goes.

Crypto exchanges rule the roost because of their fee structure: 1 percent trading fees are typical, something you’d never see on a stock brokerage. (Discount firms like Schwab offer zero-commission trading, these days.) However, there are ways in which crypto’s fee structure is friendlier than other asset categories, Coley pointed out.

Related: Ethereum’s Top DEX Is Relaunching to Tap Istanbul’s Lower Gas Fees

“I blame and credit my experience on the FX desk for making me realize some of the largest money movers out there pay nothing,” she said. “Whereas myself when I was on my desk moving Hong Kong dollars in to US dollars for, say, Christmas gifts or travel, I was paying 8 percent…on a currency that’s pegged. That was hard to digest.”

Volume discounts also exist in crypto, but perhaps not to the same degree. Buying and holding so-called exchange tokens offers a sort of a loyalty program for traders looking for lower fees. Still, Coley said, for many, 1 percent fees are a barrier to entry. Exchanges are able to charge those rates today, perhaps due to FOMO (fear of missing out) or the novelty of the crypto asset category. Neither Bankman-Fried nor Coley expect those rates to last.

2. Bitcoin needs dogecoin

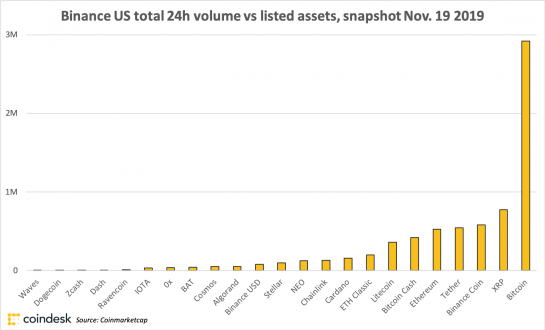

To attract order book depth both Binance US and FTX have added a long tail of thinly traded crypto assets.

Binance US began operations in September with seven markets and at the time of our webinar listed some two dozen. The chart above is just a 24-hour snapshot, but it shows how small some of these markets are by volume. Despite their diminutive size, they are an important driver of volume and liquidity into the larger markets on the exchange, both Coley and Bankman-Fried said.

It’s “Come for the shitcoins, stay for the bitcoin,” Bankman-Fried said.

Options for trading in smaller-cap crypto assets are limited, he said. An investor wishing to trade in them will incur the capital costs, time and risk of onboarding to a new exchange. In larger-cap crypto assets like bitcoin and ether, it’s harder to differentiate.

3. Believe nothing you hear, and only one half that you see

Recently, CoinDesk Research analyzed alleged bitcoin price manipulation, focusing on what is possible, or likely, when a relatively liquid market depends on a relatively illiquid market. FTX faces this problem from one side, as a derivatives market that relies on price data from less-liquid spot markets. Binance US faces it from the other, as a provider of price data to traders.

According to Bankman-Fried, there’s no easy way around it. Derivatives markets must build indexes with many component spot markets, because they are likely to be ingesting erroneous or manipulated price data from exchanges, and there is no way to filter the good from the bad. Prices move so unpredictably in bitcoin and other crypto asset markets that it is impossible to distinguish fake pricing data from real.

4. No, you may not have the keys to the car

Since 2017 and before then, bitcoin bagholders have been hyping the “institutional” capital that is waiting on the sidelines for…something. Custody. Derivatives. Trading on credit.

The truth is, bitcoin markets, and markets in any other crypto asset, are not ready to meet the expectations of institutional asset managers.

Bankman-Fried, whose firm Alameda Research acts as a market-maker on FTX and other exchanges, said he’s no longer surprised by the gaps in market structure he encounters when engaging with a new exchange. Some have low withdrawal limits; others have long withdrawal times. Others have risk checks that flag institutional accounts too frequently. Many, he said, have API rate limits of 10 queries per second, or less. That means on an exchange that lists 100 markets, it would take an institution 10 seconds just to find out its open orders.

Coley, from the other side of the table, agreed. “Seeing how institutions expect markets to behave, there’s a lot more that needs to be done,” she said.

For the full digest, listen to the episode on CoinDesk YouTube.

More

Register for the next CoinDesk Research webinar; on Dec. 18, we’ll talk about lending and staking with two managers at funds that are long bitcoin: Kyle Samani from Multicoin Capital and Jordan Clifford from Scalar Capital.

Get CoinDesk Research’s Institutional Crypto newsletter for weekly insights and charts.

Download our series of white papers, “Introduction to Crypto Investment,” covering issues like custody, fundamentals and bitcoin’s status as “digital gold.”