Yahoo Finance

Yahoo Finance UK records first July surplus in 15 years; FTSE 100 jumps back into positive territory

FTSE 100 pushes back into the green as the gloomy mood on stock markets begins to lift; European stocks also record strong early rises

Pound slips back below $1.29; UK records first July surplus since 2002

Doorstep lender Provident Financial has plummeted 63pc on the FTSE 100 after a triple whammy of a scrapped dividend, chief executive departure and warning of a full-year loss

BHS' former owner Dominic Chappell to be prosecuted by The Pensions Regulator for failing to provide information into an investigation into the sale of the closed retailer

Markets wrap: FTSE 100 snaps losing streak; pound drifts lower against stronger dollar

Global stock markets have rebounded sharply today as the risk aversion dogging equities faded away. With the dollar also advancing on the pound, the FTSE 100 snapped a three-day losing streak to finish 0.9pc higher thanks to a broad based rally.

The pick of the movements in London has been doorstep lender Provident Financial's incredible 66pc plummet after the triple whammy of a scrapped dividend, chief executive departure and full-year loss forecast. Elsewhere Tesco outstripping its rivals in the latest supermarket sales data lifted its shares 4.1pc while mining stocks were buoyed by robust base metal prices with copper rising to a three-year high.

On the currency markets, data from the ONS showing that the UK posted its first July surplus since 2002 and CBI figures indicating a strengthening manufacturing sector couldn't stop the pound drifting lower against a stronger dollar today. While sterling remains flat against the euro, it is finishing the day 0.6pc down against the greenback, trading at $1.2837.

Brent crude stabilises around $52 per barrel after OPEC meeting fails to impress traders

Brent crude has stabilised around the $52 per barrel mark this afternoon after the lack of major news from yesterday's OPEC meeting failed to impress traders, causing the price drift downwards once again.

CMC Markets analyst David Madden said this on OPEC's dwindling reputation in the oil market:

"The oil minister of Kuwait, Essam al-Marzouq stated they will talk about the possibility of extending the production cut beyond the end of March 2018. The oil cartel should not be ignored, but the group does not have the creditability it once did, as traders know they often say one thing, and do another."

Oil has stoked a bit of movement on the stock market as well today. London-listed producer Cairn Energy jumped 3.6pc today after it upped its recoverable reserves estimate at its offshore SNE field in Senegal from 473m barrels to 563m while Petrofac popped 2.1pc after it sold a 50pc stake in the Pánuco oil field to Schlumberger.

FTSE 100 rebounds into positive territory as risk aversion retreats

Markets are now closed in Europe and the FTSE 100 has rebounded into positive territory today, rallying 0.9pc, as risk aversion retreated on global stock markets. A quick round-up of today's action and the market report will follow shortly...

US markets lifted by fresh hopes of tax reform

Fresh hopes of US tax reforms are helping equities gain stateside this afternoon, according to IG's chief market analyst Chris Beauchamp.

He said this on today's play:

"One day down, one day up, and so on. This is the theme of August, with markets unable so far to establish a direction and stick with it. After losses yesterday the buyers have come back in, with fresh hope of moves on US tax reform apparently providing the catalyst for gains.

"Warm words from Senate leader McConnell on the debt ceiling are also helping to boost confidence. Perhaps this time we will see stock markets extend their gains into a second day; optimism surrounding Jackson Hole and potential comments on monetary policy from the dynamic duo of Draghi and Yellen could see Wednesday post a positive session as well."

Hostelworld back in the black as holidaymakers book by app

Travel bookings website Hostelworld swung back to profit in the first half of the year, helped by more holidaymakers booking shorter trips via their mobile phones.

The company said that even though the price of accommodation had risen, partly because of the fall in the value of sterling, it had seen the number of bookings rise by 11pc to 3.9m.

Chief executive Feargal Mooney said the number of nights per booking had dropped but that this had been balanced by the shift to mobile, which made up half of reservations in the six months to June 30.

Mobile customers “transact more frequently than other customers”, Mr Mooney said, which had been an important factor in helping the company’s adjusted profits, pushing them up 27pc to €12.9m (£11.8m).

Read Bradley Gerrard's full report here

Tech firms and copper miners lift US indices

After having a poor session yesterday, tech shares are helping to lift US indices this afternoon with the tech-heavy Nasdaq rebounding 0.9pc shortly after the opening bell in New York.

As in London, the mining stocks are also leading the way across the Atlantic with copper hitting a three-year high on hopes of stronger demand.

Over here, that rise has led to copper miner KAZ Minerals popping nearly 7pc on the FTSE 250 while blue-chip Antofagasta has risen 2.5pc with its strong interim results also giving the Chile-based firm a helping hand.

Antofagasta on a roll as copper prices surge

Chile-based miner Antofagasta believes copper’s good run is set to continue as it reported a jump in profits and a hiked dividend.

Iván Arriagada, chief executive, said the “outlook is favourable”, as copper expects to be in long-term demand for electrical wiring in houses, cars, and gadgets.

“We’re positive on where the copper market is going,” he said. “There will be volatility but the price is going in the right direction.”

Read Jon Yeomans' full report here

US markets preview

The stronger dollar following "unfavourable" economics data in Europe has helped to lift equities today, argues Henry Croft, research analyst at Accendo Markets.

He added:

"European equities are nicely positive this afternoon as a US dollar recovery aids the plethora of stocks across the region with foreign earnings.

"The rally for the global reserve currency follows a morning of unfavourable European macroeconomic data; a disappointing ZEW expectations survey print for Eurozone powerhouse Germany and an ominous forecast from the UK’s ONS that public borrowing will deepen have hurt the Euro and Sterling, respectively."

The quieter White House helped US stock indices snap their losing streak yesterday with European markets today taking their cue from the positive session over the Atlantic. US stock futures are pointing to a positive start there as well.

Spreadex analyst Connor Campbell provided this preview of this afternoon's action over in the US:

"Having briefly dipped below 21600 during yesterday’s trading the US index managed to recover by the end of the session, leaving it in line to re-cross 21700 with a 40 point rise after the bell.

"There isn’t a lot for the Dow to deal with this afternoon, so as long as the macro-issues that have plagued the markets in recent weeks remain in the background there isn’t much to disrupt its recovery."

Housebuilder Persimmon's profits soar by 30pc

FTSE 100 housebuilder Persimmon has reported a 30pc jump in profits in the first half of the year as it avoided the effects of a slowdown in the housing market.

Persimmon’s pre-tax profits rose 30pc to £457.5m in the six months ended June 30, while revenues were up 12pc to £1.66bn.

It built 556 new homes in the period, an increase in completions of 8pc to a total 7,794, as it made the business more efficient. Its average selling price rose 4pc to £213,262.

“The market remains confident,” said chief executive Jeff Fairburn. “Customer interest in our developments remains strong with encouraging levels of interest through both our websites and our sales outlets as we trade through the quieter summer weeks.

Shares nudged up 1pc following the results.

Read Sam Dean and Isabelle Fraser's full report here

Neil Woodford's portfolio takes a battering

Life comes at you fast, Neil Woodford edition... pic.twitter.com/eQsRwKpNSx

— Xavier MacDuff (@xvrmdf) August 22, 2017

Star fund manager Neil Woodford's day is going from bad to worse as, in addition to the huge 74pc fall at doorstep lender Provident Financial, his stakes in AA and Allied Minds are also taking a battering today.

The roadside rescuer is anchored to bottom of the FTSE 250 scoreboard, slipping 4.4pc, while intellectual property group Allied Minds has dived 8.1pc.

BHS owner Dominic Chappell prosecuted by Pensions Regulator

Dominic Chappell, the former bankrupt who bought BHS for £1, is to be prosecuted by The Pensions Regulator for failing to provide information related to his purchase of the now defunct retailer.

Mr Chappell has been summoned to appear at Brighton Magistrates Court on September 20 to face three charges of neglecting or refusing to provide information and documents without a reasonable excuse.

The Pensions Regulator is still pursuing Mr Chappell over the collapse of BHS, which left 20,000 BHS pensioners facing a pay cut and created 11,000 redundancies, after agreeing a £363m with Sir Philip Green to plug the retailer's deficit.

Read Ashley Armstrong's full report here

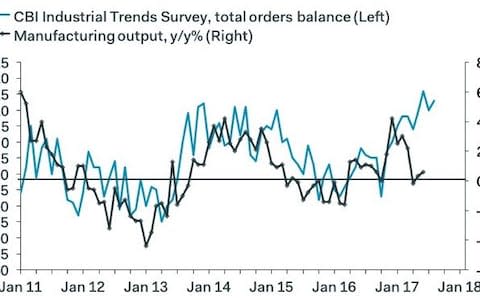

CBI manufacturing survey reaction: Can strong surveys translate to better output data?

Analysts are pointing out that today's robust CBI figures should be taken with a pinch of salt given that recently the hard output data has strayed from the trend shown in surveys such as today's.

Pantheon Macro commented that the survey's size and the way the data is collated could be to blame for the disparity:

"It’s possible that the survey’s small sample size of just 432 manufacturers is to blame for its inaccuracy. The CBI’s measure of orders also is derived from the number of manufacturers reporting if orders are above or below “normal”, which is not clearly defined.

"Firms also are asked to report order volumes, but we suspect that many think in terms of revenues, which in many cases have been boosted automatically by sterling’s depreciation.

The EY ITEM Club's chief economic advisor Howard Archer gave his thoughts on the sector's outlook:

"The outlook for manufacturing appears mixed with a promising export environment countered by challenging domestic conditions.

"On the positive side, a very competitive pound and improved global demand should buoy UK manufacturers competing in foreign markets. The weakened pound could also encourage some companies to switch to domestic sources for supplies, which could help manufacturers of intermediate products."

Lunchtime update: Provident Financial plunges 73pc as stock markets rebound

Provident Financial's colossal 73pc nosedive on the FTSE 100 this morning has made all the headlines but can't stop the blue-chip index rebounding firmly into positive territory.

The doorstep lender was ruthlessly punished after its latest interim results contained the triple whammy of a scrapped dividend, chief executive departure and shock forecast of a full-year loss.

At the other end, Tesco has jumped 3.5pc after its sale growth outstripped its UK rivals as budget supermarkets Aldi and Lidl continue to close the gap while mining heavyweight BHP Billiton has advanced 3pc following its full-year results, in which it bowed to pressure from activist investor Elliott Advisors and announced the sale of its US shale assets.

Despite the two UK economic releases this morning beating expectations, the pound has dipped 0.3pc against the dollar, trading at $1.2827, but remains flat against the euro. Analysts are pinning this morning's fall on Brexit-related jitters with EU chief Brexit negotiator Michel Barnier's goading tweets overnight ratcheting up the tension further at the negotiating table.

Here's the current state of play in Europe:

FTSE 100: +0.66pc

DAX: +0.61pc

CAC 40: +0.44pc

IBEX: +0.25pc

UK manufacturing demand remained strong in August, says CBI

Both total order books and export order books were strong in August. #CBI_ITShttps://t.co/m53aToSWoQpic.twitter.com/7r9RU8oolU

— CBI Economics (@CBI_Economics) August 22, 2017

Demand for UK manufacturing beat expectations in August, according to the CBI's latest industrial trends survey, with order books remaining strong thanks to exporters still feeling the benefit from a lower pound.

Some 30pc of manufacturers reported that order books were above normal while 17pc said they were below below, leaving a balance of +13pc, above expectations of a +8pc reading. The CBI added that strong and broad based output growth is expected to continue into the next quarter.

Anna Leach, CBI Head of Economic Intelligence, said:

"After a brief pause last month, expectations for selling prices have rebounded, indicating that the squeeze on consumers is set to persist. We expect CPI (Consumer Price Index) to top out at around 3% towards the end of this year and remain close to that level during 2018, as the effect of the weak pound continues to feed through."

BHS' former owner Dominic Chappell to be prosecuted

BHS' former owner Dominic Chappell will be prosecuted by The Pensions Regulator for failing to provide information requested during its investigation into the sale of the closed retailer.

The former bankrupt bought BHS for £1 in 2015 before it collapsed into administration in April 2016, leaving behind a £571m pension deficit.

The Pensions Regulator said this in its statement just a few moments ago:

TPR is prosecuting Mr Chappell for failing to comply with three notices issued under Section 72 of the Pensions Act 2004. The notices requiring information were issued to Mr Chappell on 26 April 2016, 13 May 2016 and 20 February 2017.

He has been summonsed to appear at Brighton Magistrates’ Court on 20 September 2017 to face three charges of neglecting or refusing to provide information and documents, without a reasonable excuse, when required to do so under section 72 of the Pensions Act 2004, contrary to section 77(1) of that Act."

Mike Ashley increases Debenhams stake to more than 20pc

Sports Direct boss Mike Ashley has increased his stake in Debenhams to more than 20pc.

In a statement to the stock market, Debenhams said Mr Ashley now holds 21pc of shares, giving him more than 10pc of voting rights in the company.

Sports Direct’s interest in Debenhams was first revealed in early 2014 and he has been steadily increasing his stake this year.

The increase of its holdings in the struggling department store chain follows Mr Ashley’s decision to snap up a stake of more than 25pc in video game retailer Game Digital last month.

Read Sam Dean's full report here

FTSE 100 holds gains; Provident on course for lowest share price since 2000

The FTSE 100 has held on to today's rebound thanks to the waning risk-off mood with European indices lifted by some bargain hunting this morning, according to CMC Markets analyst David Madden.

He commented:

"Traders adopt a risk-on strategy this morning even though the standoff between the US and North Korea is still bubbling away in the background.

"The shakedown in European equity markets yesterday has encouraged bargain hunting today. European indices have been in decline for a few months now, and today’s move higher hasn’t changed the outlook.

Some bargain buys may be lifting the blue-chip indices in Europe but I'm not sure the cut price sale on Provident Financial is enticing many buyers. The stock is now on course to close at its lowest share price since 2000.

Profit alert this morning results in Provident Financial 2019 bonds falling by 20 points, yield is now 10.6%. pic.twitter.com/ptiUEzTryH

— Bond Vigilantes (@bondvigilantes) August 22, 2017

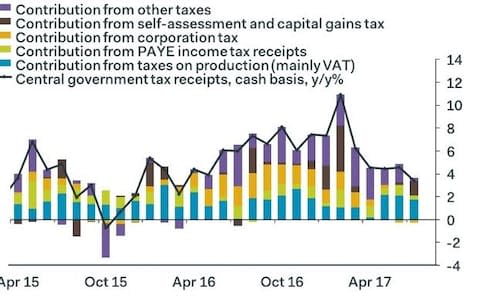

Public sector borrowing reaction: Pound continues drift downwards; slowing tax receipts highlight economy's fragility

Today's public sector net borrowing surplus hasn't been able to shift the momentum on the currency markets with the pound continuing to drift downwards against the dollar. It's currently trading at $1.2841, close to a one-month low against the greenback.

Pantheon Macro commented that today's borrowing figures are not a sign that the economy is in rude health and that instead slowing growth in tax receipts highlights the economy's fragility.

Its UK economist Samuel Tombs explained:

"Growth in receipts will slow sharply at the end of this fiscal year, because the bumper batch of SA receipts collected in January and February 2017, due to prior tax changes, will not be repeated.

"The OBR also likely will revise down its very optimistic forecasts for wage growth in the Autumn Budget, boosting the borrowing forecast in future years. As such, we continue to doubt that the Chancellor will pare back the fiscal consolidation planned for the coming years."

Here's what's driven the change in UK public sector borrowing so far this financial year. pic.twitter.com/d46wPMtsax

— Rupert Seggins (@Rupert_Seggins) August 22, 2017

Public sector borrowing reaction: Due to one-off factors

Today's much improved borrowing figures were mainly "due to one-off factors", according to Capital Economics' UK economist Ruth Gregory.

Economists had forecast a £1bn deficit in today's figures and the surplus is the UK's first in a July in 15 years.

Ms Gregory explained that we shouldn't get too carried away as figures for the first few months of the year are based on a "significant amount of forecast data".

She added:

"Some one-off effects distorted the annual comparison in July, as self-assessment receipts were boosted by the July 31st deadline falling on a Monday this year, but Sunday in 2016, meaning that some receipts were recorded in August last year.

"What’s more, cumulative borrowing in the first four months of the fiscal year at £22.8bn was still some 9% higher than the £20.9bn seen last year, with the OBR expecting a further deterioration later in the fiscal year.

"As such, despite July’s strength the Chancellor may still find that he has little scope for any easing back on the planned fiscal squeeze in his November Budget.

Public sector borrowing key takeaways

First July surplus for UK public sector finances since 2002 but run rate of borrowing still ahead of FY 2016/17 at £22.8bn YTD pic.twitter.com/09cyw1VhPa

— Simon French (@shjfrench) August 22, 2017

Public sector net borrowing recorded a £0.2bn surplus in July, the first July surplus since 2002.

July's surplus was much better than the £1bn deficit forecast.

Borrowing increased by £1.9bn to £22.8bn in the current financial year to date (April-July), when compared with the same period in 2016.

The Office for Budget Responsibility forecast that borrowing will reach £58.3bn for the financial year ending March 2018.

UK records first public sector July surplus since 2002

£22.8bn UK public sector net borrowing exc. public sector banks in April-July 2017, up £1.9bn on 2016 https://t.co/ifGjmYvKECpic.twitter.com/0i47ywD0f5

— Fraser Munro (@FraserMunroPSF) August 22, 2017

Public sector borrowing recorded a surplus of £0.2bn in July, its first July surplus since 2002. Reaction on the currency markets has been limited, however, the pound rising slightly to £1.2958, a 0.4pc fall for the session.

BHP Billiton board bow to activist investor pressure

Mining heavweights Antofagasta and BHP Billiton are pulling up the FTSE 100 most this morning after reporting their latest figures to the market.

Chilean copper miner Antofagasta has jumped 4.5pc in early trading after reporting that revenues have enjoyed a 42pc increase while BHP Billiton has popped 3.6pc after swinging back to a profit.

The dual-listed miner also said that it will sell its US shale portfolio, a key demand of activist investor shareholder Elliott Advisors.

The spin-off will be seen as a "capitulation by the board, which had previously argued that the division formed a core part of the group's operations", said Nicholas Hyett, an analyst at Hargreaves Lansdown.

He added:

"While that volte face may attract headlines, management’s strategy elsewhere seems to be going smoothly and delivering results.

"The focus on cost control at BHP’s already very low cost assets, means cash generation is soaring now commodity prices have turned. Net debt is tumbling, and as that falls towards more sustainable levels it will free up cash for other uses."

Provident Financial another Woodford pick to plunge in valuation

There were some hints that something of this nature was on the horizon for Provident Financial after its surprise profit warning in June sent shares sliding 18pc but I'm sure even those hedge funds that piled in cash against the company couldn't have foreseen a share price crash quite this large.

It appears that Provident's home credit division is the main issue with the company now expecting the department to record a pre-exceptional loss of between £80m to £120m.

Another interesting sidenote is that this is just the latest of star fund manager Neil Woodford's picks to have plunged of late with AA and AstraZeneca also suffering large drops recently.

Pharma firm AstraZeneca dropped 15pc in one session in July after revealing a setback in its key lung cancer drug trial while roadside rescuer AA plunged 14pc earlier this month following the sacking of chief executive Bob Mackenzie for a "Clarkson" moment.

It never rains but it pours.

#ProvidentFinancial a £3.11 Billion market cap specialist UK lender is down ~60% this morning! Canary in the coal mine? #UK#Debt#Bustpic.twitter.com/1icb0aAKHy

— SOLZHENITSYN (@SOLZ_ZYN) August 22, 2017

Provident Financial crashes 59pc after warning of a full-year loss

Not much Divine Providence for Provident Financial today...

— Jasper Lawler (@jasperlawler) August 22, 2017

It's hard to start any other place but Provident Financial this morning after its incredible share price crash.

The doorstep lender's valuation has been slashed in half in less than an hour after it said that it now expects a full-year loss, it ditched its interim dividend (it also indicated that a full-year dividend was unlikely) and chief executive Peter Crook stepped down.

Hedge funds have been circling Provident waiting for a slip with AQR, Systematica and Lansdowne Partners all holding large short positions in the company. Shorting, or borrowing a company's shares to sell and buy again when they have fallen to pocket the difference, is essentially a bet against a company and that bet has paid off big this morning.

Another Woodford favourite Provident Financial down 60% this morning as CEO quits & divi is withdrawn. So, does he sell, stick or twist $PFG

— Red Knight (@redknighttrader) August 22, 2017

Agenda: FTSE 100 jumps back into positive territory; borrowing figures expected to significantly improve

The FTSE 100 has jumped back into positive territory this morning as improving sessions in Asia and the US indicate that the gloomy mood hanging over stock markets appears to have lifted.

Corporate results are lighting up the UK's benchmark index early on with housebuilder Persimmon climbing 2.9pc on a 30pc increase in pre-tax profit in its first half results and dual-listed miner BHP Billiton, which reported at the open in Melbourne last night, rising 1.9pc after making key concessions to its activist investor shareholder Elliott Advisors.

It hasn't been all sunshine on the corporate calendar this morning, however, as at the other end doorstep lender Provident Financial has plummeted an incredible 48pc after forecasting a full-year loss, its chief executive stepped down and it scrapped its dividend.

A quick look at markets: Mild risk appetite recovery lifts global stocks as low vol & little news flow mean markets will likely trend higher pic.twitter.com/uGmp4DNTYK

— Holger Zschaepitz (@Schuldensuehner) August 22, 2017

Ahead of the UK public sector borrowing figures due at 9.30am this morning, the pound has slipped back below $1.29 against the dollar. The ONS data is expected to show borrowing increased by £1bn last month, a significant improvement on June's rise.

The other highlight, August's CBI industrial order expectations figure, will drop at 11am and is expected to slow slightly from the previous month's bumper showing.

Interim results: AFI Development, John Wood Group, Persimmon, Cairn Energy, Empresaria Group, Antofagasta

AGM: Puma VCT 10

Economics: Public sector net borrowing (UK), CBI industrial order expectations (UK), Consumer confidence (EU)