Yahoo Finance

Yahoo Finance Getting In Cheap On Idorsia Ltd (VTX:IDIA) Might Be Difficult

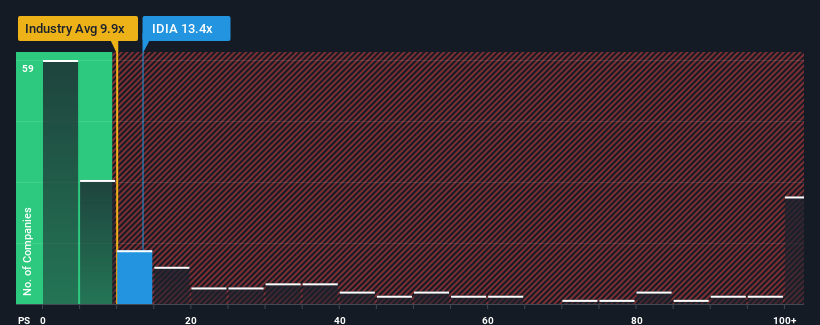

Idorsia Ltd's (VTX:IDIA) price-to-sales (or "P/S") ratio of 13.4x may look like a poor investment opportunity when you consider close to half the companies in the Biotechs industry in Switzerland have P/S ratios below 2.7x. Although, it's not wise to just take the P/S at face value as there may be an explanation why it's so lofty.

Check out our latest analysis for Idorsia

How Has Idorsia Performed Recently?

With revenue growth that's inferior to most other companies of late, Idorsia has been relatively sluggish. Perhaps the market is expecting future revenue performance to undergo a reversal of fortunes, which has elevated the P/S ratio. If not, then existing shareholders may be very nervous about the viability of the share price.

If you'd like to see what analysts are forecasting going forward, you should check out our free report on Idorsia.

Is There Enough Revenue Growth Forecasted For Idorsia?

The only time you'd be truly comfortable seeing a P/S as steep as Idorsia's is when the company's growth is on track to outshine the industry decidedly.

Retrospectively, the last year delivered an exceptional 235% gain to the company's top line. Spectacularly, three year revenue growth has ballooned by several orders of magnitude, thanks in part to the last 12 months of revenue growth. Accordingly, shareholders would have been over the moon with those medium-term rates of revenue growth.

Looking ahead now, revenue is anticipated to climb by 80% each year during the coming three years according to the eleven analysts following the company. That's shaping up to be materially higher than the 62% per annum growth forecast for the broader industry.

With this in mind, it's not hard to understand why Idorsia's P/S is high relative to its industry peers. Apparently shareholders aren't keen to offload something that is potentially eyeing a more prosperous future.

What We Can Learn From Idorsia's P/S?

Generally, our preference is to limit the use of the price-to-sales ratio to establishing what the market thinks about the overall health of a company.

Our look into Idorsia shows that its P/S ratio remains high on the merit of its strong future revenues. It appears that shareholders are confident in the company's future revenues, which is propping up the P/S. Unless these conditions change, they will continue to provide strong support to the share price.

And what about other risks? Every company has them, and we've spotted 4 warning signs for Idorsia (of which 2 can't be ignored!) you should know about.

Of course, profitable companies with a history of great earnings growth are generally safer bets. So you may wish to see this free collection of other companies that have reasonable P/E ratios and have grown earnings strongly.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here