Yahoo Finance

Yahoo Finance

Global Agricultural Tractors Market to 2027 - Size, Share & Industry Trends Analysis Report

Global Agricultural Tractors Market

Dublin, June 15, 2022 (GLOBE NEWSWIRE) -- The "Global Agricultural Tractors Market Size, Share & Industry Trends Analysis Report By Driveline Type, By Engine Power, By Regional Outlook and Forecast, 2021-2027" report has been added to ResearchAndMarkets.com's offering.

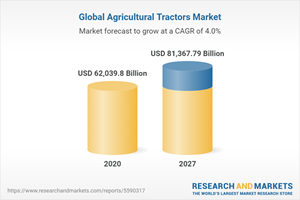

The Global Agricultural Tractors Market size is expected to reach $81.4 billion by 2027, rising at a market growth of 4.2% CAGR during the forecast period.

Tractors are defined as vehicles that are developed to travel at low speeds while producing a large amount of torque. Tractors can haul big agricultural implements behind them due to their high torque. In addition, they are also recognized for delivering massive amounts of power, comparable to that of a semi-truck. Tractors are two-wheel drive in most cases. A traditional farm tractor is a straightforward open vehicle with two huge wheels on one axle. Moreover, the agricultural tractor is designed for a variety of agricultural works, including ploughing, tilling, panning, harrowing, planting, and insecticide spraying, as well as pulling or pushing agricultural machinery or trailers. A rise in the demand for productivity and an increase in the deployment of smart farming is driving the agricultural tractors industry.

Some of the major industry trends are the growing demand for compact tractors on small farms and technical developments like the integration of telematics with agricultural tractors. Moreover, the agricultural industry has been witnessing higher adoption of mechanization in the last couple of years. Additionally, the market is expected to rise as farm laborers are migrating to cities, resulting in a labor shortage in the rural areas.

Row crop tractors are the most popular type of agricultural tractor in the world. Several key market companies are investing much in R&D in order to generate cutting-edge technology and maintain a strong market position. Deere & Company introduced the 8 Family Tractor series in 2020, which includes 8R wheel tractors, 8RT two-track tractors, and the first fixed-frame four-track tractors in the industry. In addition, customers can choose the machine configuration, extras, and horsepower that best suit their operation with these new tractors, which come loaded with the latest precision agriculture technologies.

COVID-19 Impact Analysis

OEMs are presently facing a semiconductor shortage, as well as supply chain interruptions and market uncertainty, as a result of the consistently increasing COVID-19 cases, which may cause manufacturing delays. In addition, an increase in steel and aluminum costs is predicted to raise tractor prices, which is expected to slow market development in the coming quarters.

The United States Department of Agricultural (USDA) introduced the Precision Agriculture Loan (PAL) Act on September 15, 2021, to allow farmers and ranchers to obtain loans to buy precision agriculture equipment. Tractor demand rebounded considerably in H1 2021, in major economies such as the United States, Canada, the United Kingdom, Germany, China, and India. In addition, in 2021, robust crop output in these areas, as well as the requirement to substitute aged equipment, fuelled the demand and sale of agriculture machines.

Market driving Factors:

Farm Mechanization in Emerging Economies

Because their engines have a size of less than 1,500 cc, these tractors take up less space and are more adaptable. Because of the ease of customization, manufacturers are more likely to experiment with novel components and technologies in this category before moving on to higher-powered ones. These tractors are small, with a PTO horsepower of less than 40 and a weight of less than 4,000 pounds. In addition, Schools, landscapers, parks, cemeteries, and hobby farmers all use this high-production, cost-effective, and user-friendly compact tractors. Low horsepower tractors are useful in soft soil conditions, such as river basins. Moreover, horticulture is the primary application for tractors with less than 40 horsepower.

Exponential growth in the global population and supportive governments' policies

Tractor demand is increasing as the world's population grows. Some of the key trends of the market are rapid urbanization, limited labor accessibility, rising food consumption, and technological innovation. When simple demand-supply economics and the flow of labor from urban to rural areas are taken into account, the cost of farm labor has a direct link with the percentage of a country's entire population employed in agriculture. In addition, farmers are expected to boost their yields as the population and demand for food grow. Moreover, agricultural tractors play a vital role in raising agricultural output in India. In recent years, the rising preference for lower-power output tractors, as well as the greater penetration of self-driving tractors, has been witnessed.

Marketing Restraining Factor:

The highly thriving rental industry

Tractors and harvesters, for example, constitute a big investment in agricultural activities and are responsible for a significant portion of the global rental business. The cost of the machinery available to farmers reflects all of the procedures involved in designing, producing, and distributing the equipment.

Farm equipment penetration in emerging countries is low due to small farmers' incapacity to invest a large sum of money. Farmers choose to hire farm machinery to boost output and turnaround time, which boosts the overall efficiency and profitability. When compared to purchasing agricultural equipment with a traditional loan from a financial institution, renting farm equipment is more cost-effective.

Driveline Type Outlook

Based on Driveline Type, the market is segmented into Two-wheel Drive, and Four-wheel Drive. In 2020, the 2WD segment procured the maximum revenue share of the Agricultural Tractors Market. This is because long-term considerations such as lower upfront costs and improved mobility are projected to promote demand in the 2WD segment, particularly in the Asia Pacific market. In India, 2WD tractors are the most popular among middle-income farmers. Hence, these factors are anticipated to drive the growth of this segment over the forecast years.

Key Topics Covered:

Chapter 1. Market Scope & Methodology

Chapter 2. Market Overview

2.1 Introduction

2.1.1 Overview

2.1.1.1 Market Composition and Scenario

2.2 Key Factors Impacting the Market

2.2.1 Market Drivers

2.2.2 Market Restraints

Chapter 3. Competition Analysis - Global

3.1 Publisher Cardinal Matrix

3.2 Recent Industry Wide Strategic Developments

3.2.1 Partnerships, Collaborations and Agreements

3.2.2 Product Launches and Product Expansions

3.2.3 Acquisition and Mergers

3.3 Top Winning Strategies

3.3.1 Key Leading Strategies: Percentage Distribution (2017-2022)

3.3.2 Key Strategic Move: (Product Launches and Product Expansions : 2018, Sep - 2022, Feb) Leading Players

Chapter 4. Global Agricultural Tractors Market by Driveline Type

4.1 Global Two-wheel Drive Market by Region

4.2 Global Four-wheel Drive Market by Region

Chapter 5. Global Agricultural Tractors Market by Engine Power

5.1 Global Less than 40 HP Market by Region

5.2 Global 41 to 100 HP Market by Region

5.3 Global More than 100 HP Market by Region

Chapter 6. Global Agricultural Tractors Market by Region

Chapter 7. Company Profiles

7.1 AGCO Corporation

7.1.1 Company Overview

7.1.2 Financial Analysis

7.1.3 Regional Analysis

7.1.4 Recent strategies and developments:

7.1.4.1 Partnerships, Collaborations, and Agreements:

7.1.4.2 Product Launches and Product Expansions:

7.1.4.3 Acquisition and Mergers:

7.2 Mahindra & Mahindra Limited (Mahindra Group)

7.2.1 Company Overview

7.2.2 Financial Analysis

7.2.3 Segmental and Regional Analysis

7.2.4 Research & Development Expense

7.2.5 Recent strategies and developments:

7.2.5.1 Collaborations, Partnerships and Agreements:

7.2.5.2 Product Launches and Product Expansions:

7.3 CNH Industrial N.V.

7.3.1 Company Overview

7.3.2 Financial Analysis

7.3.3 Segmental and Regional Analysis

7.3.4 Research & Development Expenses

7.3.5 Recent strategies and developments:

7.3.5.1 Partnerships, Collaborations, and Agreements:

7.3.5.2 Product Launches and Product Expansions:

7.3.5.3 Acquisition and Mergers:

7.4 Deere & Company

7.4.1 Company Overview

7.4.2 Financial Analysis

7.4.3 Segmental and Regional Analysis

7.4.4 Research & Development Expenses

7.4.5 Recent strategies and developments:

7.4.5.1 Product Launches and Product Expansions:

7.4.5.2 Acquisition and Mergers:

7.5 Claas KGaA mbH

7.5.1 Company Overview

7.5.2 Financial Analysis

7.5.3 Regional Analysis

7.5.4 Research & Development Expenses

7.5.5 Recent strategies and developments:

7.5.5.1 Partnerships, Collaborations, and Agreements:

7.5.5.2 Product Launches and Product Expansions:

7.6 Escorts Limited

7.6.1 Company Overview

7.6.2 Financial Analysis

7.6.3 Segmental and Regional Analysis

7.6.4 Research & Development Expenses

7.6.5 Recent strategies and developments:

7.6.5.1 Partnerships, Collaborations, and Agreements:

7.6.5.2 Product Launches and Product Expansions:

7.7 International Tractors Limited

7.7.1 Company Overview

7.7.2 Recent strategies and developments:

7.7.2.1 Partnerships, Collaborations, and Agreements:

7.7.2.2 Product Launches and Product Expansions:

7.8 Yanmar Holdings Co., Ltd.

7.8.1 Company Overview

7.9 KUBOTA Corporation

7.9.1 Company Overview

7.9.2 Financial Analysis

7.9.3 Segmental and Regional Analysis

7.9.4 Research & Development Expenses

7.10. Tractors and Farm Equipment Limited

7.10.1 Company Overview

7.10.2 Recent strategies and developments:

7.10.2.1 Product Launches and Product Expansions:

7.10.2.2 Acquisition and Mergers:

For more information about this report visit https://www.researchandmarkets.com/r/prmf6c

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood, Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900