Yahoo Finance

Yahoo Finance Gold and Silver Consolidate after Surge

What is our trading focus?

XAUUSD – Spot gold

XAGUSD – Spot silver

XAUXAG – Gold-Silver ratio

IGLN:xlon – iShares Physical Gold

ISLN:xlon – iShares Physical Silver

Gold was trading quietly around $1800/oz when I started my annual summer holiday in mid-July. Fast forward three weeks and the market has rallied by more than 250 dollars before so far giving a quarter of that back in an overdue correction. Silver meanwhile jumped by 50% to reach a value priced in gold close to the ten-year average.

Gold and silver are two of the best performing assets this year, putting the much hyped technology heavy Nasdaq in the shade.

Why now?

Why did these two metals burst into life in such a dramatic fashion at a time when risk appetite for stocks were strong and economic data had started to stabilise. There are several reasons, one of course being the time of year when liquidity tends to be reduced as traders vacate their desks for the beach. But overall the renewed weakness in U.S. real yields and sudden drop in the dollar were the two main catalysts that helped trigger the rally.

Since gold broke above $1400/oz last June to begin its rally, we have been highlighting the importance of real yields. Some of the major moves in gold during the past decade often started with developments in the bond market. The real yield is the return an investor get on holding a bond position once the nominal yield has been reduced by the expected inflation during the life of the bond. Rising inflation expectations would normally increase the nominal yield as investors would want to be compensated for the lower real return

Yield-curve control which has been mentioned as the potential next step by the U.S. Federal Reserve locks the nominal yield at a certain maturity at a certain level above which the central bank steps in and buy whatever bonds are on offer in order to prevent yields from rising any further. Such a development would make fixed income investments utter useless as a safe haven asset, especially into a period where inflation is expected to make a comeback. Not only due to the massive amount of liquidity that central banks have provided but also due to unprecedented government stimulus creating the political need for higher inflation to support rising debt levels.

The U.S. bond market has since April behaved as if yield-curve control was already in operation. While the yield on U.S. ten-year Notes (above chart) have been anchored within a relatively tight range, the real yield and breakeven have moved in opposite directions. A development supporting the fundamental investment case for holding precious metals in a balanced portfolio.

Falling real yields help support another gold friendly development as it helped drive the dollar lower. The Bloomberg Dollar Index dropped to a two-year low while the euro reached €1.19 before profit taking emerge on Friday when, as real yield reversed higher following a stronger than expected U.S. job report.

What happens now?

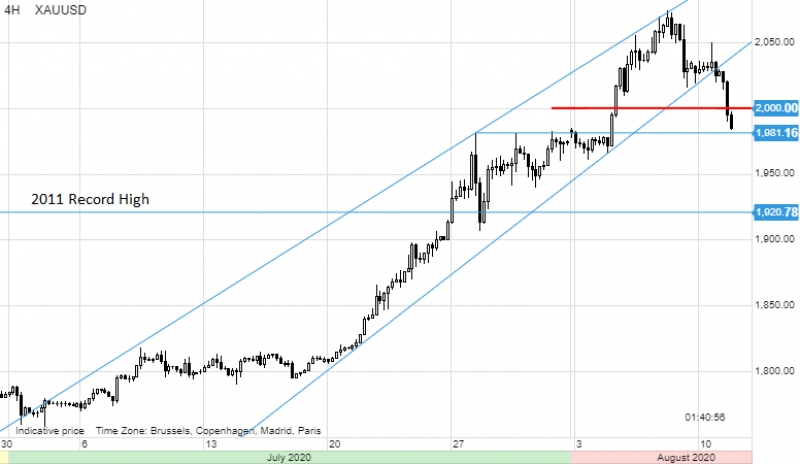

The weakness seen since Friday’s stronger-than-expected U.S. job report has kicked off a battle between short-term technical traders looking to sell, as the steep uptrend is broken and longer-term buyers who missed the move above $2000/oz. Gold’s ability to frustrate will be on display over the coming days as the market consolidates. We see support at $1980/oz followed by the very important $1920/oz level, the former top from 2011.

Overall we maintain a bullish outlook for gold and silver with loose monetary and fiscal policies around the world supporting not only gold and silver but potentially also other mined commodities. Real rates – as highlighted earlier – remains by far the biggest driver for gold and the potential introduction of yield-curve control combined with the risk of rising inflation – as the U.S. authorities are looking to overstimulate the economy – should see those rates remain at record low levels, thereby supporting demand for metals.

An increasingly fraught U.S. elections season combined with current U.S. – China tensions are likely to add another layer of support through safe-haven demand. The potential for even lower real rates should also support a continued weakness of the dollar, thereby creating the trifecta of drivers that should support investments in precious metals.

Silver’s roller coaster year from $18.5/oz in February to $12/oz in March and now $28/oz highlights the often extreme volatility that this semi-precious metal can produce. Silver’s strong surge has apart from the strong momentum attracting new investors, been driven by a combination of its relative cheapness to gold – now removed – and the tailwind coming from rising industrial demand.

Not least from a continued pick up from solar panel producers as the move towards de-carbonisation continues to gather speed. The potential demand additions could over the coming years push silver into a sustained deficit, similar to the 2006-2011 period which culminating in silver almost reaching $50/oz.

For a look at all of today’s economic events, check out our economic calendar.

Ole Hansen, Head of Commodity Strategy at Saxo Bank.

This article is provided by Saxo Capital Markets (Australia) Pty. Ltd, part of Saxo Bank Group through RSS feeds on FX Empire

This article was originally posted on FX Empire

More From FXEMPIRE:

GBP/USD Price Forecast – British Pound Continues Consolidating Against Greenback

Oil Gains Ground As Traders Bet On Continuation Of Demand Rebound

S&P 500 Price Forecast – Stock Markets Continue to Grind Higher

Silver Price Forecast – Silver Markets Break Down Significantly

Oil Price Fundamental Daily Forecast – Supported by Stimulus Hope, Increasing Demand Expectations