Yahoo Finance

Yahoo Finance If You Had Bought MaxCyte (LON:MXCT) Shares Five Years Ago You'd Have Earned 955% Returns

It might be of some concern to shareholders to see the MaxCyte, Inc. (LON:MXCT) share price down 14% in the last month. But that doesn't undermine the fantastic longer term performance (measured over five years). In fact, during that period, the share price climbed 955%. Impressive! So we don't think the recent decline in the share price means its story is a sad one. Of course what matters most is whether the business can improve itself sustainably, thus justifying a higher price.

Anyone who held for that rewarding ride would probably be keen to talk about it.

Check out our latest analysis for MaxCyte

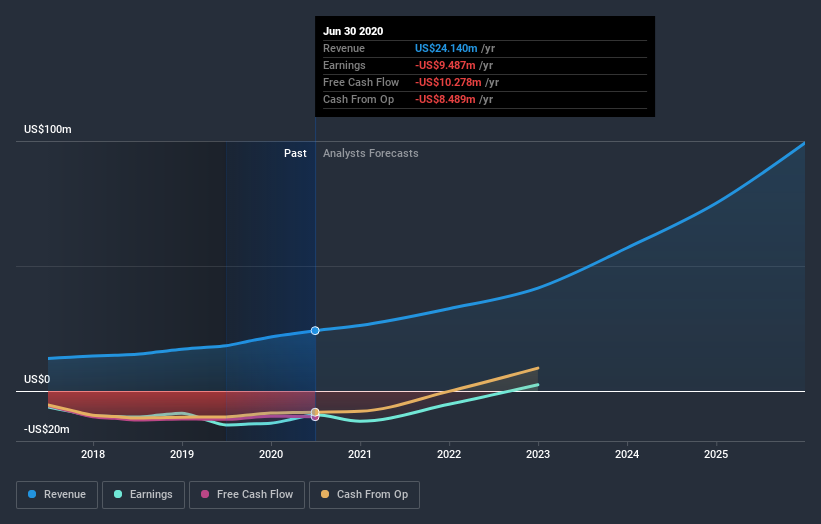

Given that MaxCyte didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. When a company doesn't make profits, we'd generally expect to see good revenue growth. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

In the last 5 years MaxCyte saw its revenue grow at 20% per year. That's well above most pre-profit companies. Fortunately, the market has not missed this, and has pushed the share price up by 60% per year in that time. It's never too late to start following a top notch stock like MaxCyte, since some long term winners go on winning for decades. So we'd recommend you take a closer look at this one, but keep in mind the market seems optimistic.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

This free interactive report on MaxCyte's balance sheet strength is a great place to start, if you want to investigate the stock further.

A Different Perspective

It's good to see that MaxCyte has rewarded shareholders with a total shareholder return of 565% in the last twelve months. That's better than the annualised return of 60% over half a decade, implying that the company is doing better recently. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. It's always interesting to track share price performance over the longer term. But to understand MaxCyte better, we need to consider many other factors. Even so, be aware that MaxCyte is showing 3 warning signs in our investment analysis , you should know about...

If you like to buy stocks alongside management, then you might just love this free list of companies. (Hint: insiders have been buying them).

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on GB exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.