Yahoo Finance

Yahoo Finance Here's Why Avast (LON:AVST) Can Manage Its Debt Responsibly

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. Importantly, Avast Plc (LON:AVST) does carry debt. But the real question is whether this debt is making the company risky.

When Is Debt Dangerous?

Debt assists a business until the business has trouble paying it off, either with new capital or with free cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more usual (but still expensive) situation is where a company must dilute shareholders at a cheap share price simply to get debt under control. Having said that, the most common situation is where a company manages its debt reasonably well - and to its own advantage. The first thing to do when considering how much debt a business uses is to look at its cash and debt together.

View our latest analysis for Avast

How Much Debt Does Avast Carry?

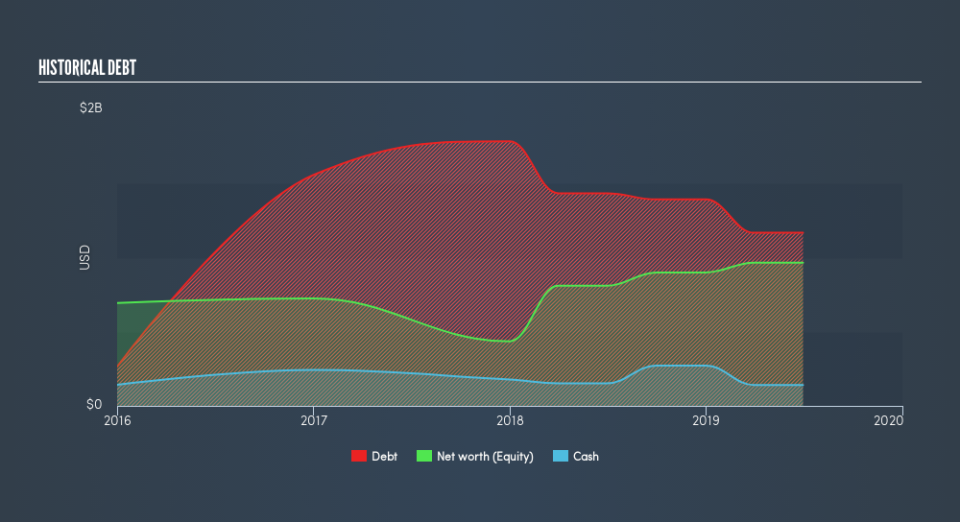

As you can see below, Avast had US$1.17b of debt at June 2019, down from US$1.43b a year prior. However, it does have US$141.0m in cash offsetting this, leading to net debt of about US$1.03b.

A Look At Avast's Liabilities

Zooming in on the latest balance sheet data, we can see that Avast had liabilities of US$554.1m due within 12 months and liabilities of US$1.27b due beyond that. Offsetting these obligations, it had cash of US$141.0m as well as receivables valued at US$96.1m due within 12 months. So its liabilities outweigh the sum of its cash and (near-term) receivables by US$1.58b.

While this might seem like a lot, it is not so bad since Avast has a market capitalization of US$4.30b, and so it could probably strengthen its balance sheet by raising capital if it needed to. However, it is still worthwhile taking a close look at its ability to pay off debt.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). This way, we consider both the absolute quantum of the debt, as well as the interest rates paid on it.

Avast's debt is 2.8 times its EBITDA, and its EBIT cover its interest expense 4.3 times over. This suggests that while the debt levels are significant, we'd stop short of calling them problematic. Looking on the bright side, Avast boosted its EBIT by a silky 49% in the last year. Like a mother's loving embrace of a newborn that sort of growth builds resilience, putting the company in a stronger position to manage its debt. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Avast's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

But our final consideration is also important, because a company cannot pay debt with paper profits; it needs cold hard cash. So we clearly need to look at whether that EBIT is leading to corresponding free cash flow. Over the last three years, Avast actually produced more free cash flow than EBIT. That sort of strong cash generation warms our hearts like a puppy in a bumblebee suit.

Our View

Avast's conversion of EBIT to free cash flow suggests it can handle its debt as easily as Cristiano Ronaldo could score a goal against an under 14's goalkeeper. But, on a more sombre note, we are a little concerned by its net debt to EBITDA. When we consider the range of factors above, it looks like Avast is pretty sensible with its use of debt. That means they are taking on a bit more risk, in the hope of boosting shareholder returns. Another positive for shareholders is that it pays dividends. So if you like receiving those dividend payments, check Avast's dividend history, without delay!

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.