Yahoo Finance

Yahoo Finance Here's Why Hold Strategy is Apt for Eni (E) Stock Right Now

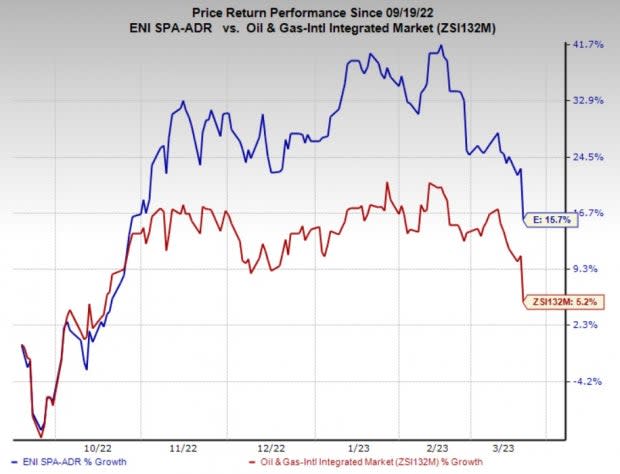

Eni SpA E has gained 15.7% in the past six months compared with the industry’s 5.2% growth.

The company, with a Zacks Rank #3 (Hold), has a Zacks Style Score of A for Value and Growth.

Image Source: Zacks Investment Research

What’s Favoring the Stock?

The price of West Texas Intermediate crude is trading around the $67-per-barrel mark, highlighting a substantial improvement. The positive trajectory in oil prices is a boon for Eni’s upstream operations.

For 2023, Eni expects a total hydrocarbon production of 1.63-1.67 million barrels of oil equivalent per day (MMBoe/d), indicating an increase from the 1.61 MMBoe/d reported in 2022. Coupled with higher oil prices, increased production will boost the company’s bottom line.

In 2022, Eni added about 750 million barrels of oil equivalent (MMBoe) of discovered resources to its reserve base. The significant discoveries amid soaring oil prices are pretty compelling. The company expects to discover exploration resources of 700 MMBoe this year. The developments will boost Eni’s organic growth and cash flow generation.

Eni’s commitment to the energy transition is commendable. It has an ambitious plan of reaching 60 gigawatts of installed renewable energy capacity by 2050. Eni’s integration of its retail and renewable power business, Plenitude, reflects its strong focus on capitalizing on the mounting demand for renewables and green energy products.

Eni’s response to the global energy crisis was a key driver of the Eni gas business’ performance. In 2022, the company’s gas business earned €2.1 billion before interest and taxes, as Eni replaced Russia flows with supplies from countries where it operates.

Eni’s efforts to reward its shareholders are commendable. Benefitting from the rising commodity prices, the company announced a share buyback plan of €2.2 billion for the year. Eni increased its 2023 annual dividend to €0.94 per share, indicating a 7% hike from 2022. The company intends to return 25-30% of annual cash flow to shareholders through these methods.

Risks

Compared with the composite stocks belonging to the industry, Eni’s balance sheet has more debt exposure. As of Dec 31, Eni had long-term debt of €19,374 million, with cash and cash equivalents of €10,155 million. As such, leverage remains a key area of concern for the company.

Stocks to Consider

Investors interested in the energy sector might look at the following companies that presently sport a Zacks Rank #1 (Strong Buy). You can see the complete list of today’s Zacks #1 Rank stocks here.

Sunoco LP’s SUN fourth-quarter 2022 earnings of 42 cents per unit missed the Zacks Consensus Estimate of 77 cents. Weak quarterly earnings resulted from the higher total cost of sales and operating expenses.

Sunoco has witnessed upward estimate revisions for 2023 earnings in the past 30 days. For 2023, Sunoco expects adjusted EBITDA of $850-$900 million.

RPC Inc.’s RES adjusted earnings of 41 cents per share in the fourth quarter beat the Zacks Consensus Estimate of 30 cents. The strong quarterly results were backed by higher activity levels in all the service lines and rising equipment utilization.

As of Dec 31, RPC had cash and cash equivalents of $126.4 million, up sequentially from $73.2 million. Nonetheless, the company managed to maintain a debt-free balance sheet.

Valero Energy Corporation’s VLO fourth-quarter 2022 adjusted earnings of $8.45 per share beat the Zacks Consensus Estimate of $7.45 per share. The strong quarterly results were driven by increased refinery throughput volumes and a higher refining margin.

Valero can benefit from the Gulf Coast export volumes as fuel demand recovery gets support from Asia economies. The Gulf Coast contributed 59.4% to the total throughput volume in the fourth quarter of 2022.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Eni SpA (E) : Free Stock Analysis Report

Valero Energy Corporation (VLO) : Free Stock Analysis Report

Sunoco LP (SUN) : Free Stock Analysis Report

RPC, Inc. (RES) : Free Stock Analysis Report