Yahoo Finance

Yahoo Finance Here's Why Hold Strategy is Apt for Xylem (XYL) Stock Now

Xylem Inc. XYL has been benefiting from strength in Measurement & Control Solutions and accretive acquisitions despite weakness in the residential building solutions market and cost inflation.

Let us discuss the factors why investors should retain the stock for the time being.

Growth Catalysts

Business Strength: Strong backlogs, owing to underlying demand, are aiding Xylem. Due to the essential nature of the business, demand remains robust. The company has been benefiting from robust demand for metrology, water treatment and integrated solutions and services across utilities, industrial and building solutions end markets. Strong growth in the United States, Western Europe and emerging markets is driving Xylem’s top line (up 33% year over year in 2023). Higher volumes, productivity savings and pricing actions are supporting the company’s margins.

At the end of 2023, the company’s backlog totaled $5.1 billion, up 5% year over year backed by strength across all regions. The adjusted EBITDA margin improved to 18.9% in 2023 from 17% in the previous year. For 2024, Xylem expects adjusted EBITDA margin to be approximately 19.4-19.9%, indicating an expansion of 50 to 100 basis points year over year.

Segmental Strength: Resiliency across the utilities and industrial water applications end markets augurs well for Xylem. The Measurement & Control Solutions (M&CS) segment is benefiting from improving supply chains and strong demand in the test and measurement market. For 2023, the company expects the M&CS segment’s organic revenues to increase in the low-twenties digits. Growth in the utilities and industrial end markets is boosting the Water Infrastructure segment’s performance. The company expects Water Infrastructure organic revenues to increase in high-single digits in the current year.

Strength in both the building solutions and industrial end markets/applications is a key catalyst to the Applied Water segment’s growth. Also, improvement in building solutions, driven by continued strength in the commercial market, should foster the unit’s growth. For 2023, Xylem expects the segment’s organic revenues to increase in mid-single digits.

Accretive Acquisition: The company’s expansion initiative is expected to drive growth. The company acquired mission-critical water treatment solutions and services provider, Evoqua, in May 2023. Evoqua’s advanced water and wastewater treatment capabilities and exposure to key industrial markets complement Xylem’s portfolio of solutions across the water cycle. The acquisition bolsters Xylem’s position in water technologies, solutions and services, and strengthens its foothold in lucrative end markets. The transaction is expected to deliver run-rate cost synergies of $140 million within three years upon closing. It is also expected to strengthen the company’s balance sheet.

Rewards to Shareholders: The company continues to increase shareholders’ value through dividend payments. In 2023, Xylem paid dividends of $299 million, up 37.8% year over year. The company also bought back shares worth $25 million in the same year. In February 2024, the company hiked its dividend by 9%. Also, in 2022, Xylem paid out dividends worth $217 million and bought back shares worth $52 million.

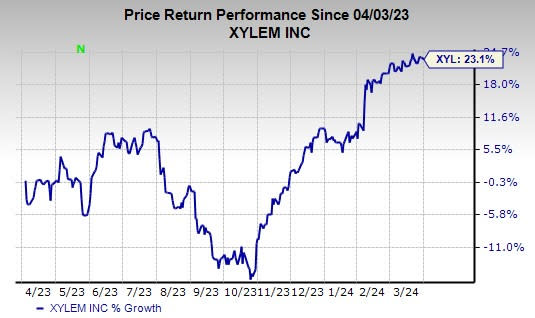

In light of the above-mentioned positives, we believe, investors should retain XYL stock for now, as suggested by its current Zacks Rank #3 (Hold). In the past year, the stock has gained 23.1%.

Image Source: Zacks Investment Research

Stocks to Consider

Some better-ranked companies from the Industrial Products sector are discussed below:

Belden Inc. BDC presently carries a Zacks Rank #2 (Buy) and a trailing four-quarter earnings surprise of 12.3%, on average. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

BDC’s earnings estimates have remained steady for 2024 in the past 60 days. Shares of Belden have risen 3.5% in the past year.

A. O. Smith Corporation AOS presently carries a Zacks Rank of 2. It has a trailing four-quarter average earnings surprise of 12%.

The Zacks Consensus Estimate for AOS’ 2023 earnings increased 0.7% in the past 60 days. Shares of A. O. Smith have rallied 29.4% in the past year.

Applied Industrial Technologies, Inc. AIT presently has a Zacks Rank of 2. It has a trailing four-quarter average earnings surprise of 10.4%.

The Zacks Consensus Estimate for AIT’s fiscal 2024 earnings has increased 1.7% in the past 60 days. The stock has gained 37.4% in the past year.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

A. O. Smith Corporation (AOS) : Free Stock Analysis Report

Applied Industrial Technologies, Inc. (AIT) : Free Stock Analysis Report

Belden Inc (BDC) : Free Stock Analysis Report

Xylem Inc. (XYL) : Free Stock Analysis Report