Yahoo Finance

Yahoo Finance Here's Why Snap-on (SNA) is Marching Ahead of the Industry

Snap-on SNA has been gaining from a continued positive business momentum and contributions from its Value Creation plan despite the tough environment. Management is on track with its Rapid Continuous Improvement process and other cost-reduction initiatives.

This led to a robust surprise trend, which continued in fourth-quarter 2022, wherein both the top and bottom lines beat the Zacks Consensus Estimate. It marked the 10th straight earnings beat and the 11th consecutive sales surprise. Earnings and sales improved year over year.

Adjusted earnings of $4.42 per share improved 7.8% from earnings of $4.10 reported in the prior-year quarter. Net sales grew 4.3% to $1,155.9 million driven by organic sales growth of 8%, partly offset by $37.7 million of negative impacts of foreign-currency translations. Sales and organic sales grew 21% and 22.7%, respectively, from the pre-pandemic levels of 2019.

Adjusted gross profit grew 5.1% year over year. Gross margin expanded 40 basis points (bps) year over year to 48.5%. The upside was backed by higher sales volume and gains from the RCI initiatives, which more than offset higher material and other costs.

The company’s operating earnings before financial services totaled $248 million, up 6.8% year over year.

As a percentage of sales, operating earnings before financial services expanded 50 bps to 21.5% in the fourth quarter.

Consolidated operating earnings (including financial services) were $311.9 million, up 4.2% year over year. As a percentage of sales, operating earnings were flat year over year at 25.1%.

Other Factors Driving the Stock

SNA remains on track with its Rapid Continuous Improvement process and other cost-reduction initiatives. The RCI process is designed to enhance organizational effectiveness and minimize costs, besides helping in boosting sales and margins, and generating savings. Savings from the RCI initiative reflect gains from continuous productivity and process improvement plans.

Management intends to boost customer services, and enhance manufacturing and supply-chain capabilities through the RCI initiatives and further investments.

Snap-on’s ability to innovate bodes well. The company has been investing in new products and increasing brand awareness across the world.

Robust business model helps in enhancing the value-creation processes, which improves safety, quality of service, customer satisfaction and innovation. The company’s growth strategy focuses on three critical areas, namely enhancing the franchise network, improving relationships with repair shop owners and managers, and expanding critical industries in emerging markets.

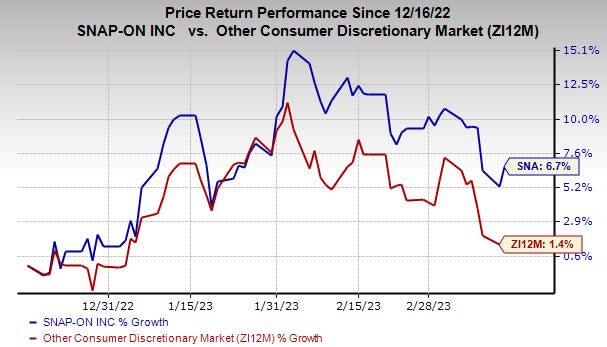

Image Source: Zacks Investment Research

Shares of this Zacks Rank #2 (Buy) company has gained 6.7% in the past three months compared with the industry’s growth of 1.4%.

Wrapping Up

Despite these upsides, the company continues to reel under macroeconomic headwinds, which are likely to persist in 2023. Rising cost inflation, stemming from higher raw material expenses and increased transportation costs, is likely to remain a deterrent. Also, unfavorable currency movements are concerning.

All said, Snap-on’s cost-cutting efforts, RCI plan and solid business momentum are likely to help sustain its momentum and offset inflation and currency woes. The earnings estimate for the current financial year have increased by a penny to $17.1 over the past 30 days. Topping it, a long-term earnings growth rate of 7% reflects its inherent strength.

Have a Look at These Picks

Here we have highlighted three other top-ranked stocks.

BJ's Wholesale Club BJ operates warehouse clubs. BJ currently carries a Zacks Rank #2. You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

The Zacks Consensus Estimate for BJ's Wholesale’s current financial-year’s EPS suggests a rise of 16.6% from the year-ago reported figure. BJ's Wholesale has a trailing four-quarter earnings surprise of 18.2%, on average.

H&R Block HRB provides assisted income tax return preparation and do-it-yourself tax return preparation services. HRB currently carries a Zacks Rank #2.

The Zacks Consensus Estimate for H&R Block’s current financial-year’s EPS suggests growth of 9.4% from the year-ago reported figure. H&R Block has a trailing four-quarter earnings surprise of 10.7%, on average.

Deckers Outdoor Corporation, DECK a leading designer, producer and brand manager of innovative, niche footwear, currently carries a Zacks Rank of 2. DECK has a trailing four-quarter earnings surprise of 31%, on average.

The Zacks Consensus Estimate for Deckers’ current financial year’s sales and earnings suggest growth of 12.2% and 13.6%, respectively, from the year-ago reported figures.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Snap-On Incorporated (SNA) : Free Stock Analysis Report

Deckers Outdoor Corporation (DECK) : Free Stock Analysis Report

BJ's Wholesale Club Holdings, Inc. (BJ) : Free Stock Analysis Report

H&R Block, Inc. (HRB) : Free Stock Analysis Report