Yahoo Finance

Yahoo Finance Here's Why TWC Enterprises Limited's (TSE:TWC) CEO Compensation Is The Least Of Shareholders Concerns

Key Insights

TWC Enterprises' Annual General Meeting to take place on 8th of May

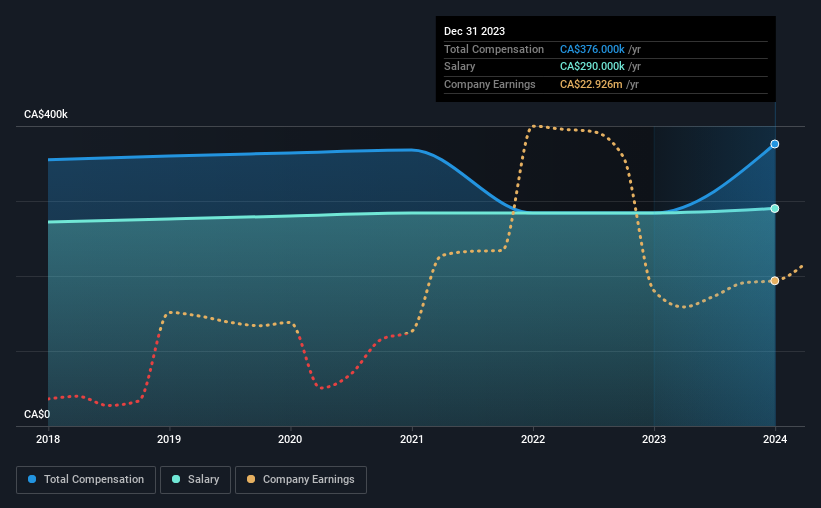

CEO Kuldip Sahi's total compensation includes salary of CA$290.0k

Total compensation is 92% below industry average

TWC Enterprises' three-year loss to shareholders was 19% while its EPS was down 2.3% over the past three years

Shareholders may be wondering what CEO Kuldip Sahi plans to do to improve the less than great performance at TWC Enterprises Limited (TSE:TWC) recently. At the next AGM coming up on 8th of May, they can influence managerial decision making through voting on resolutions, including executive remuneration. Setting appropriate executive remuneration to align with the interests of shareholders may also be a way to influence the company performance in the long run. We have prepared some analysis below to show that CEO compensation looks to be reasonable.

View our latest analysis for TWC Enterprises

How Does Total Compensation For Kuldip Sahi Compare With Other Companies In The Industry?

According to our data, TWC Enterprises Limited has a market capitalization of CA$418m, and paid its CEO total annual compensation worth CA$376k over the year to December 2023. Notably, that's an increase of 32% over the year before. Notably, the salary which is CA$290.0k, represents most of the total compensation being paid.

On examining similar-sized companies in the Canadian Hospitality industry with market capitalizations between CA$275m and CA$1.1b, we discovered that the median CEO total compensation of that group was CA$4.9m. Accordingly, TWC Enterprises pays its CEO under the industry median. Moreover, Kuldip Sahi also holds CA$333m worth of TWC Enterprises stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

Component | 2023 | 2022 | Proportion (2023) |

Salary | CA$290k | CA$284k | 77% |

Other | CA$86k | - | 23% |

Total Compensation | CA$376k | CA$284k | 100% |

Speaking on an industry level, nearly 72% of total compensation represents salary, while the remainder of 28% is other remuneration. Our data reveals that TWC Enterprises allocates salary more or less in line with the wider market. If total compensation veers towards salary, it suggests that the variable portion - which is generally tied to performance, is lower.

TWC Enterprises Limited's Growth

TWC Enterprises Limited has reduced its earnings per share by 2.3% a year over the last three years. In the last year, its revenue is up 50%.

The decrease in EPS could be a concern for some investors. On the other hand, the strong revenue growth suggests the business is growing. In conclusion we can't form a strong opinion about business performance yet; but it's one worth watching. We don't have analyst forecasts, but you could get a better understanding of its growth by checking out this more detailed historical graph of earnings, revenue and cash flow.

Has TWC Enterprises Limited Been A Good Investment?

Given the total shareholder loss of 19% over three years, many shareholders in TWC Enterprises Limited are probably rather dissatisfied, to say the least. So shareholders would probably want the company to be less generous with CEO compensation.

To Conclude...

The loss to shareholders over the past three years is certainly concerning. The downward trend in share price performance may be attributable to the the fact that earnings growth has gone backwards. The upcoming AGM will provide shareholders the opportunity to raise their concerns and evaluate if the board’s judgement and decision-making is aligned with their expectations.

So you may want to check if insiders are buying TWC Enterprises shares with their own money (free access).

Arguably, business quality is much more important than CEO compensation levels. So check out this free list of interesting companies that have HIGH return on equity and low debt.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.