Yahoo Finance

Yahoo Finance Here's Why We're Wary Of Buying EQT Holdings' (ASX:EQT) For Its Upcoming Dividend

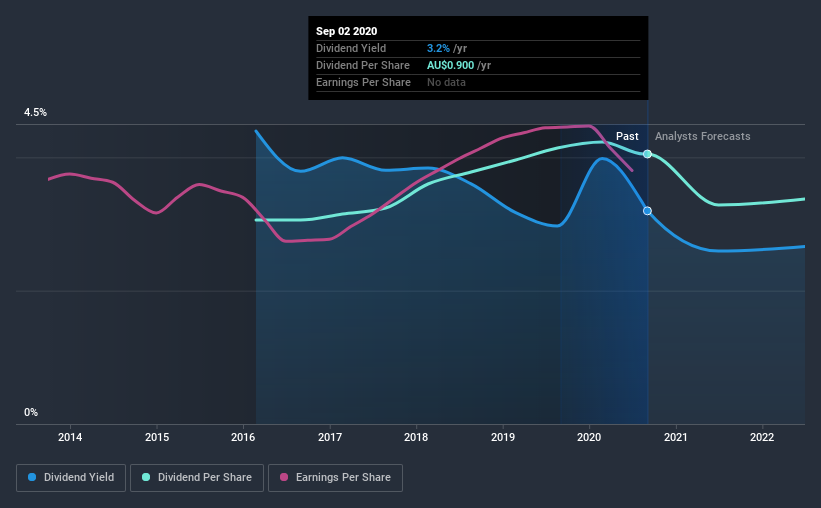

EQT Holdings Limited (ASX:EQT) is about to trade ex-dividend in the next four days. Ex-dividend means that investors that purchase the stock on or after the 7th of September will not receive this dividend, which will be paid on the 6th of October.

EQT Holdings's next dividend payment will be AU$0.43 per share, and in the last 12 months, the company paid a total of AU$0.90 per share. Last year's total dividend payments show that EQT Holdings has a trailing yield of 3.2% on the current share price of A$28.15. If you buy this business for its dividend, you should have an idea of whether EQT Holdings's dividend is reliable and sustainable. So we need to investigate whether EQT Holdings can afford its dividend, and if the dividend could grow.

View our latest analysis for EQT Holdings

If a company pays out more in dividends than it earned, then the dividend might become unsustainable - hardly an ideal situation. Last year, EQT Holdings paid out 97% of its income as dividends, which is above a level that we're comfortable with, especially if the company needs to reinvest in its business.

When a company pays out a dividend that is not well covered by profits, the dividend is generally seen as more vulnerable to being cut.

Click here to see how much of its profit EQT Holdings paid out over the last 12 months.

Have Earnings And Dividends Been Growing?

Companies that aren't growing their earnings can still be valuable, but it is even more important to assess the sustainability of the dividend if it looks like the company will struggle to grow. If earnings fall far enough, the company could be forced to cut its dividend. It's not encouraging to see that EQT Holdings's earnings are effectively flat over the past five years. Better than seeing them fall off a cliff, for sure, but the best dividend stocks grow their earnings meaningfully over the long run.

Many investors will assess a company's dividend performance by evaluating how much the dividend payments have changed over time. In the last five years, EQT Holdings has lifted its dividend by approximately 5.8% a year on average.

The Bottom Line

Has EQT Holdings got what it takes to maintain its dividend payments? EQT Holdings's earnings have barely moved in recent times, and the company is paying out a disagreeably high percentage of its earnings; a mediocre combination. EQT Holdings doesn't appear to have a lot going for it, and we're not inclined to take a risk on owning it for the dividend.

Although, if you're still interested in EQT Holdings and want to know more, you'll find it very useful to know what risks this stock faces. For example, we've found 2 warning signs for EQT Holdings (1 shouldn't be ignored!) that deserve your attention before investing in the shares.

A common investment mistake is buying the first interesting stock you see. Here you can find a list of promising dividend stocks with a greater than 2% yield and an upcoming dividend.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.