Yahoo Finance

Yahoo Finance Can Higher Visits Soften Cost Blow for Teladoc (TDOC) in Q1?

Teladoc Health, Inc. TDOC is set to report its first-quarter 2024 results on Apr 25, after the closing bell. Analysts anticipate a robust performance in the Integrated Care segment, although rising costs may partially offset its results. Let’s delve deeper.

Factors Impacting TDOC

Teladoc’s top line has been benefiting on the back of higher Access Fees, visits and segmental growth in Integrated Care. Growth in U.S. Integrated Care members is likely to have fueled growth in its first-quarter results. Our estimate for first-quarter Access Fee revenues indicates a 1% increase from the prior-year quarter’s tally of $550.9 million.

TDOC’s Integrated Care’s US-based virtual care business is likely to continue its growth trajectory due to rising demand for telehealth services. It boasts a network of approximately 90 million members, giving it the opportunity to cross-sell relevant products and services, diversifying its revenue base. We expect Integrated Care to register top-line growth of 5.3% in the first quarter of 2024. Despite being a market leader in this segment, TDOC continues to face competition in the virtual care space, which might lead to pricing pressures and the need to spend heavily on marketing. However, we expect stable growth in this business going forward.

Chronic Care’s program enrollment is expected to grow, driven by TDOC’s successful bundled chronic care management solutions. TDOC expects chronic care to deliver mid to high single digits average revenue growth in the coming years. The International B2B segment is also expected to contribute to growth in TDOC’s revenues in the future. It expects the overall Integrated Care segment to contribute majorly to overall margin expansion in the next three years.

While the above-mentioned factors are going well for TDOC, there are some points that investors should keep a careful eye on.

Despite rising demand for mental health services, TDOC expects BetterHelp to register low-single-digit growth in the coming three years, a sharp drop from the previous year's growth rates. TDOC’s new customer acquisition requires huge cash outflow on a regular basis to spread awareness. Moreover, we expect a decline in BetterHelp paying users of 4.1% in the first quarter of 2024. Restrained top-line growth due to declining users coupled with rising expenses may hamper the segment’s contribution to the overall company’s margin expansion journey.

Expenses (excluding goodwill impairments) are expected to have escalated 0.7% in the quarter, primarily due to higher advertising and marketing costs. We expect advertising and marketing and sales expenses to rise 1.2% and 2.7%, respectively, in the first quarter of 2024. This is expected to have affected profits, making earnings beat uncertain.

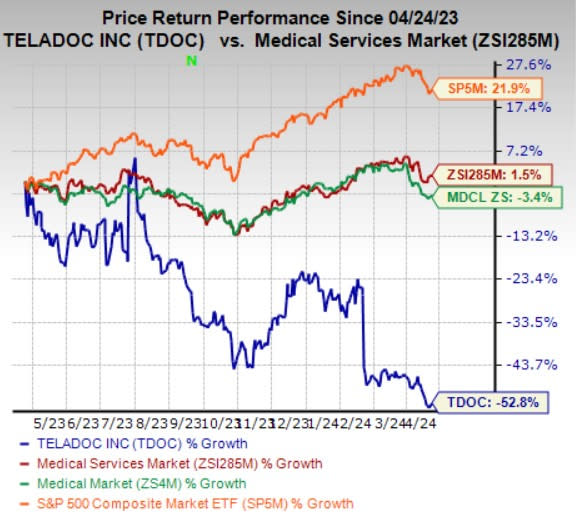

Price Performance

TDOC’s shares have lost 52.8% in the past year against the industry's 1.5% growth. Continued incidence of losses coupled with a slow growth outlook in its BetterHelp segment might have led to declining stock prices.

The Medical sector declined 3.4%, while the S&P 500 Composite increased 21.9% in the same time frame.

Image Source: Zacks Investment Research

Q1 Earnings Preview

The Zacks Consensus Estimate for first-quarter lossper share of 47 cents suggests a 27% deterioration from the prior-year loss of 37 cents. It seems like the positives from the growth in visits will likely be offset by rising costs. The consensus mark remained stable over the past week. Teladoc beat the consensus estimate for earnings in all the prior four quarters, with the average being 16.2%. The consensus estimate for first-quarter revenues of $637 million indicates a 1.2% increase from the year-ago reported figure.

Our proven model does not conclusively predict an earnings beat for Teladoc this time around. The combination of a positive Earnings ESP and a Zacks Rank #1 (Strong Buy), 2 (Buy) or 3 (Hold) increases the chances of an earnings beat. That is not the case here, as you will see below.

Earnings ESP: The company’s Earnings ESP is -5.51%. This is because the Most Accurate Estimate currently stands at a loss of 50 cents per share, higher than the Zacks Consensus Estimate of a loss of 47 cents per share.

You can uncover the best stocks to buy or sell before they’re reported with our Earnings ESP Filter.

Zacks Rank: Teladoc currently carries a Zacks Rank #3.

Stocks to Consider

While an earnings beat looks uncertain for Teladoc, here are some companies from the broader Medical space that you may want to consider, as our model shows that these have the right combination of elements to post an earnings beat this time around:

Lantheus Holdings, Inc. LNTH has an Earnings ESP of +4.29% and a Zacks Rank of 2, at present. You can see the complete list of today’s Zacks #1 Rank stocks here.

The Zacks Consensus Estimate for LNTH’s first-quarter 2024 earnings is pegged at $1.55 per share, which indicates an improvement of 5.4% from the year-ago quarter’s reported figure.

Lantheus’ bottom line beat estimates in each of the trailing four quarters, the average surprise being 14.8%.

HCA Healthcare, Inc. HCA has an Earnings ESP of +13.46% and a Zacks Rank of 2, at present. The Zacks Consensus Estimate for HCA’s first-quarter 2024 earnings is pegged at $5.01 per share, suggesting 1.6% growth from the year-ago quarter’s reported figure.

HCA Healthcare’s bottom line beat estimates in three of the trailing four quarters and missed the mark once, the average surprise being 9.8%.

Insulet Corporation PODD has an Earnings ESP of +11.11% and a Zacks Rank of 2, at present. The Zacks Consensus Estimate for PODD’s first-quarter 2024 earnings is pegged at 39 cents per share, which indicates an improvement of 69.6% from the year-ago quarter’s reported figure.

Insulet’s earnings beat estimates in each of the trailing four quarters, the average surprise being 100.1%.

Stay on top of upcoming earnings announcements with the Zacks Earnings Calendar.

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

HCA Healthcare, Inc. (HCA) : Free Stock Analysis Report

Insulet Corporation (PODD) : Free Stock Analysis Report

Teladoc Health, Inc. (TDOC) : Free Stock Analysis Report

Lantheus Holdings, Inc. (LNTH) : Free Stock Analysis Report