‘I’m in God’s waiting room – how do I cut inheritance tax for my children?’

At 89, Derek Smith still puts some of his savings in the money box his father made for him in the 1940s. “Anything less than a pound I put in it,” he says.

Nowadays he uses the coins he collects to give pocket money to his grandchildren, but he plans to leave them more when he dies.

After a career building submarines for Britain’s Polaris nuclear weapons programme, later working for Chevron before doing consulting work, Mr Smith has travelled the world and now wants little more than to enjoy small luxuries from time to time at his home near Glasgow.

“I bought a bottle of English sparkling wine the day before yesterday. My wife complained it was £20. But I said I worked for 60 years,” he jokes.

“We’ve been to just about every country there is. We’re just sitting in the house at the moment. As I said to my wife a few weeks ago, I feel as though we’re in God’s waiting room.”

As well as dividing up his estate in a tax-efficient way for his five children and seven grandchildren, Mr Smith wants to see better returns on a healthy investment portfolio, comprising £62,000 with Abrdn, and his wife’s £62,000 with Blackrock and £36,000 with Zopa.

Together, the couple have £70,000 in premium bonds and £35,000 of savings in a current account.

They bought their home in Scotland more than half a century ago, which is currently valued at between £350,000 and £400,000. He also owns a campervan, motorbike and two cars.

Mr Smith’s Royal Navy and Chevron pensions, together with his state pension, give him an income of just under £50,000 per year.

Hazel Bowen, senior wealth planner, Canaccord Genuity Wealth Management

The good news is that Mr Smith’s estate is below the band for inheritance tax (IHT), so that should circumvent any issues when he and his wife pass on their estate.

And this is a point for all readers to bear in mind – people often worry about IHT when it doesn’t apply to them. But there are still some good practices Mr Smith can follow to maximise his financial situation.

The combined estate value is £665,000, plus the value of their vehicles which I will estimate at £85,000 – giving a total estate of £750,000.

As a rule of thumb, where there are children and a residential property involved, estates must be more than £500,000 to be impacted by IHT.

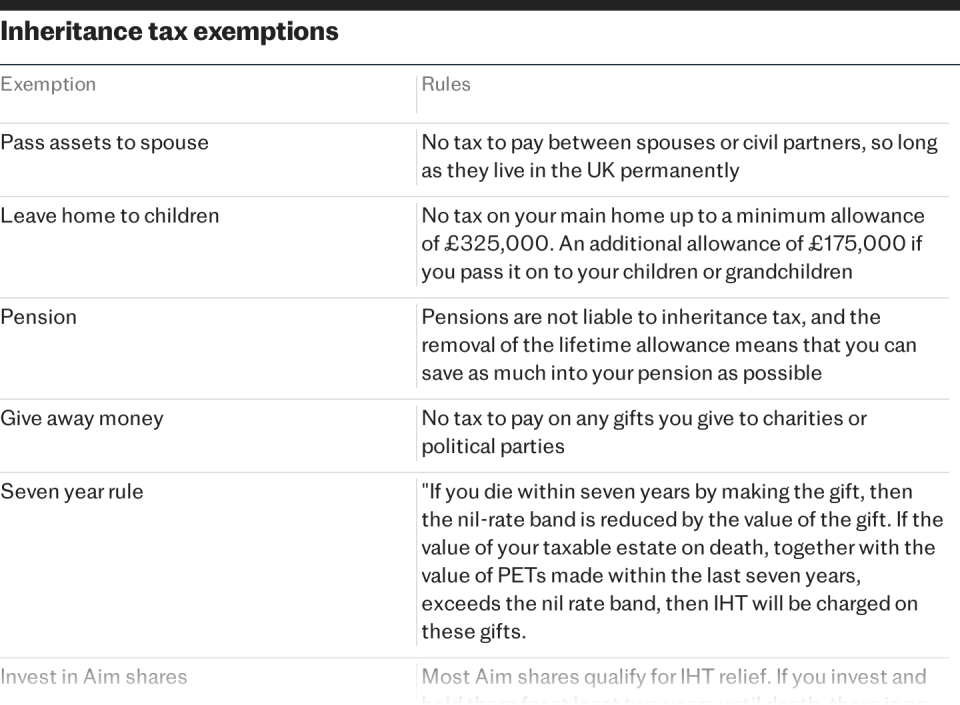

To pass on wealth when they die, the reader and his wife can use the nil rate band (NRB), which means you can pass on up to £325,000 free of IHT.

They can also use the residence nil rate band (RNRB) of £175,000 – this is capped at the value of the residential property and available when a current or previous residential property (or equivalent assets if the property has been sold since 8 July 2015) are passed directly to descendants.

This NRB is reduced by the value of any lifetime gifts made in the previous years in excess of small annual exemptions.

Assuming no previous gifts have been made, and as this couple intend to pass the estate to children and grandchildren, the full NRB and RNRB is available to them both. This means Mr Smith and his wife each have £500,000 that can be passed on IHT-free.

When a spouse dies, they often pass their estate to the survivor. As Mr and Mrs Smith are married, if one of them inherits when the other dies, they will benefit from the spousal transfer exemption from IHT and the transferable NRB.

The unused allowances for both can then be claimed by the administrators of the estate when the second spouse dies.

On the second death the combined value of the NRBs and RNRBs is £1m. The full RNRB allowance of £350,000 is available as the property value exceeds this value.

Since the estate value is £750,000, it falls well within the available NRBs, so IHT will not be due on the estate.

Wills are the most important aspect of estate planning. They could also explore using will trusts to ensure their personal share of assets is ringfenced for their children and grandchildren should they die first, to prevent assets leaving the family if the surviving spouse remarries.

In terms of reducing taxes in retirement – not just IHT – depending on the level of state pension income Mr Smith’s wife receives, she may have some unused personal allowance and she will be able to claim the starting rate for savings income of 0pc for any savings interest that falls within the first £5,000 of taxable income (i.e. income above the personal allowance).

Our reader could transfer part of his savings and investment into his wife’s name, to reduce income tax on any interest income above his 0pc tax personal savings allowance (currently £1,000 for basic rate taxpayers or £500 for higher rate taxpayers) and dividends above the 0pc tax dividend allowance (currently £1,000 but reducing to £500 from 6 April 2024).

Alternatively – assuming our reader’s total income is within the basic rate income tax band – they could make use of the marriage allowance, where his wife can transfer 10pc of her personal allowance to him, increasing the income he can receive tax free by £1,260 and reducing her personal allowance by the same amount.

This can result in a tax saving for our reader of £252 per year.

Neither of these planning methods would be necessary if the investments are already held in a tax-exempt Isa wrapper.

Bradley Russell, investment manager at wealth manager RBC Brewin Dolphin

First of all, well done, Derek; you’ve clearly worked hard for the last 60 years to get where you are today, so it’s about time you thought about how best to enjoy your savings, though I know you are also conscious about what you can leave behind for your children.

It sounds like your home has been your biggest and best investment and this will undoubtedly make up a big part of your eventual estate, which will be passed down to the children.

In addition to this, you have £71,000 in cash savings, £70,000 in premium bonds and £124,000 in investments. This gives you a total “investment pot” of around £262,000.

Firstly, you would need to ensure you have a sufficient “emergency pot” of cash. How much you feel is appropriate is largely down to personal preference, though we recommend a minimum of three to six months’ expenditure.

For these purposes, let’s assume that’s around £10,000, being around five times your net pension income, or thereabouts, though of course you may wish to hold back more, if this makes you more comfortable.

This leaves up to £250,000 potentially available for investment, including your premium bonds. You have given your attitude to risk as “not shy, willing to learn”, so our first priority would be to drill down into this, in a bit more detail.

Recommended

Don’t invest a penny until you’ve read these 11 key rules

It’s really important to understand how you feel about risk and how you may react to periods of volatility in the markets.

While it’s important to generate good returns on your investments, it’s perhaps more important to make sure you are not taking on more risk than you are comfortable with; after all, what’s the point of having money if it’s going to leave you with sleepless nights during difficult times.

Our first port of call would be to review how your existing investments have performed against a relevant benchmark. With a larger pot to invest, we would look to put together a well-diversified spread of investments, potentially consisting of lower risk bonds, shares and some other investments, such as commercial property and commodities like gold and silver.

How much would go into each “basket” would vary depending on our discussions around risk, but the aim here would be to give you the best possible return, at a level of risk you were comfortable with.

From this, we would then agree on a sensible level of income you wished to generate, though practically speaking we may well provide this “income” in the form of both capital returns and naturally produced income, as this is often more tax efficient.

It would also be important to make use of both your and your wife’s Isa allowances each year, to minimise the impact of taxation, with the majority of the investments outside of the Isa held in your wife’s name, to make best use of her allowances.