Yahoo Finance

Yahoo Finance

Insights on the Medical Simulation Global Market to 2030 - Assured Improvement in Patient Safety Outcomes is Driving Growth

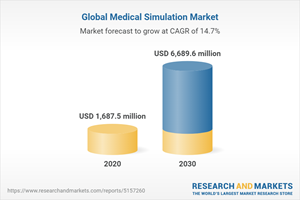

Global Medical Simulation Market

Dublin, April 21, 2022 (GLOBE NEWSWIRE) -- The "Medical Simulation Market by Product & Service, Fidelity, and End User: Global Opportunity Analysis and Industry Forecast, 2021-2030" report has been added to ResearchAndMarkets.com's offering.

The global medical simulation market was valued at $1,687.50 million in 2020, and is estimated to reach $6,689.60 million by 2030, growing at a CAGR of 14.7% from 2021 to 2030.

Medical simulation is a virtual duplication of in situ activities or phenomenon, representing functions and properties of a selective real abstract or process. It is a branch of simulation relating to teaching and training in various medical professions. Simulations can take place in the classroom, in situational settings, or in specially designed venues for simulation exercise. It can include simulated human patients; artificial human, or a combination of the two, educational papers with comprehensive simulated animations, casualty assessment in national security and war scenarios, emergency response, and holographic simulation to support virtual health activities.

Medical simulation also known as healthcare simulation or clinical simulation. It is used to train healthcare professionals using advanced healthcare technologies. It is a contemporary technique that every healthcare practitioner will require but will not always be able to partake in during real-life patient care. Its primary goal was to teach medical professionals to decrease errors in surgery, medication, crisis response, and general practice. It is currently utilized to teach students in anatomy, physiology, and communication during their schooling, when combined with debriefing approaches.

Medical simulators are rapidly becoming a standard component of the educational services provided to medical students, residents, fellows, nursing staff, ancillary health care workers, and practicing physicians all around the world. The rising demand for evidence based treatment services and the decrease in the amount of hours that residents may work each week are two of the reasons for this acceptance. To achieve time, cost, and resource efficiencies that enable successful training, more medical programs are being integrated in traditional classroom and hands-on instruction with the use of computer based medical simulators.

Increase in the use of medical simulation is mainly due rise in use of simulation in healthcare; increase in deaths, owing to medical errors; and necessity to improve patient safety outcomes. According to the World Health Organization (WHO) in 2019, patient safety is one of the serious global public health concern and there is about 1 in 300 chance of a patient being harmed during health care.

In addition, it is estimated that there are about 421 million hospitalizations in the world annually, and approximately 42.7 million adverse events or errors occur in patients during these hospitalizations and is further estimated that patient harm is the 14th leading cause of morbidity and mortality across the world. Moreover, inaccurate or delayed diagnoses affect all settings of care and harm an unacceptable number of patients and research shows that at least 5% of adults in the U.S. experience a diagnostic error each year in outpatient settings. Recent postmortem examination research spanning decades has shown that diagnostic errors contribute to approximately 10% of patient deaths in the U.S.

Moreover, benefits such as training of complex as well as normal cases to professionals and technological advancements in the medical field further increases demand for medical simulation. Limited access to patients during medical training, increasing demand for minimally invasive treatments, and rise in demand for virtual training interaction due to the COVID-19 pandemic has further propelled the growth of the medical simulator market.

The advancement of surgical tools for research and development has raised public awareness of minimally invasive surgical methods. Minimally invasive treatments need specialized psychomotor abilities. Simulation offers the necessary tools for mastering these minimally invasive treatments. In addition, augmented reality is utilized for training and teaching and AR-based apps are utilized to give efficient treatment. Thus, surge in demand for minimally invasive surgical techniques is expected to significantly boost the healthcare simulation market. However, high installation cost and lack of complete real situation restrains the market growth.

The major players profiled in the report are CAE, Inc., Gaumard Scientific Company, Inc., Intelligent Ultrasound Group Plc., Kyoto Kagaku Co. Ltd., Laerdal Medical AS, Limbs and Things, Ltd., Mentice AB, Operative Experience, Inc., Simulab Corporation, and VirtaMed AG.

Key Benefits

This report provides an extensive analysis of the current and emerging market trends and dynamics in the global medical simulation market to identify the prevailing opportunities.

This study presents the competitive landscape of the global market to predict the competitive environment across geographies.

Comprehensive analysis of factors that drive and restrict the market growth is provided.

Region & country-wise analysis is provided to understand the market trends and dynamics.

Key Topics Covered:

CHAPTER 1: INTRODUCTION

CHAPTER 2: EXECUTIVE SUMMARY

CHAPTER 3: MARKET LANDSCAPE

3.1. Market definition and scope

3.2. Key findings

3.2.1. Top investment pockets

3.2.2. Top winning strategies

3.3. Porter's five forces analysis

3.4. Top player positioning, 2020

3.5. Market dynamics

3.5.1. Drivers

3.5.1.1. Increase in use of virtual and augmented reality

3.5.1.2. Assured improvement in patient safety outcomes

3.5.1.3. Benefits of medical simulation

3.5.1.4. Technological advancements in medical field

3.5.1.5. Increase in demand for virtual training

3.5.2. Restraints

3.5.2.1. High cost for setting up simulators

3.5.2.2. Limitation to imitate a complete real situation

3.5.3. Opportunity

3.5.3.1. Lucrative opportunities in emerging markets

3.5.4. Impact analysis

3.6. Impact analysis of COVID-19 on the medical simulation market

CHAPTER 4: GLOBAL MEDICAL SIMULATION MARKET, BY PRODUCT & SERVICE

4.1. Overview

4.1.1. Market size and forecast

4.2. Model-based simulation

4.2.1. Key market trends, growth factors, and opportunities

4.2.2. Market size and forecast, by region

4.2.3. Market analysis, by country

4.2.4. Market size and forecast, by type

4.2.4.1. Patient simulation

4.2.4.1.1. Market size and forecast

4.2.4.1.2. Manikin-based simulation

4.2.4.2. Surgical simulation

4.2.4.2.1. Market size and forecast

4.2.4.3. Ultrasound simulation

4.2.4.3.1. Market size and forecast

4.3. Web-based simulation

4.3.1. Key market trends, growth factors, and opportunities

4.3.2. Market size and forecast, by region

4.3.3. Market analysis, by country

4.3.4. Market size and forecast, by type

4.3.4.1. Simulation software

4.3.4.1.1. Market size and forecast

4.3.4.2. Performance recording software

4.3.4.2.1. Market size and forecast

4.3.4.3. Virtual tutors

4.3.4.3.1. Market size and forecast

4.3.4.4. Learning management software

4.3.4.4.1. Market size and forecast

4.4. Simulation training services

4.4.1. Key market trends, growth factors, and opportunities

4.4.2. Market size and forecast, by region

4.4.3. Market analysis, by country

4.4.4. Market size and forecast, by type

4.4.4.1. Vendor-based training

4.4.4.1.1. Market size and forecast

4.4.4.2. Custom consulting services

4.4.4.2.1. Market size and forecast

4.4.4.3. Educational societies

4.4.4.3.1. Market size and forecast

CHAPTER 5: GLOBAL MEDICAL SIMULATION MARKET, BY FIDELITY

5.1. Overview

5.1.1. Market size and forecast

5.2. Low-fidelity

5.2.1. Market size and forecast, by region

5.2.2. Market analysis, by country

5.3. Medium-fidelity

5.3.1. Market size and forecast, by region

5.3.2. Market analysis, by country

5.4. High-fidelity

5.4.1. Market size and forecast, by region

5.4.2. Market analysis, by country

CHAPTER 6: GLOBAL MEDICAL SIMULATION MARKET, BY END USER

6.1. Overview

6.1.1. Market size and forecast

6.2. Academic institutions

6.2.1. Market size and forecast, by region

6.2.2. Market analysis, by country

6.3. Hospitals

6.3.1. Market size and forecast, by region

6.3.2. Market analysis, by country

6.4. Military organizations

6.4.1. Market size and forecast, by region

6.4.2. Market analysis, by country

CHAPTER 7: MEDICAL SIMULATION MARKET, BY REGION

CHAPTER 8: COMPANY PROFILES

8.1. CAE INC.

8.1.1. Company overview

8.1.2. Company snapshot

8.1.3. Operating business segments

8.1.4. Product portfolio

8.1.5. Business performance

8.1.6. Key strategic moves and developments

8.2. GAUMARD SCIENTIFIC COMPANY

8.2.1. Company overview

8.2.2. Company snapshot

8.2.3. Operating business segments

8.2.4. Product portfolio

8.2.5. Key strategic moves and developments

8.3. INTELLIGENT ULTRASOUND GROUP PLC.

8.3.1. Company overview

8.3.2. Company snapshot

8.3.3. Operating business segments

8.3.4. Product portfolio

8.3.5. Business performance

8.3.6. Key strategic moves and developments

8.4. KYOTO KAGAKU CO. LTD.

8.4.1. Company overview

8.4.2. Company snapshot

8.4.3. Operating business segments

8.4.4. Product portfolio

8.5. LAERDAL MEDICAL AS

8.5.1. Company overview

8.5.2. Company snapshot

8.5.3. Operating business segments

8.5.4. Product portfolio

8.5.5. Key strategic moves and developments

8.6. LIMBS AND THINGS LTD.

8.6.1. Company overview

8.6.2. Company snapshot

8.6.3. Operating business segments

8.6.4. Product portfolio

8.6.5. Key strategic moves and developments

8.7. MENTICE AB

8.7.1. Company overview

8.7.2. Company snapshot

8.7.3. Operating business segments

8.7.4. Product portfolio

8.7.5. Business performance

8.7.6. Key strategic moves and developments

8.8. OPERATIVE EXPERIENCE, INC.

8.8.1. Company overview

8.8.2. Company snapshot

8.8.3. Operating business segment

8.8.4. Product portfolio

8.8.5. Key strategic moves and developments

8.9. SIMULAB CORPORATION

8.9.1. Company overview

8.9.2. Company snapshot

8.9.3. Operating business segments

8.9.4. Product portfolio

8.9.5. Key strategic moves and developments

8.10. VIRTAMED AG

8.10.1. Company overview

8.10.2. Company snapshot

8.10.3. Operating business segment

8.10.4. Product portfolio

8.10.5. Key strategic moves and developments

For more information about this report visit https://www.researchandmarkets.com/r/dvkz7c

Attachment

CONTACT: CONTACT: ResearchAndMarkets.com Laura Wood, Senior Press Manager press@researchandmarkets.com For E.S.T Office Hours Call 1-917-300-0470 For U.S./CAN Toll Free Call 1-800-526-8630 For GMT Office Hours Call +353-1-416-8900