Yahoo Finance

Yahoo Finance Institutional owners may consider drastic measures as easyJet plc's (LON:EZJ) recent UK£171m drop adds to long-term losses

Key Insights

Given the large stake in the stock by institutions, easyJet's stock price might be vulnerable to their trading decisions

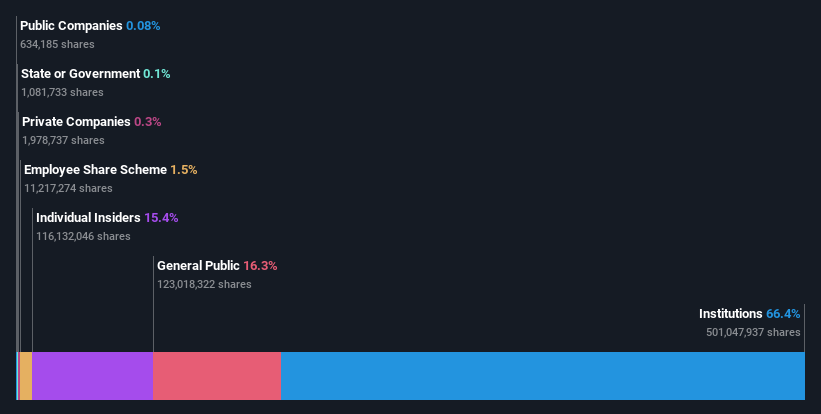

51% of the business is held by the top 17 shareholders

Every investor in easyJet plc (LON:EZJ) should be aware of the most powerful shareholder groups. And the group that holds the biggest piece of the pie are institutions with 66% ownership. Put another way, the group faces the maximum upside potential (or downside risk).

And institutional investors endured the highest losses after the company's share price fell by 4.7% last week. This set of investors may especially be concerned about the current loss, which adds to a one-year loss of 11% for shareholders. Institutions or "liquidity providers" control large sums of money and therefore, these types of investors usually have a lot of influence over stock price movements. As a result, if the decline continues, institutional investors may be pressured to sell easyJet which might hurt individual investors.

Let's take a closer look to see what the different types of shareholders can tell us about easyJet.

See our latest analysis for easyJet

What Does The Institutional Ownership Tell Us About easyJet?

Institutions typically measure themselves against a benchmark when reporting to their own investors, so they often become more enthusiastic about a stock once it's included in a major index. We would expect most companies to have some institutions on the register, especially if they are growing.

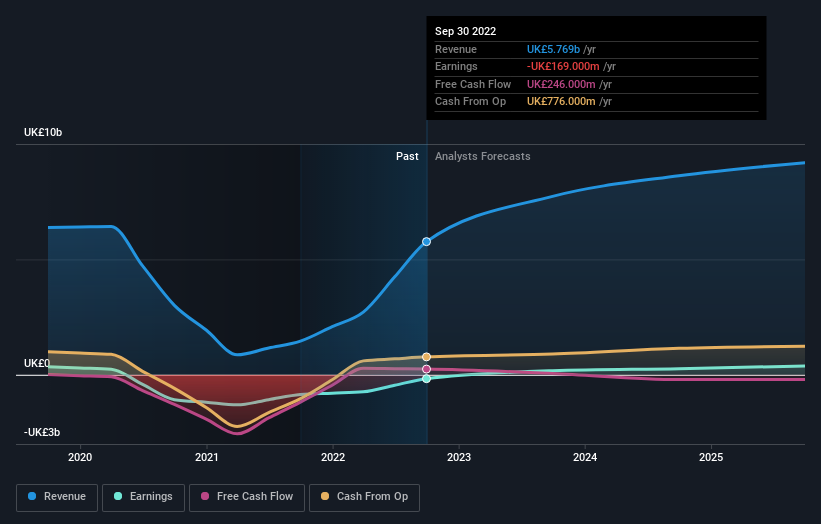

easyJet already has institutions on the share registry. Indeed, they own a respectable stake in the company. This suggests some credibility amongst professional investors. But we can't rely on that fact alone since institutions make bad investments sometimes, just like everyone does. When multiple institutions own a stock, there's always a risk that they are in a 'crowded trade'. When such a trade goes wrong, multiple parties may compete to sell stock fast. This risk is higher in a company without a history of growth. You can see easyJet's historic earnings and revenue below, but keep in mind there's always more to the story.

Institutional investors own over 50% of the company, so together than can probably strongly influence board decisions. easyJet is not owned by hedge funds. Stelios Haji-Ioannou is currently the largest shareholder, with 9.5% of shares outstanding. UBS Asset Management is the second largest shareholder owning 6.0% of common stock, and Polys Haji-Ioannou holds about 5.9% of the company stock.

After doing some more digging, we found that the top 17 have the combined ownership of 51% in the company, suggesting that no single shareholder has significant control over the company.

While it makes sense to study institutional ownership data for a company, it also makes sense to study analyst sentiments to know which way the wind is blowing. There are plenty of analysts covering the stock, so it might be worth seeing what they are forecasting, too.

Insider Ownership Of easyJet

While the precise definition of an insider can be subjective, almost everyone considers board members to be insiders. Management ultimately answers to the board. However, it is not uncommon for managers to be executive board members, especially if they are a founder or the CEO.

I generally consider insider ownership to be a good thing. However, on some occasions it makes it more difficult for other shareholders to hold the board accountable for decisions.

It seems insiders own a significant proportion of easyJet plc. It has a market capitalization of just UK£3.5b, and insiders have UK£535m worth of shares in their own names. That's quite significant. Most would be pleased to see the board is investing alongside them. You may wish to access this free chart showing recent trading by insiders.

General Public Ownership

With a 16% ownership, the general public, mostly comprising of individual investors, have some degree of sway over easyJet. While this size of ownership may not be enough to sway a policy decision in their favour, they can still make a collective impact on company policies.

Next Steps:

It's always worth thinking about the different groups who own shares in a company. But to understand easyJet better, we need to consider many other factors.

I like to dive deeper into how a company has performed in the past. You can access this interactive graph of past earnings, revenue and cash flow, for free.

If you would prefer discover what analysts are predicting in terms of future growth, do not miss this free report on analyst forecasts.

NB: Figures in this article are calculated using data from the last twelve months, which refer to the 12-month period ending on the last date of the month the financial statement is dated. This may not be consistent with full year annual report figures.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here