Yahoo Finance

Yahoo Finance Should You Investigate Dixons Carphone plc (LON:DC.) At UK£1.36?

Want to participate in a short research study? Help shape the future of investing tools and you could win a $250 gift card!

Dixons Carphone plc (LON:DC.), which is in the specialty retail business, and is based in United Kingdom, saw a double-digit share price rise of over 10% in the past couple of months on the LSE. As a mid-cap stock with high coverage by analysts, you could assume any recent changes in the company’s outlook is already priced into the stock. However, what if the stock is still a bargain? Let’s take a look at Dixons Carphone’s outlook and value based on the most recent financial data to see if the opportunity still exists.

View our latest analysis for Dixons Carphone

Is Dixons Carphone still cheap?

Great news for investors – Dixons Carphone is still trading at a fairly cheap price. My valuation model shows that the intrinsic value for the stock is £2.16, which is above what the market is valuing the company at the moment. This indicates a potential opportunity to buy low. Dixons Carphone’s share price also seems relatively stable compared to the rest of the market, as indicated by its low beta. If you believe the share price should eventually reach its true value, a low beta could suggest it is unlikely to rapidly do so anytime soon, and once it’s there, it may be hard to fall back down into an attractive buying range.

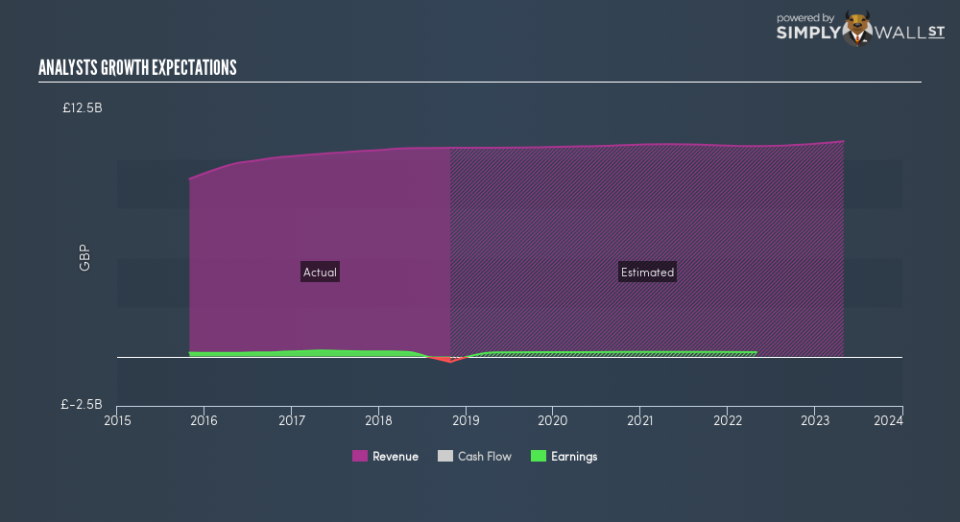

Can we expect growth from Dixons Carphone?

Investors looking for growth in their portfolio may want to consider the prospects of a company before buying its shares. Although value investors would argue that it’s the intrinsic value relative to the price that matter the most, a more compelling investment thesis would be high growth potential at a cheap price. Though in the case of Dixons Carphone, it is expected to deliver a relatively unexciting top-line growth of 1.3% in the next few years, which doesn’t help build up its investment thesis. Growth doesn’t appear to be a main reason for a buy decision for the company, at least in the near term.

What this means for you:

Are you a shareholder? Even though growth is relatively muted, since DC. is currently undervalued, it may be a great time to increase your holdings in the stock. However, there are also other factors such as capital structure to consider, which could explain the current undervaluation.

Are you a potential investor? If you’ve been keeping an eye on DC. for a while, now might be the time to make a leap. Its future outlook isn’t fully reflected in the current share price yet, which means it’s not too late to buy DC.. But before you make any investment decisions, consider other factors such as the track record of its management team, in order to make a well-informed buy.

Price is just the tip of the iceberg. Dig deeper into what truly matters – the fundamentals – before you make a decision on Dixons Carphone. You can find everything you need to know about Dixons Carphone in the latest infographic research report. If you are no longer interested in Dixons Carphone, you can use our free platform to see my list of over 50 other stocks with a high growth potential.

To help readers see past the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price-sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned. For errors that warrant correction please contact the editor at editorial-team@simplywallst.com.