Yahoo Finance

Yahoo Finance Should You Be Investing in Cash?

The latest bull market may prove to be one of the most hated bull markets in history. Pessimism is evident in the outflow of equities and a distinct dislike for anything that has perceived risk. This is naturally creating valuation anomalies which can be a source of both opportunity and risk for investors, and consequently is bringing the notion of value investing back to the fore in their minds.

The irony behind this comment is that the point of maximum pessimism is typically a playground for value investor outperformance. However, unlike other periods of equity withdrawal in 2009 and 2012, we consider this cautious stance a partly-rational response, as it aligns with our valuation-implied return trends.

Both Stocks and Bonds are Expensive

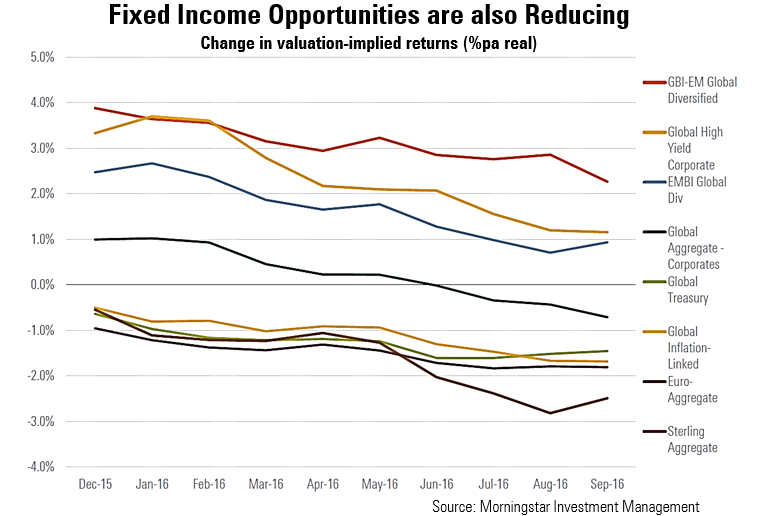

With equities generally becoming more expensive, a typical response would be an increase in defensive assets such as fixed income. However, with central banks manipulating bond yields and interest rates remaining extraordinarily low, we are also seeing the opportunity set shrink in this space too.

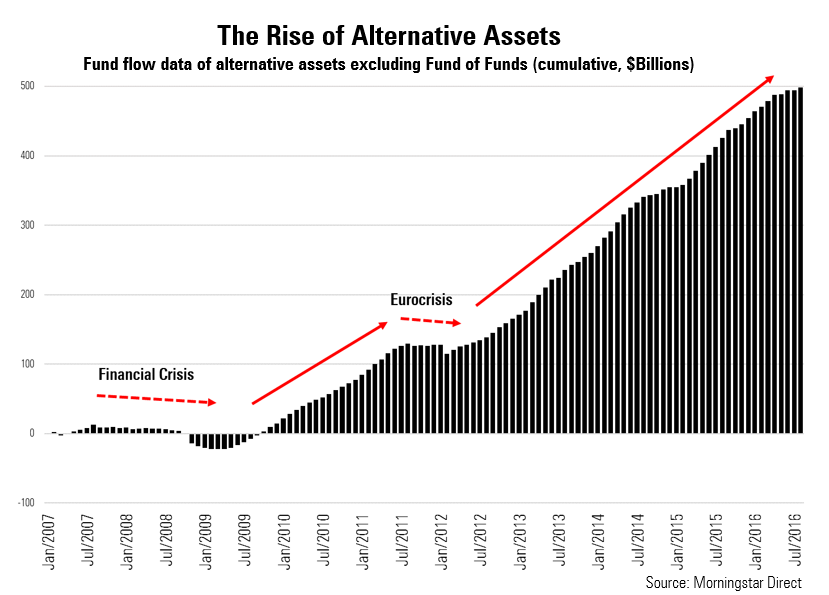

Therefore, as prudent money managers, we must consider the use of non-traditional asset classes; cash can be useful but we also use alternative managers that may be able to achieve positive absolute returns. We are not the only investors seeing this exposure, as demonstrated by the fund flow data into alternatives since the global financial crisis.

Unlike traditional funds which typically provide exposure to the return of a particular asset class, alternative funds are primarily dependent upon the skill of the manager. Consequently, there tends to be significant divergence in returns which adds to the importance of manager selection. It is therefore important to select high quality managers, especially given the survivorship bias we tend to see in the alternative space.

While the popularity of these alternative funds are understandable, confidence in a managers ability to deliver in all environments may be misplaced. Many investors were badly let-down by alternative funds in 2008 and 2011, with negative returns at the time investors needed them the most. Therefore, while selective exposure can be warranted we do not believe it is the silver-bullet most asset allocators are presuming.

Of course, the only other option is cash. This is the most patient play and could be uncomfortable in the shorter-term. However, as Warren Buffett has said “Holding cash is uncomfortable, but not as uncomfortable as doing something stupid”. We couldn’t agree more.