Yahoo Finance

Yahoo Finance Investors Who Bought Apple Hospitality REIT (NYSE:APLE) Shares A Year Ago Are Now Up 71%

These days it's easy to simply buy an index fund, and your returns should (roughly) match the market. But you can significantly boost your returns by picking above-average stocks. To wit, the Apple Hospitality REIT, Inc. (NYSE:APLE) share price is 71% higher than it was a year ago, much better than the market return of around 54% (not including dividends) in the same period. So that should have shareholders smiling. Zooming out, the stock is actually down 16% in the last three years.

See our latest analysis for Apple Hospitality REIT

While the efficient markets hypothesis continues to be taught by some, it has been proven that markets are over-reactive dynamic systems, and investors are not always rational. By comparing earnings per share (EPS) and share price changes over time, we can get a feel for how investor attitudes to a company have morphed over time.

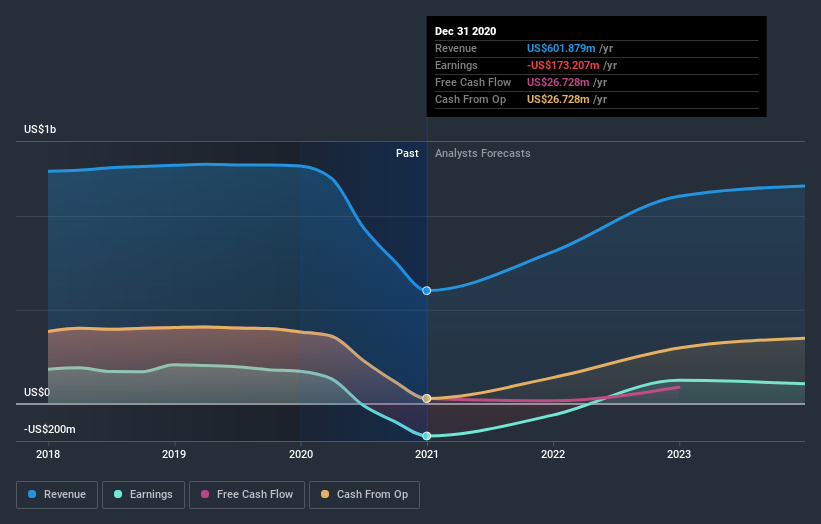

Over the last twelve months Apple Hospitality REIT went from profitable to unprofitable. While this may prove temporary, we'd consider it a negative, so we would not have expected to see the share price up. We might get a clue to explain the share price move by looking to other metrics.

We doubt the modest 0.3% dividend yield is doing much to support the share price. Apple Hospitality REIT's revenue actually dropped 52% over last year. So using a snapshot of key business metrics doesn't give us a good picture of why the market is bidding up the stock.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

We consider it positive that insiders have made significant purchases in the last year. Even so, future earnings will be far more important to whether current shareholders make money. You can see what analysts are predicting for Apple Hospitality REIT in this interactive graph of future profit estimates.

A Different Perspective

We're pleased to report that Apple Hospitality REIT shareholders have received a total shareholder return of 71% over one year. Of course, that includes the dividend. That gain is better than the annual TSR over five years, which is 0.2%. Therefore it seems like sentiment around the company has been positive lately. Someone with an optimistic perspective could view the recent improvement in TSR as indicating that the business itself is getting better with time. It's always interesting to track share price performance over the longer term. But to understand Apple Hospitality REIT better, we need to consider many other factors. Consider for instance, the ever-present spectre of investment risk. We've identified 2 warning signs with Apple Hospitality REIT (at least 1 which is concerning) , and understanding them should be part of your investment process.

There are plenty of other companies that have insiders buying up shares. You probably do not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.