Yahoo Finance

Yahoo Finance Investors more bullish on Mr. Cooper Group (NASDAQ:COOP) this week as stock rises 3.9%, despite earnings trending downwards over past five years

For many, the main point of investing in the stock market is to achieve spectacular returns. While the best companies are hard to find, but they can generate massive returns over long periods. To wit, the Mr. Cooper Group Inc. (NASDAQ:COOP) share price has soared 642% over five years. If that doesn't get you thinking about long term investing, we don't know what will. On top of that, the share price is up 14% in about a quarter. But this move may well have been assisted by the reasonably buoyant market (up 7.8% in 90 days). Anyone who held for that rewarding ride would probably be keen to talk about it.

On the back of a solid 7-day performance, let's check what role the company's fundamentals have played in driving long term shareholder returns.

See our latest analysis for Mr. Cooper Group

In his essay The Superinvestors of Graham-and-Doddsville Warren Buffett described how share prices do not always rationally reflect the value of a business. One flawed but reasonable way to assess how sentiment around a company has changed is to compare the earnings per share (EPS) with the share price.

Mr. Cooper Group's earnings per share are down 20% per year, despite strong share price performance over five years.

This means it's unlikely the market is judging the company based on earnings growth. Because earnings per share don't seem to match up with the share price, we'll take a look at other metrics instead.

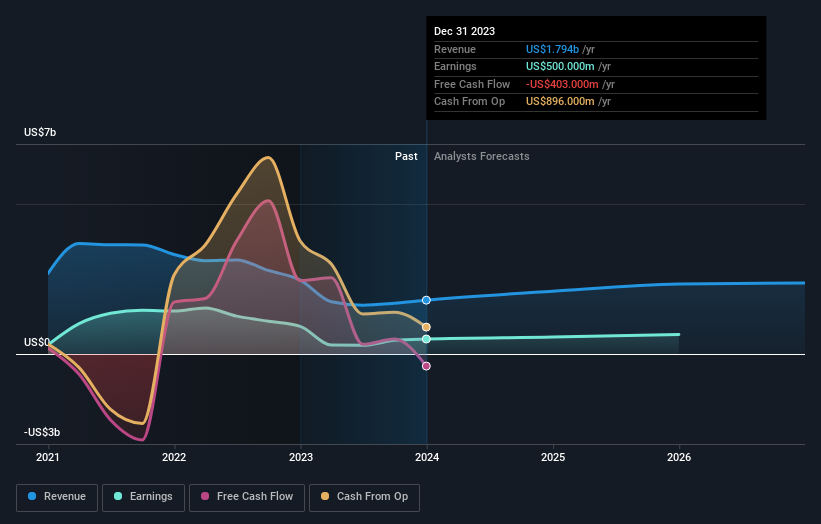

We are not particularly impressed by the annual compound revenue growth of 2.1% over five years. So it seems one might have to take closer look at earnings and revenue trends to see how they might influence the share price.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

It's probably worth noting we've seen significant insider buying in the last quarter, which we consider a positive. That said, we think earnings and revenue growth trends are even more important factors to consider. You can see what analysts are predicting for Mr. Cooper Group in this interactive graph of future profit estimates.

A Different Perspective

We're pleased to report that Mr. Cooper Group shareholders have received a total shareholder return of 94% over one year. Since the one-year TSR is better than the five-year TSR (the latter coming in at 49% per year), it would seem that the stock's performance has improved in recent times. Given the share price momentum remains strong, it might be worth taking a closer look at the stock, lest you miss an opportunity. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 1 warning sign with Mr. Cooper Group , and understanding them should be part of your investment process.

Mr. Cooper Group is not the only stock that insiders are buying. For those who like to find winning investments this free list of growing companies with recent insider purchasing, could be just the ticket.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.