Yahoo Finance

Yahoo Finance Investors Overreacted to Expedia's Earnings

Expedia Group Inc. (EPXE) is a travel company that primarily operates in online bookings. It owns and operates many websites, including hotels.com, travelocity.com, orbitz.com, vrbo.com and expedia.com. It has grown significantly to a market cap of over $14 billion since it was founded in the late 1990s.

Earnings results

The company reported first-quarter earnings after the market closed on May 2. It outperformed Wall Street expectations in regard to revenue (reported $2.89 billion versus $2.81 billion expected) and earnings per share (reported 21 cents versus an anticipated loss of 17 cents).

Margins also improved, with the gross margin jumping 3 basis points to 87.60% compared to the first quarter of 2023.

However, company management lowered the guidance for the rest of the fiscal year. Management is expecting mid- to high-single-digit growth rather than low double-digit growth for fiscal year 2024.

What changed that led to management having a more pessimistic view for the rest of the year?

Vrbo, Expedia's marketplace for vacation rentals (similar to Airbnb (NASDAQ:ABNB)), was migrated to work within Expedia's existing technology. Vrbo's recovery from this migration is taking longer than expected and is hurting Expedia's top and bottom line.

What will fiscal year 2024 look like?

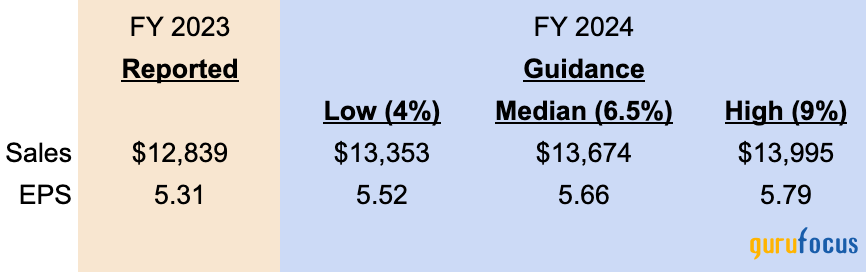

Expedia is expecting single-digit growth in 2024. Most likely, this will look like a 4% to 9% increase from fiscal year 2023.

It is important to note management is also expecting margins to remain flat. So if revenue increases in that range, then we should expect growth to work its way down into gross income, operating income and net income.

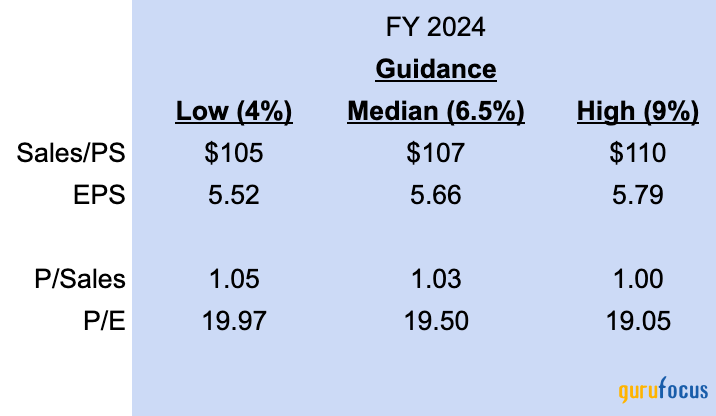

The median guidance would put sales at around $13.50 billion and earnings around $5.66 per share for fiscal year 2024. What would valuation ratios look like using the current price?

Using the current price ($110), this would put the median guidance price-sales at 1.03 and the median guidance price-earnings around 19.50.

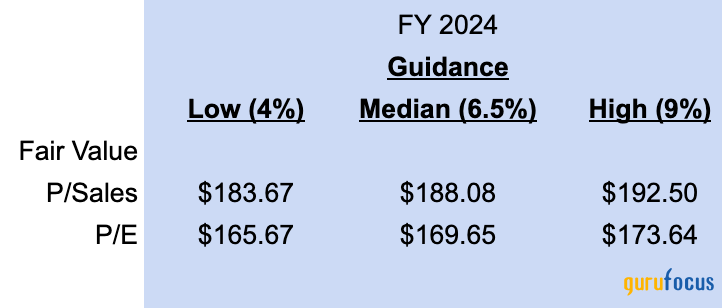

How does this compare to historical figures for Expedia? Historically, the stock trades around 1.750 times sales and 30 times EPS. Using these historical averages, Expedia should be trading in the $170 to $180 range.

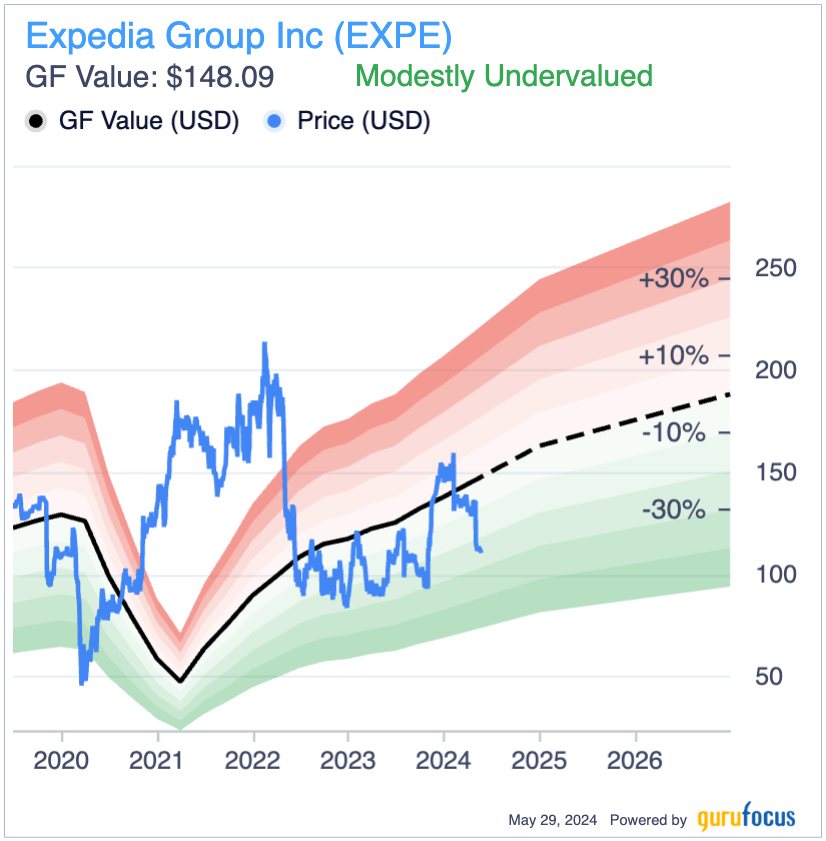

Expedia appears undervalued and GuruFocus agrees. The GF Value is currently around $150 per share, which is lower than my estimates above, but still significantly higher than current trading levels.

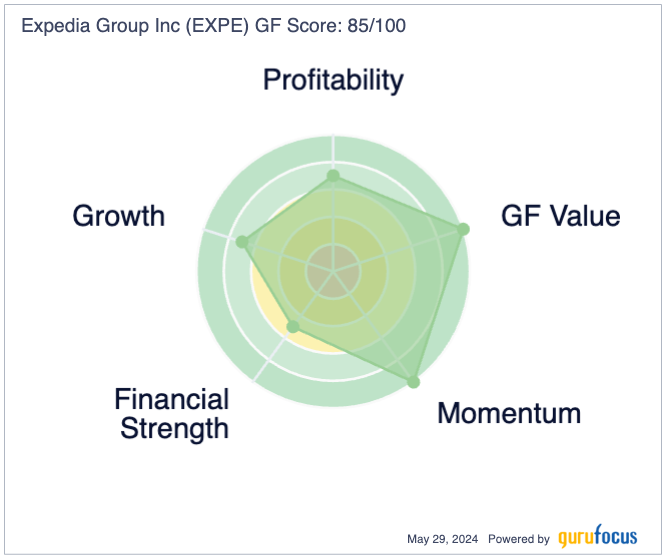

The GF Score also likes Expedia with a score of 85 out of 100 and a perfect 10 out of 10 valuation score.

Even Wall Street analysts are optimistic about Expedia. The average 12-month price target is $143.60, which is 30% higher than the current price.

What's the catch?

This all looks too good to be true. In investing, when something appears too good to be true, it usually is. So what is the catch?

Competition is fierce and might be getting worse.

Online travel is a very competitive industry. The largest player, Booking Holdings (NASDAQ:BKNG), is much larger than Expedia with revenue over $20 billion per year. Plus, new players could be entering the industry.

Alphabet's (NASDAQ:GOOG) Google is looking to leverage its expertise to get into the online travel business. Expedia and its competitors send a lot of money to Google to advertise their sites on the search platform.

However, Google is looking to cut out the middleman and allow hotels to advertise directly through its search engine. Last year, Google announced Performance Max, a new portal for hotels to drive advertisements directly to consumers.

This could pose a significant risk to companies like Expedia if hotels find a lot of value skipping their sites and doing business directly with Google.

Regulatory risk

Vrbo is estimated to account for over $3 billion in revenue for Expedia (about 25% of the total). The service's sales were hit when its interface was migrated over to Expedia's existing technology. That is an issue, but management expects Vrbo to recover, so I anticipate this to be a short-term issue.

However, Vrbo is not out of the woods. There are long-term risks to the business, especially in regards to local regulations.

In late 2023, New York City said it will no longer allow short-term rentals of properties less than 30 days unless the host shares the property with their guests. Other localities in Long Island and the San Francisco Bay area are putting up similar regulations.

Why is this happening? One reason is housing is getting very expensive in some areas so homebuyers are hoping that preventing investors from buying up properties for short-term rental income will provide additional housing inventory. Another reason is hotels in the area want to limit their competition from sites like AirBnB and Vrbo.

How much this will impact Vrbo is unclear. Right now, most localities are requiring short-term rental hosts to zone their properties for short-term rental usage. This is not that big of an issue and should not impact the company.

However, if localities follow New York City's regulatory model, that could significantly hurt its business.

Artificial intelligence is comingand Expedia is short a captain

Artificial intelligence is expected to make significant changes to many business landscapes, and online travel booking is no exception. Expedia is aware of the risks and opportunities AI presents and in 2023 launched travel planning assistance using ChatGPT. This service will assist customers by answering questions about travel destinations or by providing advice on their travel plans.

Earlier in May, Expedia released Romie, an AI-powered travel assistant. Expedia hopes Romie will act as a personalized travel agent for its customers, something that will be new for online travel booking companies.

One of the reasons Expedia is migrating all of its different platforms to a single platform is to be better equipped to handle AI.

AI is definitely on the mind of incoming CEO Ariane Gorin:

"And just in terms of what I get excited about, look, there are a lot of things. I think probably AI and opportunity with AI, and especially now with our platform, given that we have one platform across all of our brands so we can move faster in the way that we're learning, I think, is going to have a bigger opportunity than ever to deliver personalized experiences for travelers."

This all sounds wonderful. AI is coming and Expedia is positioning itself to be ready. So why am I considering this a possible negative?

In mid-May, Expedia fired Chief Technology Officer Rathi Murphy and a senior vice president of products and engineering, Sreenivas Rachamadugu, for violating company policy. We do not know the full details right now, but this leaves Expedia a little vulnerable as it looks to expand its AI offerings.

If Expedia is unable to replace these key positions with effective people, it could set the company back in its AI capabilities and open the door to competitors.

Bottom line: Expedia is still a buy

Expedia is a major player in an industry that is not going anywhere. I do have concerns about potential competition from Google, regulatory risks to Vrbo and leadership changes regarding AI. However, I think the company will make the proper hiring decision for the vacant position and continue its investments in AI.

If Expedia was trading around $150, I would feel a little hesitant to jump in. But at $110, it is a really good deal that is too difficult to pass up.

This article first appeared on GuruFocus.