Yahoo Finance

Yahoo Finance The John Lewis of Hungerford (LON:JLH) Share Price Is Down 63% So Some Shareholders Are Wishing They Sold

Generally speaking long term investing is the way to go. But that doesn't mean long term investors can avoid big losses. Zooming in on an example, the John Lewis of Hungerford plc (LON:JLH) share price dropped 63% in the last half decade. That's not a lot of fun for true believers. And some of the more recent buyers are probably worried, too, with the stock falling 33% in the last year. Furthermore, it's down 24% in about a quarter. That's not much fun for holders. However, one could argue that the price has been influenced by the general market, which is down 33% in the same timeframe.

See our latest analysis for John Lewis of Hungerford

John Lewis of Hungerford wasn't profitable in the last twelve months, it is unlikely we'll see a strong correlation between its share price and its earnings per share (EPS). Arguably revenue is our next best option. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. Some companies are willing to postpone profitability to grow revenue faster, but in that case one does expect good top-line growth.

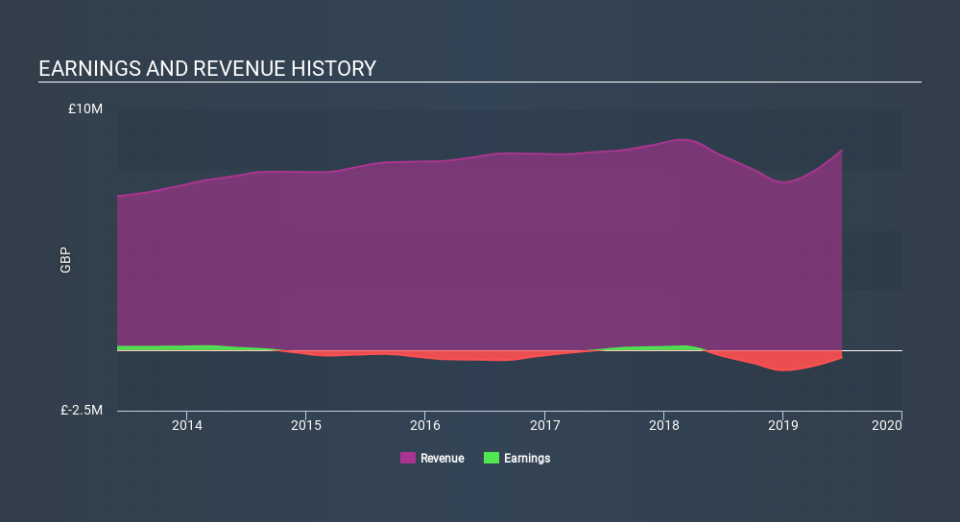

In the last half decade, John Lewis of Hungerford saw its revenue increase by 1.7% per year. That's far from impressive given all the money it is losing. This lacklustre growth has no doubt fueled the loss of 18% per year, in that time. We'd want to see proof that future revenue growth is likely to be significantly stronger before getting too interested in John Lewis of Hungerford. However, it's possible too many in the market will ignore it, and there may be an opportunity if it starts to recover down the track.

The company's revenue and earnings (over time) are depicted in the image below (click to see the exact numbers).

It's probably worth noting that the CEO is paid less than the median at similar sized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. This free interactive report on John Lewis of Hungerford's earnings, revenue and cash flow is a great place to start, if you want to investigate the stock further.

A Different Perspective

While the broader market lost about 25% in the twelve months, John Lewis of Hungerford shareholders did even worse, losing 33%. However, it could simply be that the share price has been impacted by broader market jitters. It might be worth keeping an eye on the fundamentals, in case there's a good opportunity. Unfortunately, last year's performance may indicate unresolved challenges, given that it was worse than the annualised loss of 18% over the last half decade. Generally speaking long term share price weakness can be a bad sign, though contrarian investors might want to research the stock in hope of a turnaround. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. For example, we've discovered 5 warning signs for John Lewis of Hungerford (3 make us uncomfortable!) that you should be aware of before investing here.

We will like John Lewis of Hungerford better if we see some big insider buys. While we wait, check out this free list of growing companies with considerable, recent, insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on GB exchanges.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.