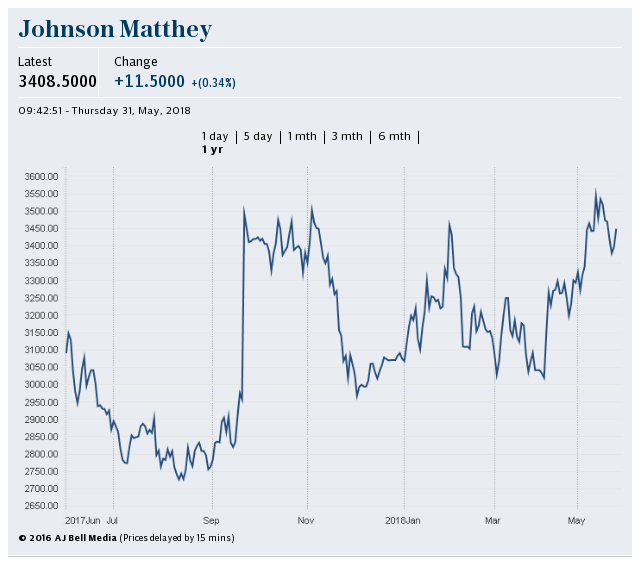

Yahoo Finance

Yahoo Finance Johnson Matthey profits slump as it seeks growth in electric car batteries

Johnson Matthey has reported profits down by almost a third after restructuring costs and a legal charge held back the chemicals company’s annual results.

The business - which is one of the world’s largest suppliers of catalytic converters - said pre-tax profit fell 31pc to £320m after £90m of costs related to its restructuring programme and a £50m charge to settle a contract dispute with a US car manufacturer.

Headline revenues - which are inflated by the cost of the precious metals Johnson Matthey uses in its production processes - were 17pc higher at £14.1bn. Stripping this out, underlying revenue rose 8pc to £3.85bn and underlying pre-tax profit edged up 1pc to £486m in the year to the end of March.

The stronger underlying revenues were largely down to the FTSE 100 company’s catalytic converter-producing clean air business. This is the largest part of Johnson Matthey, responsible for almost three-quarters of all sales. The division’s revenues rose 10pc to £2.5bn and underlying operating profits were also 10pc higher at £349m.

Another strong performer was the new markets unit, which is developing new materials including those to be used in batteries in the growing electric car market. While sales were flat at £312m, its profit rose 37pc driven by the components it produces for use in medical devices.

The company said it expects the division to deliver “break out growth” as it commercialises the “ultra high energy density” battery materials it is developing which are likely to make electric cars more viable. Potential major car manufacturing customers are giving "positive feedback" on the products, it said.

Johnson Matthey has plans to build a battery materials demonstration plant in the UK with double the originally expected production capacity, as well as a commercial plant in Europe.

Robert MacLeod, chief executive, called it a “good year”. He added: “The further development of our next generation battery material was a highlight of the year and I am excited about the speed of progress we are making and the plans we have to commercialise this product.”

The dividend is being raised by 7pc to 80p, which the chief executive said “reflected our confidence in Johnson Matthey’s prospects”.

UBS analysts called the performance “bang in line with expectations” and noted the company’s plans to double the demonstration plant’s capacity to 1,000 tonnes a year.

However, UBS - which has a "sell” rating on Johnson Matthey - urged caution because of the “long-term challenges” faced by diesel which raised questions over demand for catalytic converters. The broker also noted the heavy capital expenditure required for research into battery materials and “limited visibility about the success of technology”.