Yahoo Finance

Yahoo Finance July 2024 Insight Into Three Stocks Estimated Below Value on SIX Swiss Exchange

The Swiss market recently exhibited a nuanced performance, closing slightly down despite an initially strong trading session. This subtle downturn occurred amid broader economic signals, including regional inflation data and U.S. spending reports, which investors are closely monitoring. In such a context, identifying stocks that appear undervalued could offer potential opportunities for those looking to invest in assets that may not fully reflect their intrinsic value given the current economic environment.

Top 10 Undervalued Stocks Based On Cash Flows In Switzerland

Name | Current Price | Fair Value (Est) | Discount (Est) |

COLTENE Holding (SWX:CLTN) | CHF47.10 | CHF76.51 | 38.4% |

Swissquote Group Holding (SWX:SQN) | CHF283.60 | CHF363.81 | 22% |

Burckhardt Compression Holding (SWX:BCHN) | CHF590.00 | CHF847.67 | 30.4% |

Julius Bär Gruppe (SWX:BAER) | CHF50.20 | CHF96.44 | 47.9% |

Sonova Holding (SWX:SOON) | CHF277.60 | CHF463.13 | 40.1% |

Temenos (SWX:TEMN) | CHF62.00 | CHF84.45 | 26.6% |

Comet Holding (SWX:COTN) | CHF362.00 | CHF581.21 | 37.7% |

SGS (SWX:SGSN) | CHF80.00 | CHF125.40 | 36.2% |

Medartis Holding (SWX:MED) | CHF68.60 | CHF129.61 | 47.1% |

Sika (SWX:SIKA) | CHF257.20 | CHF328.39 | 21.7% |

Here's a peek at a few of the choices from the screener

Barry Callebaut

Overview: Barry Callebaut AG operates in the manufacturing and sale of chocolate and cocoa products, with a market capitalization of approximately CHF 8.01 billion.

Operations: The company's revenue is derived from its Global Cocoa segment, which generated CHF 5.31 billion.

Estimated Discount To Fair Value: 18.9%

Barry Callebaut, trading at CHF 1464, is perceived below its fair value of CHF 1804.13, marking a potential undervaluation based on discounted cash flows. Despite recent earnings decline to CHF 77.93 million from CHF 235.49 million half-yearly, the company's future looks promising with expected significant earnings growth and faster revenue increase than the Swiss market average. However, its dividend sustainability is questionable as it's poorly covered by cash flows, and debt levels are concerning relative to operating cash flow.

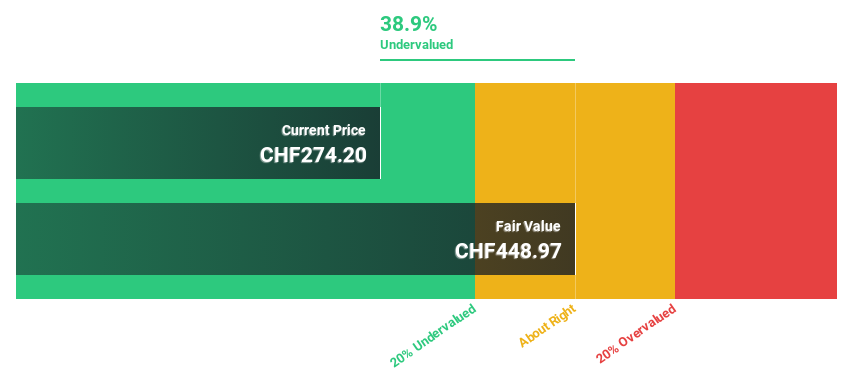

Sonova Holding

Overview: Sonova Holding AG is a company that specializes in manufacturing and selling hearing care solutions for both adults and children across regions including the United States, Europe, the Middle East, Africa, and Asia Pacific, with a market capitalization of CHF 16.55 billion.

Operations: Sonova's revenue is primarily derived from two segments: Cochlear Implants generating CHF 282.40 million and Hearing Instruments contributing CHF 3.36 billion.

Estimated Discount To Fair Value: 40.1%

Sonova Holding, with a current price of CHF 277.6, appears undervalued by over 38% against a fair value estimate of CHF 448.69 based on discounted cash flow analysis. The company's earnings are set to grow by approximately 9.91% annually, outpacing the Swiss market's average of 8.4%. Despite this growth, Sonova carries a high level of debt which may concern investors looking for robust financial health alongside value opportunities.

Our growth report here indicates Sonova Holding may be poised for an improving outlook.

Delve into the full analysis health report here for a deeper understanding of Sonova Holding.

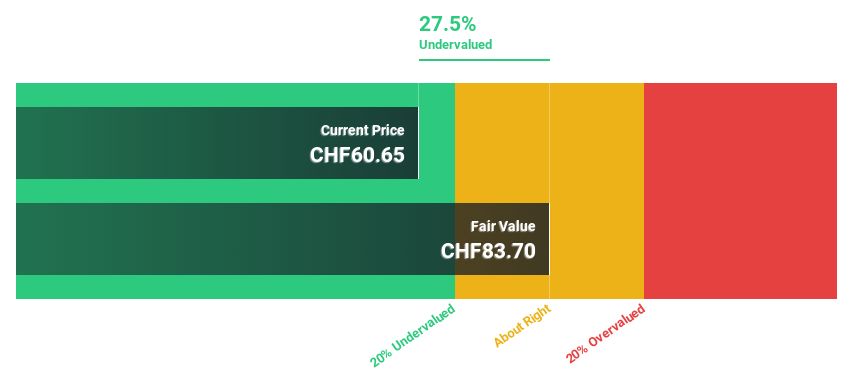

Temenos

Overview: Temenos AG is a global company that develops, markets, and sells integrated banking software systems to financial institutions, with a market capitalization of approximately CHF 4.49 billion.

Operations: The company generates its revenue by providing integrated banking software systems to financial institutions across the globe.

Estimated Discount To Fair Value: 26.6%

Temenos, priced at CHF 62, is trading significantly below its fair value estimate of CHF 84.45, suggesting undervaluation based on cash flows. Despite its high volatility over the past three months and a debt level considered high, Temenos shows promise with an expected revenue growth of 7.6% per year—outpacing the Swiss market's average of 4.4%. The company's earnings are projected to grow by 14.66% annually, which is faster than the market forecast of 8.4%, supported by recent strategic client acquisitions and share buyback initiatives aimed at capital reduction.

Summing It All Up

Investigate our full lineup of 12 Undervalued SIX Swiss Exchange Stocks Based On Cash Flows right here.

Are these companies part of your investment strategy? Use Simply Wall St to consolidate your holdings into a portfolio and gain insights with our comprehensive analysis tools.

Enhance your investing ability with the Simply Wall St app and enjoy free access to essential market intelligence spanning every continent.

Searching for a Fresh Perspective?

Explore high-performing small cap companies that haven't yet garnered significant analyst attention.

Diversify your portfolio with solid dividend payers offering reliable income streams to weather potential market turbulence.

Fuel your portfolio with companies showing strong growth potential, backed by optimistic outlooks both from analysts and management.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Companies discussed in this article include SWX:BARN SWX:SOON and SWX:TEMN.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com