Yahoo Finance

Yahoo Finance Key Things To Understand About Scentre Group's (ASX:SCG) CEO Pay Cheque

Peter Allen has been the CEO of Scentre Group (ASX:SCG) since 2014, and this article will examine the executive's compensation with respect to the overall performance of the company. This analysis will also assess whether Scentre Group pays its CEO appropriately, considering its funds from operations growth and total shareholder returns.

View our latest analysis for Scentre Group

Comparing Scentre Group's CEO Compensation With the industry

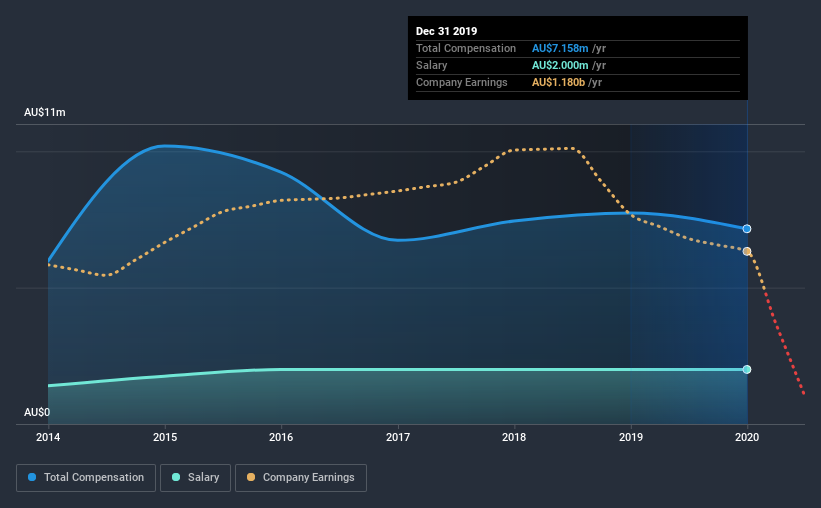

Our data indicates that Scentre Group has a market capitalization of AU$14b, and total annual CEO compensation was reported as AU$7.2m for the year to December 2019. That's a slightly lower by 7.5% over the previous year. We think total compensation is more important but our data shows that the CEO salary is lower, at AU$2.0m.

For comparison, other companies in the industry with market capitalizations above AU$11b, reported a median total CEO compensation of AU$9.2m. This suggests that Scentre Group remunerates its CEO largely in line with the industry average. Moreover, Peter Allen also holds AU$15m worth of Scentre Group stock directly under their own name, which reveals to us that they have a significant personal stake in the company.

Component | 2019 | 2018 | Proportion (2019) |

Salary | AU$2.0m | AU$2.0m | 28% |

Other | AU$5.2m | AU$5.7m | 72% |

Total Compensation | AU$7.2m | AU$7.7m | 100% |

Speaking on an industry level, nearly 51% of total compensation represents salary, while the remainder of 49% is other remuneration. In Scentre Group's case, non-salary compensation represents a greater slice of total remuneration, in comparison to the broader industry. It's important to note that a slant towards non-salary compensation suggests that total pay is tied to the company's performance.

A Look at Scentre Group's Growth Numbers

Over the last three years, Scentre Group has shrunk its funds from operations (FFO) by 6.3% per year. It saw its revenue drop 9.3% over the last year.

Few shareholders would be pleased to read that FFO have declined. This is compounded by the fact revenue is actually down on last year. It's hard to argue the company is firing on all cylinders, so shareholders might be averse to high CEO remuneration. Moving away from current form for a second, it could be important to check this free visual depiction of what analysts expect for the future.

Has Scentre Group Been A Good Investment?

Given the total shareholder loss of 26% over three years, many shareholders in Scentre Group are probably rather dissatisfied, to say the least. This suggests it would be unwise for the company to pay the CEO too generously.

To Conclude...

As we touched on above, Scentre Group is currently paying a compensation that's close to the median pay for CEOs of companies belonging to the same industry and with similar market capitalizations. Meanwhile, FFO growth and shareholder returns have been in the red for the last three years. We'd stop short of saying compensation is inappropriate, but we would understand if shareholders had questions regarding a future raise.

While it is important to pay attention to CEO remuneration, investors should also consider other elements of the business. That's why we did some digging and identified 1 warning sign for Scentre Group that investors should think about before committing capital to this stock.

Switching gears from Scentre Group, if you're hunting for a pristine balance sheet and premium returns, this free list of high return, low debt companies is a great place to look.

This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team@simplywallst.com.