Yahoo Finance

Yahoo Finance Should LANXESS Aktiengesellschaft’s (ETR:LXS) Recent Earnings Decline Worry You?

For long-term investors, assessing earnings trend over time and against industry benchmarks is more beneficial than examining a single earnings announcement at a point in time. Investors may find my commentary, albeit very high-level and brief, on LANXESS Aktiengesellschaft (ETR:LXS) useful as an attempt to give more color around how LANXESS is currently performing. Check out our latest analysis for LANXESS

Was LXS’s recent earnings decline indicative of a tough track record?

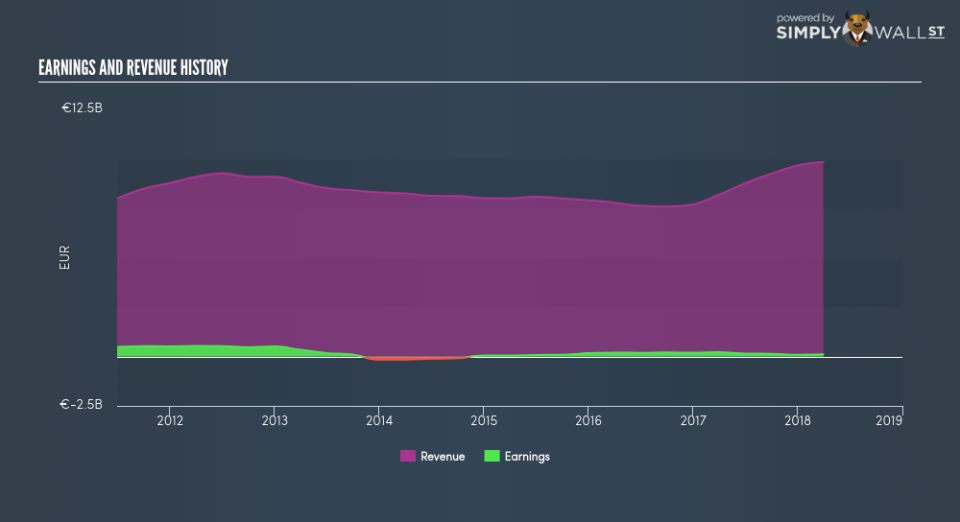

LXS’s trailing twelve-month earnings (from 31 March 2018) of €105.00m has more than halved from €192.00m in the prior year. Furthermore, this one-year growth rate has been lower than its average earnings growth rate over the past 5 years of -23.67%, indicating the rate at which LXS is growing has slowed down. Why could this be happening? Well, let’s look at what’s occurring with margins and if the rest of the industry is facing the same headwind.

Although revenue growth over the last couple of years, has been negative, earnings growth has been falling by even more, meaning LANXESS has been growing its expenses. This harms margins and earnings, and is not a sustainable practice. Scanning growth from a sector-level, the DE chemicals industry has been growing its average earnings by double-digit 13.23% over the prior year, and a more muted 6.32% over the previous five years. This suggests that any uplift the industry is profiting from, LANXESS has not been able to realize the gains unlike its average peer.

In terms of returns from investment, LANXESS has not invested its equity funds well, leading to a 3.80% return on equity (ROE), below the sensible minimum of 20%. Furthermore, its return on assets (ROA) of 1.44% is below the DE Chemicals industry of 6.62%, indicating LANXESS’s are utilized less efficiently. However, its return on capital (ROC), which also accounts for LANXESS’s debt level, has increased over the past 3 years from 5.20% to 8.25%. This correlates with a decrease in debt holding, with debt-to-equity ratio declining from 100.31% to 85.08% over the past 5 years.

What does this mean?

Though LANXESS’s past data is helpful, it is only one aspect of my investment thesis. Typically companies that experience an extended period of decline in earnings are going through some sort of reinvestment phase with the aim of keeping up with the recent industry disruption and growth. I recommend you continue to research LANXESS to get a more holistic view of the stock by looking at:

Future Outlook: What are well-informed industry analysts predicting for LXS’s future growth? Take a look at our free research report of analyst consensus for LXS’s outlook.

Financial Health: Is LXS’s operations financially sustainable? Balance sheets can be hard to analyze, which is why we’ve done it for you. Check out our financial health checks here.

Other High-Performing Stocks: Are there other stocks that provide better prospects with proven track records? Explore our free list of these great stocks here.

NB: Figures in this article are calculated using data from the trailing twelve months from 31 March 2018. This may not be consistent with full year annual report figures.

To help readers see pass the short term volatility of the financial market, we aim to bring you a long-term focused research analysis purely driven by fundamental data. Note that our analysis does not factor in the latest price sensitive company announcements.

The author is an independent contributor and at the time of publication had no position in the stocks mentioned.