Yahoo Finance

Yahoo Finance London's mega-mansion fire sale: why the super rich are slashing millions off their asking prices

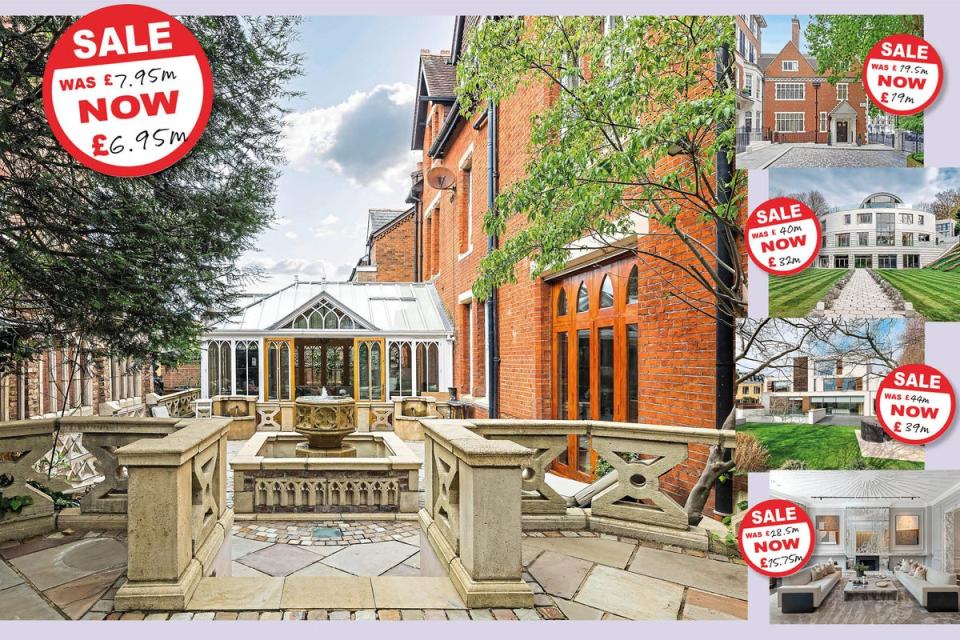

In the early summer the sun was shining, the air was scented with lilac and Kam Babaee was full of optimism when he put his former family home on to the market for £7.95 million.

The magnificent seven-bedroom Gothic vicarage in Chiswick had just been fully renovated and Babaee thought that another family would snap it up.

But over the weeks that followed, his optimism faded along with the lilac blossom. Buyers came to look. One even made an offer but could not raise the cash and had to drop out.

Last month, Babaee bowed to the inevitable and knocked a cool £1 million off his asking price. The house is now listed with Dexters for £6.95 million.

“I am a commercially minded businessman, and £6.95 million in the bank is better than £7.95 million not in the bank,” says Babaee.

Across prime London, homeowners are reaching similar conclusions. Trophy mansions, beloved family homes, glamorous townhouses on famous streets and fabulous lateral flats on garden squares are all having seven-figure sums shaved off their asking prices to tempt buyers over the threshold.

Babaee bought his former vicarage back in 1999, renovated it and moved in with his family. In 2016, in the throes of a divorce, the family moved out.

The house was rented out, for £500,000 a year, until 2021. Then, with the housing market in its post-pandemic boom, Babaee — founder of luxury boutique developer K10 Group — took it back, did it up and put it onto the market.

For him a paper loss of £1 million is not an issue. He has a bigger problem with keeping the house empty and mothballed while he pays about 10 per cent interest on the development loan he took out to do the work to it.

“I am a realistic person,” he says. “Interest rates have surged, and if you are selling a trophy asset like the vicarage, you set a sensible price to get people in through the doors.”

‘It is not just super-distressed sellers cutting prices’

Because Babaee has owned the vicarage for well over two decades, he will certainly enjoy a windfall when he sells — whatever the price. But some owners simply want to unload surplus homes, even at a loss.

Buying agent Camilla Dell, founding partner of Black Brick, is currently acting for a client who is in the process of buying a house in Knightsbridge. “Its owner is a billionaire, he bought it at the peak of the market, and he put it on sale for significantly less than he paid for it,” she says.

“He is selling it for even less, because he just doesn’t need it any more. It is not just super-distressed sellers who are cutting prices.”

Dell believes the rash of price-cutting is down to the fact that vendors have finally woken up to the fact that London’s prime property market is on the fritz.

Savills reports that average sale prices in prime Central London have dropped 1.2 per cent in the past year. Across prime London they are down 2.1 per cent. Transaction levels — the number of homes being bought and sold — have also seen a downturn.

And this stagnation is nothing new. According to house-price analyst LonRes PCL, sale prices almost trebled between 2003 and 2013 — surging from £630 to £1,674 per square foot.

But over the past decade, what with increases in stamp duty, Brexit and the pandemic, they have inched up only 3.5 per cent to £1,733 per square foot.

The same pattern of a decade of dramatic price growth followed by a long slow flatline has been seen across the wider prime London property market too and, it seems, buyers have finally realised that their central London home has not been quite the genius investment they had assumed it would be.

“Finally, the penny is dropping,” says Dell. “Anyone who wants to sell a property has got to be realistic, because buyers are super sensitive about price.”

Madly overpriced

The other issue is that many of the homes currently now being discounted were, to be blunt, madly overpriced to start off with. Buying agent Jo Eccles, managing director of Eccord, agrees.

“We had a shortage of supply during the pandemic, estate agents were desperate for instructions, so they were pricing higher to win instructions,” she says. “There were also vendors who were very overconfident and unrealistic about the value of their homes.”

The cold, hard reality of the prime London market is now making those owners — and agents — change tack. “We have seen estate agents say to sellers that they can’t sell a property for a certain price; they see that it would be a complete waste of time and they are never going to get paid,” she says.

As an estate agent, Marc Schneiderman, director of Arlington Residential, has found himself having some very delicate conversations with prospective vendors about price over the past few months.

“Most property owners at the middle and top end of the market feel that their home is worth more than it is,” he says. “You try explaining to someone who thinks their home is beautiful, but which hasn’t been renovated in 15 years, that a buyer is going to come in and want to redo it all.”

These house-proud owners want to price their properties at a level Schneiderman politely describes as “ambitious and optimistic”. And in a market that is flying, with plenty of eager buyers and not much stock to buy, this strategy can work.

In a market more nervous and price conscious, and in which there are plenty of houses to choose from, it won’t.

Not all sellers have their feet on the ground, however. “There is a house in Knightsbridge we are circling for a client at the moment,” says Eccles. “The owners spent around £15 million on it, and a lot on doing it, but the problem is that the way it is done is very personal and is not going to appeal to anyone else.

"We have to price it as though it were a gut job, unless the client has got immaculate, timeless taste and not many people have that.”

International buyers look to Dubai and Portugal

Traditionally prime central London’s market was propped up by high-rolling international buyers, but while there are plenty looking, says Eccles, few are actually putting hands in pockets.

“They are circling, the appetite is there, but they are so discretionary that they don’t have to buy,” she says. “They still like London but unless there is a really compelling reason they just say: ‘We’ll come back next summer.’”

Dell agrees that the overseas buyer market has been dented in recent years, what with increases in stamp duty — some aimed directly at overseas and second-home owners, and the prospect of the non-dom system — which allows foreign nationals to reside in the UK and pay minimal tax — being dismantled by a possible future Labour government.

“We have to be honest with ourselves,” says Dell. “There are parts of the world which are more welcoming and tax friendly to foreign buyers than we are, like Dubai or Portugal.”

Another deterrent to foreign buyers has been the introduction of tighter anti-money-laundering regulations, which has encouraged the shadier end of the international buyer market to look elsewhere.

Additionally, the decision to impose travel bans and freeze the assets of Russian property owners following the invasion of Ukraine has also sent a clear “go away” message.

Schneiderman thinks that prime central London won’t revive until interest rates come back down again.

Rich people in big houses, he says, might have an enviably Instagram friendly lifestyle but they are no more immune to economic headwinds than anyone else. Their power bills are massive, City bonuses are not what they were and parents are anticipating having to pay VAT on school fees if Labour wins the next general election.

When interest rates were low many of them took on big mortgages. Now they are wondering how to keep on paying them. “Even people in lovely, expensive houses are doing a bit of number crunching,” says Schneiderman.