Yahoo Finance

Yahoo Finance Loss-making BuzzFeed (NASDAQ:BZFD) sheds a further US$10m, taking total shareholder losses to 76% over 1 year

It's not a secret that every investor will make bad investments, from time to time. But it should be a priority to avoid stomach churning catastrophes, wherever possible. So we hope that those who held BuzzFeed, Inc. (NASDAQ:BZFD) during the last year don't lose the lesson, in addition to the 76% hit to the value of their shares. That'd be a striking reminder about the importance of diversification. We wouldn't rush to judgement on BuzzFeed because we don't have a long term history to look at. On top of that, the share price is down 14% in the last week. This could be related to the recent financial results - you can catch up on the most recent data by reading our company report.

After losing 14% this past week, it's worth investigating the company's fundamentals to see what we can infer from past performance.

Check out our latest analysis for BuzzFeed

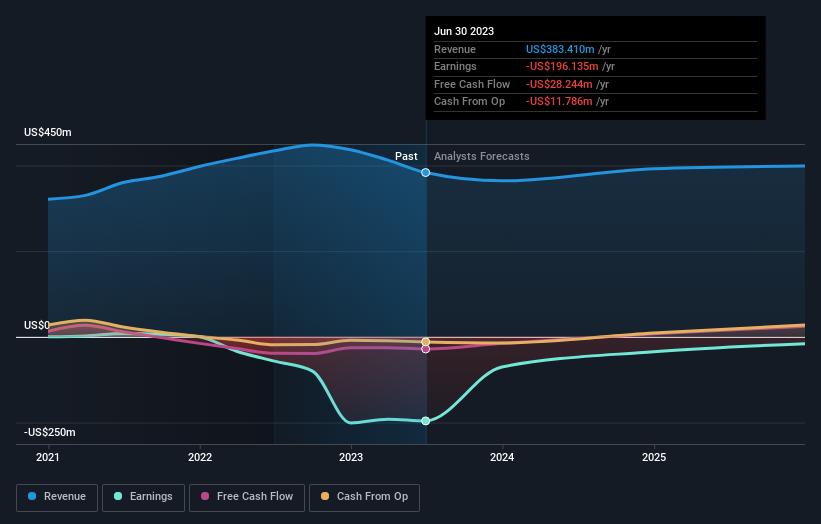

Given that BuzzFeed didn't make a profit in the last twelve months, we'll focus on revenue growth to form a quick view of its business development. Generally speaking, companies without profits are expected to grow revenue every year, and at a good clip. That's because it's hard to be confident a company will be sustainable if revenue growth is negligible, and it never makes a profit.

BuzzFeed's revenue didn't grow at all in the last year. In fact, it fell 12%. That's not what investors generally want to see. The market obviously agrees, since the share price tanked 76%. That's a stern reminder that profitless companies need to grow the top line, at the very least. But markets do over-react, so there opportunity for investors who are willing to take the time to dig deeper and understand the business.

The image below shows how earnings and revenue have tracked over time (if you click on the image you can see greater detail).

It's probably worth noting that the CEO is paid less than the median at similar sized companies. But while CEO remuneration is always worth checking, the really important question is whether the company can grow earnings going forward. This free report showing analyst forecasts should help you form a view on BuzzFeed

A Different Perspective

While BuzzFeed shareholders are down 76% for the year, the market itself is up 4.0%. While the aim is to do better than that, it's worth recalling that even great long-term investments sometimes underperform for a year or more. With the stock down 11% over the last three months, the market doesn't seem to believe that the company has solved all its problems. Basically, most investors should be wary of buying into a poor-performing stock, unless the business itself has clearly improved. I find it very interesting to look at share price over the long term as a proxy for business performance. But to truly gain insight, we need to consider other information, too. Consider for instance, the ever-present spectre of investment risk. We've identified 4 warning signs with BuzzFeed , and understanding them should be part of your investment process.

If you are like me, then you will not want to miss this free list of growing companies that insiders are buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.