Yahoo Finance

Yahoo Finance FTSE hits six-month low after China says US ‘seriously violated’ trade pact: as it happened

A weighed-down FTSE 100 reached its lowest level since late February

European trading turned sharply negative after China says US tariffs break “consensus”

Global stock markets plunged yesterday as global bond markets began to ‘scream recession’

Ambrose Evans-Pritchard: Europe risks losing the UK to the Americans for half a century unless it changes course fast

The FTSE 100 hit a six-month low on Thursday after China warned the US had “seriously violated” the countries’ trade relations by announcing ramped-up tariffs.

A temporary discount on Royal Dutch Shell shares added to the drag on the blue-chip index, which hit its lowest level since late February.

Indices turned red across Europe as investor worries about a trade conflict between the world’s two biggest economies appeared to be facing a fresh escalation.

Bourses worldwide tumbled yesterday as a slew of ominous data suggested economies are being pushed to the brink of recession by increasing trade tensions.

Wrap-up: Messy day for markets leaves FTSE 100 bloodied

Well, that was a bit of a rollercoaster. After a stop-start beginning that suggested traders weren’t sure which way to go, China gave markets a firm bit of direction. An initial rush to safety seemed overblown, however, as Chinese and US rhetoric during the day (so far) stayed calm.

Sadly, it wasn’t enough for the FTSE 100, which continued yesterday’s drop to reach a six-month low, as pressures from widespread share prices falls and a strengthening pound combined to produce a miserable day for the blue-chip index.

The only consolation it can take is that 1) Tomorrow is another day, one where Shell’s price will bounce back, and 2) It isn’t Italy.

That’s all from me today. Tomorrow is set to be a quiet day, with no major economic news or UK company reports expected. If there’s one thing we’re learnt from the past couple of weeks, however, it’s that summer volatility and Donald Trump can make a powerful combo. See you then!

FTSE 100 closes at six-month low

The FTSE closed down 1.13pc, falling by 80.87 points to 7,067.01 — its lowest closing price since February.

London’s blue chip index was caught by a set of negative factors:

Brexit hopes raised the pound

Trade war twitches kept traders on edge

Several shares went ex-dividend, including The Big One (Shell)

The picture was more muted across the continent — except, of course, in Italy, where a rout is quickly becoming a bloodbath.

Round-up: Asda blames Brexit for sales fall, Gem Diamonds finds its shine, FirstGroup gets a new chair and ministers signal fracking rethink

Here are some of the top stories from this afternoon:

Asda boss blames Brexit as sales fall: The supermarket’s boss Roger Burnley blamed Brexit for shattering consumer confidence and knocking the sales in the first half of the year.

Gem Diamonds delivers ‘pleasant surprise’ with higher prices: The small-cap firm delivered a “pleasant surprise” to investors by overcoming a slump in the gemstone market to report higher prices.

FirstGroup buses in ex-Arriva chief as chair after intervention by shareholders: FirstGroup has bowed to shareholder pressure by appointing the former chief executive of rival Arriva as chairman of the troubled rail and bus operator.

Fracking limits could be eased as ministers signal possible rethink: The Government has signalled a possible rethink over strict rules that restrict fracking in a move that is likely to draw anger from environmental campaigners.

Citigroup ups stake in struggling Sirius Minerals

Citigroup has announced an announced an expanded stake in miner Sirius Minerals, which is facing a cash crisis after the last-minute cancellation of its $500m (£411m) bond sale. Shares, which had been sagging all day, cleared their losses after it revealed Citi has increased its position from 0.5pc to 4.8pc.

Meanwhile, in Westminster...

The day’s big squabble remains unchanged: a effort by Jeremy Corbyn to form a ‘caretaker’ government to stop a no-deal Brexit is struggling to gain traction after immediately meeting resistance from the Liberal Democrats. Here’s HuffPost’s Arj Singh:

Lib Dem source says if Corbyn can demonstrate a majority the party could back him as interim PM, but regard the prospect as "unrealistic" and therefore a waste of time.

— Arj Singh (@singharj) August 15, 2019

You can follow the latest political updates here: Brexit latest: ‘Caretaker Corbyn’ plan rejected by Liberal Democrats will be discussed by Tory rebels

Burford names new CFO in wake of short seller attack

Burford Capital has named Jim Kilman as its new chief financial officer, saying “investors would prefer an alternative CFO”.

That’s after the dramatic short seller attack on the litigation funder last week, which included the criticism that Burford’s CEO and current CFO are married.

The company said:

Concern has been raised about the fact that Burford's CEO and Chief Financial Officer ("CFO") are married. We believe that concern is unjustified given Burford's control structure and ignores Burford's finance and accounting structure.

Nevertheless, it is clear that investors would prefer an alternative CFO, and thus Burford announces that, with immediate effect, Jim Kilman will take on the role of CFO to buttress confidence in Burford's financial disclosures and to guide the Company through the change in its listing discussed above.

Now-outgoing CFO Elizabeth O’Connell “will become Burford's Chief Strategy Officer so that Burford can continue to benefit from her long and deep knowledge of the business”.

Here’s our big read on the story: Spoofing, Twitter and 'illegal market manipulation': does Burford have a case against Muddy Waters?

Royal London: Still ‘silver linings’ amid global market malaise

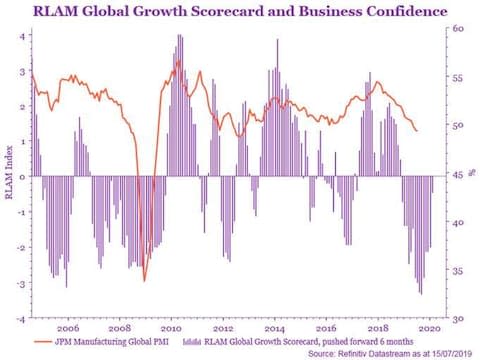

Despite the dreary picture across markets, and the increasing level of fear over an upcoming recession, Royal London Asset Management’s Trevor Greetham still sees reasons to be cheerful. He writes:

There are silver linings. Shorter term lead indicators are improving. Our global growth scorecard is a good six month lead indicator for the world economy and it has been recovering since March, helped by an improvement in US consumer spending and the housing market. Moreover, central banks have started to ease monetary policy and, with inflation low, they will keep cutting interest rates until the world economy responds.

Here’s how that ‘scorecard’ looks:

Turkish investor becomes preferred bidder for British Steel

Ataer Holding, a Turkish investor, has been named as the preferred bidder for British Steel, sources have told the Telegraph. Industry Editor Alan Tovey writes:

Official confirmation of the preferred bidder has been delayed by what one insider called “minor business questions and queries for Ataer”. The Eid religious festival and a national holiday in Turkey has meant that much of the country is shut down until Friday...

...The insider said the issues in question were minor, although there was still a “very slim” chance they could cause the deal to stall.

You can read his full report here: Turkey’s Ataer swoops to rescue British Steel

Trump tweets...

...but it’s just a repeat of what he said yesterday. The US President thinks a personal intervention by the Chinese Premier would be enough to solve issues in Hong Kong.

If President Xi would meet directly and personally with the protesters, there would be a happy and enlightened ending to the Hong Kong problem. I have no doubt! https://t.co/eFxMjgsG1K

— Donald J. Trump (@realDonaldTrump) August 15, 2019

Explained: How to invest through a recession

If the pattern of history carries through, yesterday’s yield curve inversion means the US is due a recession within the next two years. It’s only a sign, however, and if today’s retail data is anything to go by, American GDP growth should hold up fine this quarter.

Through the longer term, however, it’s good to know what to do with your money if a recession hits. Telegraph Money’s Investment Editor Taha Lokhandwala has put together an guide on what investors need to know. “No investor will simply accept the value of their money going in reverse,” he writes.

Taha has split his advice into five key headings:

Shift into cash

Shift into different stocks

Shift into the right funds

Buy the dips

Do nothing

You can read all his tips here: Markets are falling: here’s how you can invest through a recession

Euro drops sharply against dollar as ECB council member says better to ‘overshoot’ on stimulus

The euro has dropped sharply following comments made by Bank of Finland governor Olli Rehn, a member of the European Central Bank’s Governing Council, who said a highly-anticipated stimulus package set to arrive next month needs to be “significant and impactful”.

Speaking to the Wall Street Journal, Mr Rehn said “It’s important that we come up with a significant and impactful policy package in September.” He added:

When you’re working with financial markets, it’s often better to overshoot than undershoot, and better to have a very strong package of policy measures than to tinker.

The ECB is expected to introduce a wide package of measures next month, as it tries to instill some life back into the troubled eurozone.

On the topic of currencies, sterling is having its best day so far this week, with this morning’s strong retail figure providing temporary respite to the currency.

Euro drops as #ECB's Rehn makes big promises. Says stimulus package in Sep may beat expectations. “When you’re working w/ financial markets, it’s often better to overshoot than undershoot,” Mr. Rehn said. https://t.co/4DSAMsa4Jtpic.twitter.com/Dx537jNuWV

— Holger Zschaepitz (@Schuldensuehner) August 15, 2019

Wall Street stumbles slightly at open

Stock exchanges in New York have opened with what can be be described as a wobble — opening narrowly up, dropping slightly and then flattening out.

It’s worth remembering that the Dow Jones Industrial Average is coming off its worst day of the year, so given the mixed messages we’ve been getting from the US and China, traders might be looking for a little guidance.

What a negative yield curve means for investors

If you haven’t got your fill of negative bond yield goodness yet, here’s an explainer for investors. Telegraph Money’s Harry Brennan writes:

The Treasury yield curve has a formidable track record of predicting US recessions, sounding the alarm before every downturn of the last 50 years.

You can read his full breakdown of the situation here: Yield curve inversion: Are we now heading for recession — and is it time for investors to panic?

Trump: China deal must be on ‘our terms’

Here comes the response: Donald Trump has said an agreement with China has to be on “our terms”, Fox Business reported (via Bloomberg). I’ll bring you more when I get it.

More on the wonder of We...

...hard-working tech reporters Matthew Field, James Cook and Hannah Boland have compiled 12 of the most bizarre revelations we found in WeWork’s float prospectus.

In-depth: Why the UK’s luxury car companies are prepared to weather Brexit

Industry Editor Alan Tovey has released the last installment in his three-part series about what a no-deal Brexit would mean for the UK’s car industry. To round things off, he’s taken a look at Britain’s luxury car makers, and why they might find that brand Britain is too valuable to give up. Alan writes:

A no-deal Brexit will bring huge challenges to UK carmakers but, in the very short-term, little is likely to change. Manufacturers are committed to the UK for years to come, and unwinding agreements early will be costly and complex.

There may even be some benefits, with the weaker pound making cars built here cheaper to foreign buyers — although import costs and tariffs could well outweigh this.

You can read his full report here: Why premium and luxury car brands have more reasons to stay in Britain than to go

Parts one and two are here:

Aston Martin shares return to all-time lows

Shares in Aston Martin are once again exploring the depths, down 9.41pc today. Earlier in the week, one bearish analyst said the shares — which are at just under a quarter of their float day high, have a long way left to skid. Here’s our report from then:

US retail beats estimates with biggest gain since March

Consumers have over-delivered again, this time in the US. Retail sales rose 0.7pc in July, their sharpest increase since March and high above expectations of 0.3pc growth.

Like in the UK, online sales underpinned the expansion, meaning once again the hand of Amazon might well be sen in the boost. Prime Day, as well as driving sales in its own right, has also increasingly Amazon’s rivals (basically everyone) to cut prices.

Consumers are clearly seizing the opportunity, and the rises in the US and UK suggest the uncertainty that is increasingly gripping global markets isn’t being felt by regular shoppers.

Jobs data beat expectations the other way, with weekly jobless claims rising to 220,000. That’s not a major shift, but may hint at some underlying issues.

Pantheon Macroecnomics’ Ian Shepherdson said the data should push the US to solid GDP for the quarter:

Headline sales were constrained by a dip in the auto component, no big deal, while the core was propelled by Amazon’s two-day prime event, which lifted nonstore sales by a huge 2.8pc, even better than the 2.5pc we had expected. Ex-nonstore, retail sales ex-autos rose 0.6pc, still respectable, led by electricals, general merchandise and clothing. Restaurants had a good month too, up 1.1pc.

He adds:

The consumer, in short, remains in very good shape, starting the third quarter on a very solid note. Gains at this pace can’t be sustained—control sales rose 9.9pc annualized in the three months to July, compared to the previous three months, about double the pace of income growth—but we see zero evidence that the consumer is being dragged down by the troubles in manufacturing. As consumption accounts for nearly 70pc of GDP, this makes us comfortable expecting GDP growth to exceed 2pc again in the third quarter.

China says it hopes to meet US ‘half-way’ on trade

Some more upbeat talk from China has manage to stymie losses on European indices, with no response from the White House forthcoming just yet.

China’s Ministry of Finance spokesperson said they hoped the US would “meet China half-way” on trade, to avoid a further escalation.

It’s a lot more carrot-y than this morning’s stick, but there’s little reason to believe anything has actually changed, given there haven’t been any further formal talks since Mr Trump announced the new tariffs a fortnight ago.

Here’s the Q&A with China’s MOFCOM that moved futures

(via @onlyyoontv) pic.twitter.com/E9CpWiDtsU— Carl Quintanilla (@carlquintanilla) August 15, 2019

That has pushed US futures up, and cut most European losses . The FTSE 100 and Italian FTSe MiB still stick out like sore thumbs, however — down 1.2 and 2.5pc respectively.

Lunchtime wrap: Trade war ‘kicks investors while they’re down’

There were suggestions this morning that markets would meander as they awaited some kind of signal from on high, but things ended up moving quite quickly this morning.

Let’s sum up the main events:

Hong Kong’s Hang Seng index managed to hold gains for the first time in days despite widespread losses in the Asia-Pacific region. Australian shares had their sharpest drop in 18 months

European markets opened flat, but were quickly sent into a second day of drops after China issued a fresh warning of “countermeasures” if the US proceeds with new tariffs

Surprisingly strong retail figures were not enough to offset trade war fears and ex-dividend share discounts dragging on the FTSE 100

Wall Street looks set to drop at open, with investors holding their breath to see what kind of response emerges from the White House

Here’s more on those retail figures, from my colleague Tim Wallace:

Summing up the morning’s events, Oanda economist Craig Erlam says:

Every time investors find the strength to pick themselves up off the floor, the trade war delivers another blow and knocks them down again... I guess this report also answers the question of whether China viewed the decision to delay half of the tariff hikes until mid-December as being conciliatory in any way or just an act of self-preservation, given the importance of the holiday season in the US.

Speaking of Trump...

...the President is awake and tweeting — or, rather, retweeting praise of himself. The US commander-in-chief is known for moving markets before breakfast, but his timings aren’t always consistent so we might be waiting a bit longer for a response to China’s latest salvo.

What does Hong Kong disruption mean for the trade war?

Tensions in Hong Kong could increasingly become a sticking point in trade war talks, as Donald Trump shows a greater interest in the protests wracking the city.

Tweeting last night, Mr Trump called Xi Jinping a “good man”, and said he believed the Chinese Premier would want to resolve issues. The tweet came straight after two others, in which Mr Trump suggested a deal could only come after China works to “humanely” resolve problems in Hong Kong;

..deferral to December. It actually helps China more than us, but will be reciprocated. Millions of jobs are being lost in China to other non-Tariffed countries. Thousands of companies are leaving. Of course China wants to make a deal. Let them work humanely with Hong Kong first!

— Donald J. Trump (@realDonaldTrump) August 14, 2019

Though far from a formal statement, Mr Trump’s tweet have a habit of sometimes becoming policy. Therefore the suggestion that further progress on trade is contingent on the situation in the Asian financial hub might have been what sparked China’s pugnacious rhetoric today.

Hu Xijin, editor-in-chief of the Chinese state-run paper Global Times, usually gives a good sense of China’s stance on the issues of the day. He tweeted earlier:

President Trump hasn't linked trade talks with Hong Kong problem. It won't work even if he does so. Trade war has dragged on to now, the US has no more economic levers to pressure China. If Beijing determines to intervene, it won't worry about US sanctioning Hong Kong. https://t.co/HUYxXXxage

— Hu Xijin 胡锡进 (@HuXijin_GT) August 15, 2019

This is partially untrue — although the full tariffs the US is preparing would effectively cover all its imports from China, tariffs could also be raised further (which might mean a 25pc levy on all goods).

Space race: Everything you need to know about WeWork’s wild float plans

One of the more business bizarre stories in recent years is that of WeWork, the office rental company that seems part-company, part-cult.

The company has grown rapidly over the past decade, and is now eyeing a mega-float, which could be as soon as next month, that would give it a valuation of up to $47bn. I’ll let the Telegraph’s US business correspondent Laurence Dodds take it from here:

It is not every day that a corporate document filed with financial regulators begins with a sentence like: "We dedicate this to the energy of we – greater than any one of us but inside each of us."

Still, that is how WeWork, the rapidly growing office rental company with hundreds of elegantly-decorated beachheads in major cities around the world, began the official prospectus for its hotly-anticipated public float later this year.

Laurence has taken a closer look at that propectus, and his findings make for a reading that is probably best described as inspiring awe — and maybe a little scepticism. One choice quote from an analyst who has looked at WeWork’s proposal:

It doesn't make any sense

You can read Laurence’s full analysis here: Is $47bn WeWork the office of the future – or an overvalued confidence trick?

Ladbrokes owner raises profit forecast but will plow ahead with closures

GVC, the company behind bettting shops Ladbrokes and Coral, raised its profit forecast this morning despite fears of a regulatory crackdown, but will press on with stores closure. My colleague Michael O’Dwyer writes:

The online business expanded 17pc but UK retail sales at the FTSE 250 company tumbled 10pc as betting shops face the combined challenge of falling high street footfall and the introduction of restrictions on the stakes punters can bet on fixed odds betting terminals (FOBTs), which have been described as the “crack cocaine” of gambling.

You can read his full report here: Ladbrokes owner GVC upgrades profit forecast but still plans to close 900 shops

Analysts: ‘Substantial change’ needed to settle markets

With the FTSE 100 extending its losses and pressure being felt across Europe, let’s take a quick step back.

RBC analysts have taken a wider look at the cocktail of factors afflicting global markets, and their conclusions aren’t the rosiest. They write:

Despite the latest twist and turns, the ‘trade war’ fought mainly by the US is causing a slowdown in global trade and is hitting particularly those countries that act as the workshop for the rest of the globe. This is mainly China and some other South East Asian countries, but also the heavily export-oriented countries of Europe, particularly Germany. The European countries are also feeling the extra strain of the increasingly acrimonious Brexit debate. This is causing a global downswing that manifests itself mainly in the manufacturing sector that produced goods that are heavily dependent on international trade and global demand.

The analysts add:

...we see little that will stand in the way of the current direction of travel for financial markets. We would think that only very large key developments can alter the bigger picture, yet none of these seems in sight in the near term. A substantial change in US trade policies comes to mind, a substantial easing of fiscal policy that eases the pressure on central banks is another. Yet, none of those seems forthcoming at this stage. We thus remain in flattening trades and are considering whether to revise our already low bond yield forecasts even lower.

Explained: What’s going on in Italy, and what does it mean for Europe’s economy?

Despite a poor start out of the gate, the FTSE 100 is now nearer the middle of the pack among Europe’s blue-chip indices.

The biggest faller is Italy’s FTSE MiB, which is down 2.5pc, pushing deeper into lows not seen since June. The country’s financial markets are being rocked by its latest outbreak of political disruptions, as populist Matteo Salvini makes a grab to seize power.

Deputy economics editor Tim Wallace has taken a closer look at the situation, and what it could mean in the long-run for Europe’s fourth-biggest economy. He writes:

Salvini was the driving force behind last year’s bust-up with Brussels. Favouring tax cuts and higher infrastructure spending, he says he wants to boost the economy. The EU worries the extra borrowing would be a serious hazard to Italy’s already teetering debt pile.

A long-standing eurosceptic, he raised the prospect of issuing debts with a sort of parallel currency, raising fears the eurozone’s third-largest economy could ditch the euro.

You can read Tim’s full piece here: How Salvini’s reputation for riling Brussels and the markets could harm Italy’s economy and the euro

Here’s how Italian stocks have looked so far this year:

RBS ex-dividend drop compounded by downgrades

The FTSE 100 is still off more than 1pc, or 83 points, with that substantial drag from Shell making up 24 points of the fall.

The blue-chip index is being weighed upon by miners, but the biggest fallers is Royal Bank of Scotland. As well as being ex-dividend (see 8:44am update), it faced a downgrade from HSBC and Macquarie analysts, who cut their expectations for the bank. UBS and Goldman Sachs both reduced their target price.

If FTSE closes below 7060 I think we are in for a lot of pain - 6800 realistic

— Neil Wilson (@marketsneil) August 15, 2019

Australia’s stock market drop was worst in 18 months

Despite a bright spot in Hong Kong, things looked very doom-and-gloom for much of the Asia-Pacific region during the past day’s trading.

Japanese shares hit a nine-day low, but the biggest loser was Australia, which suffered its worst fall since February 2018.

Its benchmark index, the S&P/ASX 200, closed to 2.85pc.

Australian finance minister Mathias Cormann played down the drop earlier today, saying: “We are heading in the right direction... We are facing some risks in the global economy and in the domestic economy.”

FTSE hits fresh five-month low as Europe sags

European traders aren’t waiting for Donald Trump to fire back. They’re already heading back to the hills, with losses across the board for the continent’s blue-chip indices.

The FTSE has dropped to a six-month low, extending its fall from yesterday.

On Wall Street, futures trading (basically bets on how indices will perform) has taking a turn into the red, meaning it looks like US stocks are set for a drop at open.

Will Trump be goaded into a snap reaction?

After China’s latest salvo in the war of words over trade tensions, all eyes are likely to be on one man in the White House. And, more specifically, what that man’s hands are doing on his phone.

Markets.com’s Neil Wilson writes:

This does bode well and may encourage Trump to react — there is a chance he could bring forward all the tariffs to September 1st. Countermeasures suggests China is not interested in the delay to tariffs — and may have sniffed a weakness in the US position and is keen to exploit it. Retaliation by China means escalation in tensions, and diminishes the chances of a positive outcome in the near term. Risks are still to the downside. As ever, though, only a tweet away.

Fresh worries about trade compound the risk aversion we are seeing due to the macro-economic slowdown and yield curve inversion. The delay to tariffs was about the only bright spot bulls could cling to – the comments from China undermine this positivity and threaten to spook investors again. Hong Kong lowering its growth target does not help.

Beijing low on ammunition to wage a tariff war

Trinh Nguyen, a Natixis economist, says despite China’s words, it has a limited ability to take countermeasures on the tariff front:

China: Will have to take all necessary measures to impose new tariffs.

The amount China has left is ~USD10bn (already imposed 110bn) so not much ammunition & will need curb investment/FX deval/UST/rare earth curb. Chart below ���� US has plenty left & reflects trade diff w/ China. pic.twitter.com/eieW5WF2MM— Trinh Nguyen (@Trinhnomics) August 15, 2019

She adds that the Chinese Finance Ministry’s statement may be an attempt to show strength:

As I always say, WATCH WHAT PEOPLE DO NOT WHAT THEY SAY. Okay, ask yourself, since the multitude of statements, what have happened?

A lot of threats etc. Why? Because it has to sound STRONG to the domestic audience. Right? Have to think from the other person's perspective.— Trinh Nguyen (@Trinhnomics) August 15, 2019

Of course, the counter-argument is that Donald Trump has now repeatedly followed through on threats to introduce tariffs, despite expectations to the contrary.

China kicks back

Trade war tensions appeared to be back with a vengeance, even though Donald Trump delayed some new tariffs on Tuesday.

Here a reminder of what happened then:

Christmas came early for global stock markets after the Trump administration delayed tariffs on some Chinese goods, including laptops and mobile phones, until December 15.

Shares rallied on hopes that US shoppers and Apple will be shielded from higher costs in the run-up to the festive period. Video game consoles, toys, computer monitors and clothes will also be left out of the latest tranche of tariffs, reducing the risk of American consumers feeling the pinch from the trade war.

“We’re doing this for the Christmas season,” President Trump said.

You can read the full details here: Global stock markets rally as Trump plays Santa on tariffs

Despite the festive spirit, new tariffs are new tariffs, and it looks like China plans to respond in kind.

Bloomberg reports the Chinese central bank has just made a substantial cash injection into its banking system, which could mean it is preparing for a protracted trade war.

Hong Kong slashes growth forecast

The Hang Seng index in Hong Kong actually closed up 0.76pc today, bucking recent trends in what may be seen as a dead cat bounce following days of drops.

The financial hub is hugely exposed to trade tensions between the US and China, and is feeling the impact of local demonstrations against a controversial Chinese extradition bill. The city’s international airport was brought to a standstill by protesters twice this week.

Financial secretary Paul Chan said GDP growth is now expected to be between 0pc and 1pc, down from a previous estimate of 2pc to 3pc.

China: US tariff announcement ‘seriously violated’ consensus between countries

Time for a jump scare? The Chinese Ministry of Finance released a statement a few minutes ago that says US plans to place a 10pc tariffs on a further $300bn of goods will derail trade talks between the two economic superpowers.

Beijing says the decision, announced by US President Donald Trump two weeks ago, is a violation of agreements made between Mr Trump and Chinese Premier Xi Jinping. It said “the US side’s move seriously violated the consensus between the heads of state of the two countries”, and vowed countermeasures.

That’s been enough to immediately rattle markets, with Europe now looking distinctly in the red after its flat open. The FTSE is 0.8pc off, with Shell continuing to pull it to underperformance.

Worried about a market downturn? This is how to keep your investments safe

With recession worries running through the global economy, it can be hard to know how to move as an investor.

Telegraph Money’s Richard Evans and Jonathan Jones have taken a look at at what negative-yield bonds and falling equities mean, and prepared a list of the best defensive funds — designed to weather an storm on the markets.

You can read their full breakdown here: Telegraph Defensive 10: our favourite investment funds for protection in falling markets

Amazon Prime Day underpins growth

A big e-commerce boost underpinned that unexpected rise in July retail sales figures, disguising some distinct weakening in the food sector.

The biggest driver was promotional events, suggesting Amazon Prime Day discounts were a strong driver.

Pantheon Macroeconomics’ Samuel Tombs writes:

July’s retail sales figures continue the trend of above-consensus numbers which demonstrate that consumers aren’t fazed by the Brexit deadline. Granted, Amazon's Prime Day, which the retailer has run every July since 2015, probably was chiefly responsible for the colossal 6.9pc month-to-month rise in non-store sales, which made a 0.7 percentage point contribution to growth in total sales. Sales volumes likely will fall back in August, given that some shoppers probably brought forward planned purchases to take advantage of the temporary discounts offered by Amazon.

Food sales drop without World Cup boost

This summer was always going to feel like a downgrade after 2018’s heatwave and football World Cup festivities, and the ONS thinks that may have translated into lower food sales.

This July’s food store sales are down by 0.5%, compared with the same month last year �� ��

This could be in part due to 2018’s prolonged heatwave and special events like the FIFA World Cup ⚽ https://t.co/QFDmkBVf1z— Office for National Statistics (@ONS) August 15, 2019

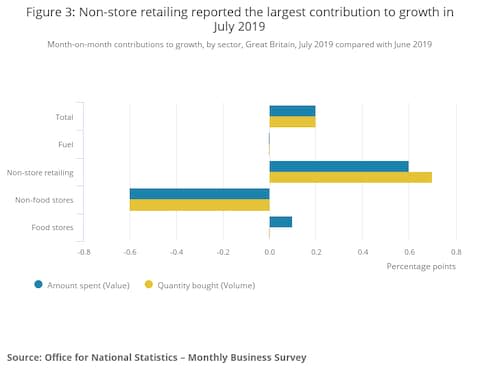

Retail sales beat expectations as department stores rebound

UK retail sales rose by 0.2pc last month as consumers continued to perform above expectations.

A comeback of sorts by Britain’s beleaguered departments stores added to the bounce, with sales growing 1.6pc after half a year in doldrums.

Analysts polled by Bloomberg had expected a 0.2pc drop.

Non-retail sales, likely to primarily mean internet shopping, spiked amid discounting. The ONS said:

Anecdotal evidence suggests that there were a range of promotions in July 2019 from non-store retailers, which boosted sales.

Department store sales increased for the first time this year with a month-on-month growth of 1.6% ��️

This was following six consecutive months of decline https://t.co/IItccpaQ7ipic.twitter.com/1VsYb71Cex— Office for National Statistics (@ONS) August 15, 2019

Here’s how different sectors contributed:

Inverted bonds: Is a recession coming?

Bond yield inversion was at the front of everyone’s minds yesterday (or, at least, everyone following the financial markets).

Traders seized on the US 2yr/10yr bond spread’s negative flip, meaning it was temporarily more lucrative to hold government debts for two years than ten. The relationship is positive again today, but the drop was enough to send shivers down traders’ spines.

The inversion goes against a fundamental tenant of finance: that by reducing the liquidity of your assets (i.e., how quickly they can be turned into cash), you ought to receive a greater payback.

It’s a sign of highly-negative sentiment, and tends to presage an economic downtime: a 2yr/10yr US bond inversion has only not been followed by an American recession once in the past five decades.

There’s still plenty to question, however. Firstly, just because the yield curve is inverted doesn’t mean a recession is coming immediately — historically, downturns have arrived up to 18–24 months after the swing.

In addition, it’s possible the circumstances are different. Speaking to Fox Business Network yesterday, former US Federal Reserve chair Janet Yellen said of the inversion:

Historically, it has been a pretty good signal of recession, and I think that’s when markets pay attention to it, but I would really urge that on this occasion it may be a less good signal. The reason for that is there are a number of factors other than market expectations about the future path of interest rates that are pushing down long-term yields.

Another former Fed Chair, Alan Greenspan, told CNBC “international arbitrage going on in the bond market” was to blame, adding: “There is no barrier for U.S. Treasury yields going below zero. Zero has no meaning, beside being a certain level.”

The UK’s 2yr/10yr spread also flipped, which is less of a sure indicator (it spent most of the 1990s upside-down, for example). Economist Rupert Seggins explains:

1. UK yield curve inversions (10 year Gilt rate higher than 2 year Gilt rate) have been pretty much 50/50 as a recession signal since 1970. Preceded 3, falsely signalled 4 and was late to the party once. Usually tied to some major domestic or global event though... pic.twitter.com/oECE7Sm2DT

— Rupert Seggins (@Rupert_Seggins) August 15, 2019

Another economist, Duncan Weldon, has produced an excellent Twitter thread on the topic of yield curves, and what they mean. I’ll cut to his conclusions here for the sake of space, but it’s well worth reading his full thoughts:

I think a better read of the current pricing is that investors in UK and US longer term bonds think that longer term growth prospects are weak. Not that a recession is imminent.

— Duncan Weldon (@DuncanWeldon) August 14, 2019

Top dog: Metro Bank takes the podium in customer service ranking

There’s been a much-needed bit of good news for struggling challenger lender Metro Bank today — it topped a competition watchdog survey for customer service. My colleague Michael O’Dwyer writes:

The challenger bank shared the top spot with First Direct, the online-only division of the HSBC group. HSBC also took the top spot in a separate survey covering Northern Ireland.

The surveys asked current account holders how likely they were to recommend their bank to friends and family.

Nationwide, Barclays and Lloyds Bank rounded out the top five while Royal Bank of Scotland received the worst score of the 16 banks ranked.

You can read his full report here: Boost for struggling Metro Bank as it tops watchdog’s poll for customer service

Ex-dividend shares weigh on FTSE 100

The FTSE 100, now 0.25pc down, is feeling a significantly drag from a slew of stocks going ex-dividend, including Royal Dutch Shell, Royal Bank of Scotland and Evraz.

Shell, which is listed twice because of its governance structure, is single-handedly taking more than 15 points off the blue-chip index.

When a share is ex-dividend, an investor who buys it will not be entitled to the next dividend payout, meaning it sells at a proportionate discount.

30 points ex-dividend factors for FTSE not helping today - otherwise would be tracking Europe mildly higher

— Neil Wilson (@marketsneil) August 15, 2019

Although the weight will lift tomorrow, the overall picture remains ugly, with traders having fled to safe havens amid yesterday’s rumbles.

Here’s Deutsche Bank’s Jim Reid, with a reminder of why Wednesday’s bond yield curve inversion was particularly spooky for investors.

Although other measures of the US yield curve have progressively inverted over the last few quarters, for me yesterday’s 2s10s inversion is the one that worries me most. In my opinion, it has the best track record for predicting an upcoming recession over more cycles than any of the others.

But CMC Markets’ Michael Hewson points out that conditions may have changed:

An inversion such as this generally tends to support a view that short-term monetary conditions are too tight, and that these short rates need to be lower. That would be an eminently sensible view point if interest rates were at normal levels. As we all know they clearly aren’t at normal levels so it’s difficult to argue that historical precedents apply.

FTSE falls while European markets rise at open

Arguably, the only way was up for European markets this morning, after yesterday’s losses and a quiet day in the United States set the scene for a small bounce.

If there’s been a solid trend for the volatility of the last few weeks, it’s that the FTSE 100 tends to follow the trends of European stocks, only more weakly.

That’s not the case today, however. The FTSE is off about 0.2pc, with the latest Brexit brouhaha likely adding to negative sentiment.

(Reminder that you can use the Markets Hub tool above to check out the latest prices throughout the day)

Round-up: What went wrong on the markets yesterday?

Yesterday was a torrid day across global markets, with the combination of poor German economic data and a major recession warning from the bond market combining to send equities sharply down. Here are the key moments, all from my colleague Tom Rees:

German GDP lands with a thud: Recession fears are mounting in Europe’s biggest economy after it was revealed that German GDP contracted in the second quarter, falling 0.1pc.

Yield curve go negative: The most trusted recession indicator on bond markets finally flashed red as storm clouds gather on the horizon for the global economy.

Markets react: Financial markets around the world tumbled on Wednesday as a slew of ominous data suggested economies are being pushed to the brink of recession by increasing trade tensions.

Indications remain that European stocks are going to open up — just barely — but given how sensitive markets have been lately, gains are likely to be quite fragile.

Oil on the ropes

Brent crude slid 2.97pc yesterday to $59.48 a barrel. Its only a little higher this morning. Traders are worried a general slowdown in the world economy will push down demand for energy.

FTSE 100 called to open up

Will Europe pull out of the global tailspin?

FTSE 100 futures are currently indicating the blue chip index will open up 0.23pc, at 7,110.

One thing to look out for will be ONS retail sales data at 9:30am, which will show how consumer spending held up in July.

Asian markets in the red

The slump on Wall Street continued to Asia overnight, with the Nikkei down more than 1pc and a smaller fall on the Shanghai stock exchanges.

As of 7am UK time, the Hang Seng was in positive territory — but just barely, up 0.1pc. It has wiped off all its 2019 gains in recent weeks amid political disruption.

Agenda: Five things to start your day

Good morning. Today we'll be looking to see if stocks can recover from an ugly day of trade and keeping our eye on upcoming UK retail figures.

1) Fleet Street veteran David Montgomery is on the brink of a comeback with plans to target struggling newspaper publishers in a takeover spree and strip out costs as he attempts to build a new digital giant. Mr Montgomery, 70, is within days of revealing a new listed vehicle set up to make a series of deals.

2) Tim Wallace has taken a deep dive into how Matteo Salvini’s reputation for riling Brussels and the markets could harm Italy's economy and the euro. Mr Salvini is the scourge of migration, the biggest threat to the eurozone and potentially Italy’s next Prime Minister.

3) Sports Direct was thrown into fresh crisis afterits auditor Grant Thornton resigned, casting doubt over the retailer’s future as a listed company should it fail to find a replacement.

4) Rail commuters are set for a 2.8pc hike in fares in January as ticket prices are linked to July’s retail price index measure of inflation. It means a worker with a £3,000 annual season ticket can expect to pay an extra £84 on next year’s travel.

5)Will a no-deal Brexit compel car makers to move overseas? In part 2 of a daily three-part series the future of major British car plants is discussed. Does a mass (Br)exodus await, or will Britain's reputation for engineering excellence discourage vehicle manufacturers from settling elsewhere?

What happened overnight

The growing fears about a world recession sent global stocks sliding in Asia.

Spooked investors stampeded to the safety of sovereign debt and drove yields on 30-year Treasuries to all-time lows at 1.97pc. Yields have now fallen a staggering 60 basis points in just 12 sessions to pay less than three-month debt.

Yields on 10-year paper dropped to 1.55pc, taking them under two-year paper. Such an inversion was last seen in 2007 and correctly foretold the great recession that followed a year later.

Japan's Nikkei was still off 1.5pc but up from early lows, while Shanghai blue chips eased a relatively modest 0.5pc.

MSCI's broadest index of Asia-Pacific shares outside Japan dropped 0.8pc and briefly touched a seven-month low.

In Hong Kong, the Hang Seng Index inched down 0.17 percent or 42.59 points to end the morning at 25,259.69.

Coming up today

Retail sales for July are expected to show a continued bounceback, after June bucked the trend emerging from a downbeat April and May. The sector tends to benefit from hotter weather and major events, which July served up in spades — including Wimbledon, the British Grand Prix and England’s cricket World Cup glory.

“Against that sort of backdrop it would be a surprise if we didn’t see the rebound seen in consumer spending in June,” said Michael Hewson of CMC Markets.

Interim results: Kaz Minerals, Marshalls

Economics: Retail sales figures (UK), productivity, jobless claims, retail sales and industrial production (all US)