News Flash: Analysts Just Made A Notable Upgrade To Their Prothena Corporation plc (NASDAQ:PRTA) Forecasts

Celebrations may be in order for Prothena Corporation plc (NASDAQ:PRTA) shareholders, with the analysts delivering a significant upgrade to their statutory estimates for the company. The analysts have sharply increased their revenue numbers, with a view that Prothena will make substantially more sales than they'd previously expected.

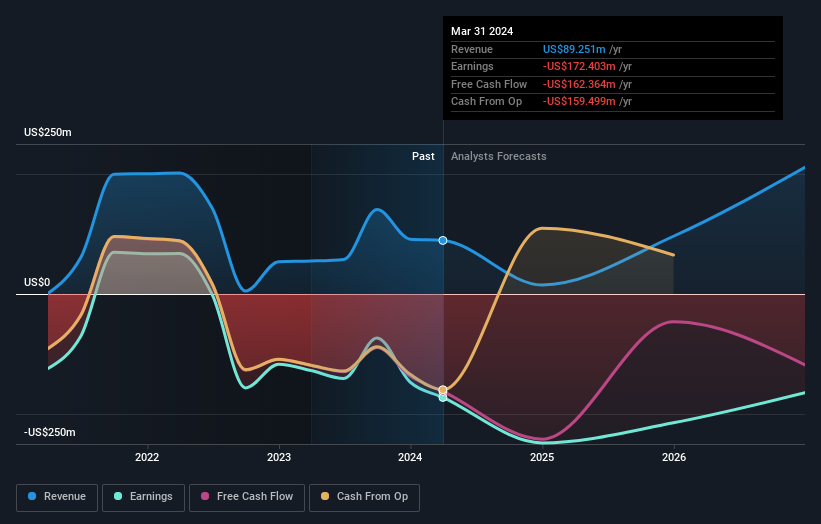

Following the latest upgrade, the current consensus, from the ten analysts covering Prothena, is for revenues of US$15m in 2024, which would reflect a stressful 83% reduction in Prothena's sales over the past 12 months. Per-share losses are expected to explode, reaching US$4.66 per share. However, before this estimates update, the consensus had been expecting revenues of US$13m and US$4.81 per share in losses. We can see there's definitely been a change in sentiment in this update, with the analysts administering a sizeable upgrade to this year's revenue estimates, while at the same time reducing their loss estimates.

Check out our latest analysis for Prothena

There was no major change to the consensus price target of US$63.43, perhaps suggesting that the analysts remain concerned about ongoing losses despite the improved earnings and revenue outlook.

Another way we can view these estimates is in the context of the bigger picture, such as how the forecasts stack up against past performance, and whether forecasts are more or less bullish relative to other companies in the industry. We would highlight that sales are expected to reverse, with a forecast 91% annualised revenue decline to the end of 2024. That is a notable change from historical growth of 40% over the last five years. By contrast, our data suggests that other companies (with analyst coverage) in the same industry are forecast to see their revenue grow 18% annually for the foreseeable future. It's pretty clear that Prothena's revenues are expected to perform substantially worse than the wider industry.

The Bottom Line

The highlight for us was that the consensus reduced its estimated losses this year, perhaps suggesting Prothena is moving incrementally towards profitability. Pleasantly, analysts also upgraded their revenue estimates, and their forecasts suggest the business is expected to grow slower than the wider market. Given that analysts appear to be expecting substantial improvement in the sales pipeline, now could be the right time to take another look at Prothena.

Still, the long-term prospects of the business are much more relevant than next year's earnings. At Simply Wall St, we have a full range of analyst estimates for Prothena going out to 2026, and you can see them free on our platform here..

Of course, seeing company management invest large sums of money in a stock can be just as useful as knowing whether analysts are upgrading their estimates. So you may also wish to search this free list of stocks that insiders are buying.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.