Yahoo Finance

Yahoo Finance Is Now a Good Time to Buy Tech Stocks?

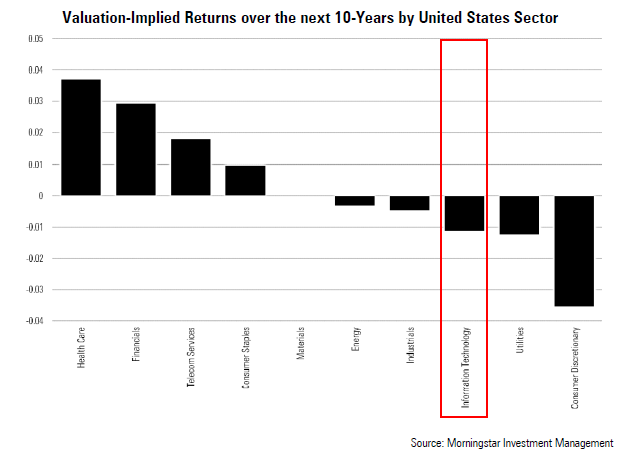

In the United States, we think overvaluations are the biggest risk to investor returns at the current time; especially within some of the most popular sectors such as technology.

Underlying much of the distortion in United States equity values appears to be unrealistic earnings expectations. In tech stocks for instance, the past 10-year earnings growth has equated to 7.65% versus 0.83% for the broader market in real terms. This has resulted in a return-on-equity figure of 20.5% in tech stocks, which is far higher than the 20-year average of 17.9%, and the market average of 14.8%.

Whether these growth rates are sustainable is a source of contention, and is frankly impossible to predict with precision. For instance, with Apple (AAPL), Google (GOOG), Facebook (FB) and Microsoft (MSFT) making up more than 48% of the tech sector, the success of the iPhone 7 will have a material impact on the growth rates and therefore sector fundamentals.

The only rational way to assess the broad range of potential outcomes is to therefore undertake stress-testing when implementing our valuation framework. The key questions are the likely growth rate under a sustainable scenario as well as the broad divergence that could occur in these growth rates.

Admittedly, our methodology allows for higher earnings growth rates in United States technology companies than many other sector, which is a risk in itself, however even under this framework we see the current valuations as unsustainable under most scenarios.

To add a further layer of comprehension, we can consider value in terms of the traditional price-earnings ratio versus a cyclically-adjusted price-earnings ratio (CAPE). This follows the work of Robert Shiller and the numerous academic studies that have generally supported the CAPE over traditional P/E ratio analysis. As can be seen below, this also shows similar distortions in United States equities by sector. Investors should note that the energy sector is impacted by the commodity slump and the subsequent fall in earnings.

Overwhelmingly, a rationally positioned investor should see these overvaluation concerns as a fundamental risk. With total returns on offer of only 1.1% across the United States equity index, according to our valuation-implied methodology, and negative valuation-implied returns in five of the key sectors, we would suggest a very cautious stance is warranted towards United States exposure.

Why Going Passive for Global Stock Exposure is Dangerous

With the United States now comprising just over 57% of the global index, there is a growing theme around active versus passive equity selection. One growing strategy is to run a core/satellite portfolio to keep fees low, whereby the majority of equity exposure is taken via a passive exposure, then using an active satellite theme to increase the valuation opportunities. Keeping fees low is a principle Morningstar takes very seriously, however the acceptance of a high United States equity exposure adds a layer of fundamental risk many investors are ignoring. More specifically, the greatest risk to a portfolio is a substantial drawdown which impairs value and results in a permanent loss of capital.

In essence, and in summary, while we are generally supporters of low-cost passive investing, we do not believe passive global equity selection is desirable under a backdrop where 57% of the global index has a poor fundamental backdrop.