Yahoo Finance

Yahoo Finance One indicator to rule them all - the F-Score

Many stock market traders follow “momentum” strategies that focus on buying stocks in line with the trend in their price movements. Prices have strange but predictable behaviour… a price that has been moving up in the recent past has a strong tendency to continue moving up in the near future. Trend trading has been show in dozens of research papers and in the fortunes of many traders to work incredibly well.

But while traders have developed a legion of indicators, such as relative strength or moving averages, to spot companies showing momentum in a company’s price rarely have they developed or understood indicators that highlight the momentum in a company’s fundamentals. Surely if such an indicator existed it would also have some kind of predictive quality?

The truth is that just such an indicator does exist and a body of research is now building that show it to be an astonishingly predictive indicator of long term company health and share price movements. But in spite of this, it is still largely misunderstood or ignored by most investors.

Enter Fundamental Momentum

The indicator in question is known as the F-Score and its origin I will explain shortly. It is extremely simple to calculate for a single company as it’s a checklist of nine rules that a company either passes or fails to create a score between zero and nine (see the bottom of this page for details). Each of these rules looks at one aspect of a company’s financials, with six of the nine rules looking at the change in a company’s financials. Whereas most ratios look solely at a company’s current financial state, the F-Score looks more deeply into the direction in which it’s financial state is moving, and herein lies it’s secret sauce - it captures fundamental momentum in a single number. (See this article on How to calculate the F-Score).

It was developed by Josef Piotroski, a Stanford Finance Professor, in the 1990s who wished to figure out how to separate the wheat from the chaff amongst bargain stocks. In the bargain basement of the stock market there is a huge variability of returns as when stocks get beaten down they either recover magnificently, dawdle or just go dramatically bust. Piotroski developed the F-Score to discover which companies in this segment of the market were most likely to recover, with astonishing results.

Piotroski’s classic strategy, which Stockopedia models here, is to take the cheapest segment of the stock market and only buy the stocks that rank 8 or 9 on his F-Score indicator. Over a 20 year backtest he showed that the average “return earned by a high book-to-market investor can be increased by at least 7.5% annually”. Furthermore, he found that buying the top stocks in the market and shorting those that got the worst scores would have resulted in 23% annualized gains, more than double the S&P 500 broad market index return!

While, the original paper was enormously influential the F-Score was in danger of being siloed off as a bargain stock eccentricity, but as time went by it became championed in an increasing number of research papers and experiments by the top tier of investment banks. It seems by applying a high F-Score filter to a wide variety portfolio of stocks the returns can be significantly improved and often the risk diminished.

The higher the F-Score the better

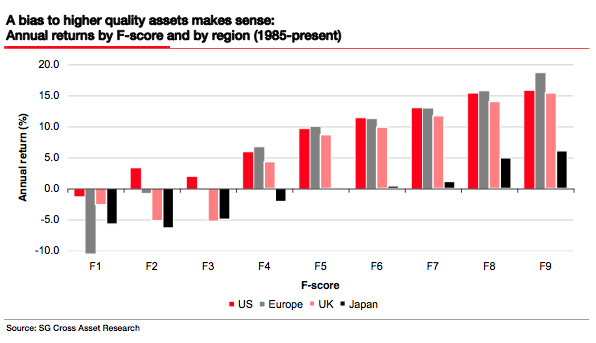

The Societe Generale equity research team have been big fans of the F-Score since James Montier championed it a few years ago, but Andrew Lapthorne, their current top rated quant analyst, has seriously investigated it in several papers and provided a great body of work into it’s effectiveness. He has provided strong evidence that independently of valuation the higher the F-Score (or quality) of a stock the greater the return. I borrow a chart from one of his research papers to indicate the extent to which high F-Score stocks dramatically outperform the market and low F-Score stocks underperform.

Not only that but in the US, Europe and the UK Soc Gen have found that in 4 out of every 5 years high F-Score stocks beat the market. Clearly having a large bias towards higher F-Score stocks in your portfolio makes sense.

Short Seller’s dream - Piotroski found that weak stocks, scoring two points or less, were five times more likely to either go bankrupt or delist due to financial problems. The Soc Gen research above confirms that low F-Score stocks (0–3) do underperform dramatically and James Montier used this criteria in conjunction with high valuations as a key part of his ‘Unholy Trinity’ Short selling strategy which we are currently modelling at Stockopedia. It has dramatically underperformed the market this year (–19.9% underperformance year to date). Clearly avoiding these kinds of stocks makes a lot of sense!

Bear Market Protector - 2008 was one of the worst markets on record for stocks, almost every market participant saw dramatic losses across their entire portfolio. The American Association of Individual Investors, similarly to Stockopedia, tracks many famous strategies and has been doing so since 1999. Their model of Piotroski’s low Price to Book strategy was the only strategy which posted positive absolute returns that year. In fact, since it’s inception AAII’s Piotroski strategy has shown an average annualised return of 24.9% versus only a 2.6% return for the S&P 500, indicating that high F-Score stocks can be an excellent bear market protectors.

A Secret Sauce for any Strategy?

The great thing about the F-Score is that it essentially is an entire quality and fundamental momentum screen in a single number. Applying it as a filter on top of almost any strategy can help to increase returns and reduce risk. This has been confirmed in a pair of research notes one from Soc Gen and another from Morgan Stanley which have used the F-Score in conjunction with both Value and Income strategies to remarkable effect.

The Magic Scormula - Teun Draaisma was a heralded equity strategist at Morgan Stanley for many years where he launched the tracking of a long-short ‘Combo’ strategy. The rationale of the ‘Combo’ strategy was to identify cheap (or expensive) stocks with strong (or weak) financial health as potential long (or sell) ideas, by combining the best of both Joel Greenblatt’s Magic Formula with Piotroski’s F-score as the bear market continued to unfold. They found the portfolio outperformed in 17 out of 19 years with an average 12.3% gain. The maximum drawdown was 5% and performed extremely well in bear markets. Essentially this strategy is similar to the long only ‘Nifty Thrifty’ version popularised by Richard Beddard for Money Observer - we are tracking a version for UK investors here which again is outperforming the market by a distance.

Quality Income - Soc Gen’s own proprietary ‘Quality Equities’ strategy is a meshing of the F-Score with a bankruptcy risk filter that has performed astoundingly well in backtests since 1989 with an over six-fold return. But it’s not been a patch on the returns generated when quality is meshed with higher yielding stocks. Their Quality Income strategy which I have previously written about has returned over 11 fold in backtests since 1989 and is now marketed as an ETN under the ticker SGQI. We model our version of this Quality Income portfolio here.

A few issues and caveats

Whenever anyone starts harping on about a cool new financial indicator that beats all others its worth putting on the skeptics hat. Soc Gen's research has highlighted a few downsides that promote at least a fair bit of caution.

In spite of these caveats, you would think that such a predictive indicator would have a massive following, but I have spoken to several long-short hedge funds in recent weeks and have been astonished to find out that they have never heard of the Piotroski F-Score. Could it be that the vast majority of the fund management industry is so busy making themselves appear busy by meeting company management teams again and again that they have no time to apply themselves to the kind of quantitative edges that could make their investment results that much better! As an individual you don’t have to make the same mistakes.

We provide F-Scores for every company in the UK Market as a key part of our Stock Reports. Both as a fundamental meter and as a popup checklist. This has never before been available in such detail on the web. If you want to research any stock in the UK market based on the F-Score you can take a free trial to Stockopedia.

Example of the Stockopedia Piotroski Checklist Popup - available for all stocks:

Read More about value investing on Stockopedia

See the latest Stockmarket News, Commentary & Analysis on Stockopedia