Oracle Is Navigating the AI Revolution With Cloud Momentum

Oracle Corp. (NYSE:ORCL), a global leader in enterprise software and cloud computing solutions, was founded in 1977. The company excels in developing and marketing database software and technology, cloud-engineered systems and enterprise software products, particularly its own brands of database management systems.

Originally an enterprise software database giant, Oracle has transitioned to the cloud over the past 10 to 15 years and is now poised to tackle the artificial intelligence revolution. As such, the company presents a compelling investment opportunity amid its impressive momentum in AI and cloud businesses.

Despite tight competition, Oracle has delivered high double-digit growth in both areas recently. As a legacy database provider, its database solutions have become a key competitive advantage against industry peers, strengthening its position in the cloud business. Oracle offers a comprehensive and fast cloud solution for deploying AI, boasting the fastest infrastructure in the industry, backed by Nvidia (NASDAQ:NVDA) hardware.

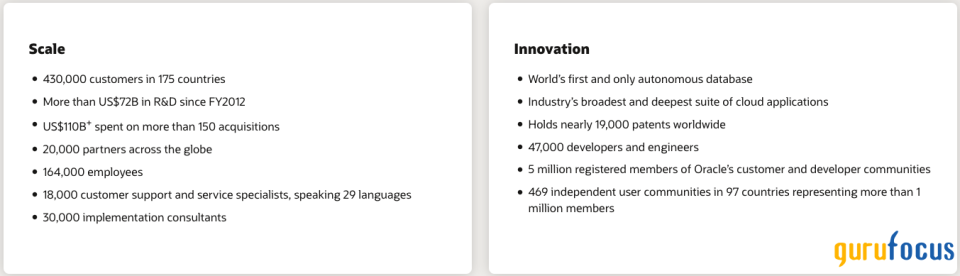

Source: Oracle Investor Relations

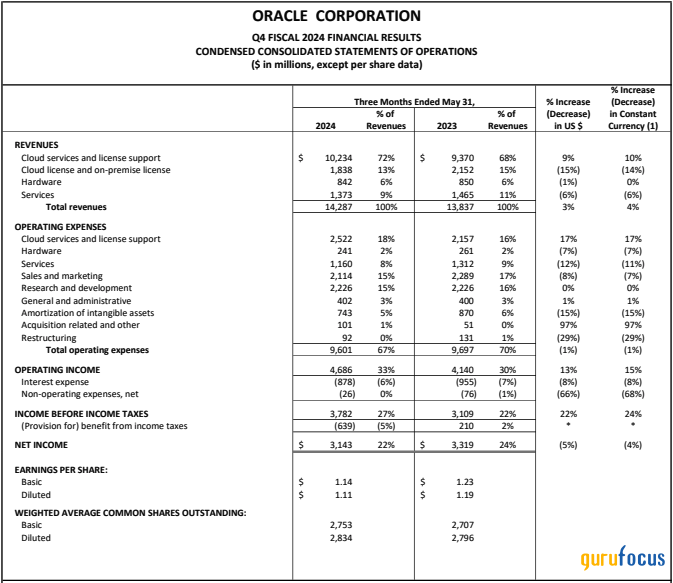

Oracle reported its fiscal fourth-quarter 2024 earnings on June 11. Quarterly earnings of $1.63 per share narrowly missed estimates by 1.20%. Revenue of $14.29 billion also missed expectations by 1.90%. Despite these misses, the stock price surged due to growth in the remaining performance obligation, which has remained resilient despite the deceleration in the company's cloud infrastructure growth rate.

Significant deals with Alphabet's (NASDAQ:GOOG) Google, OpenAI and Microsoft (NASDAQ:MSFT) around Oracle Cloud Infrastructure also contributed to this positive sentiment. Oracle's earnings growth was complemented by strong margins, with the adjusted operating margin and adjusted Ebitda margin expanding to 44% and 55%, respectively, highlighting the scalability of OCI across its operations. I believe Oracle can sustain this exceptional growth rate as it continues to build larger data centers.

Year to date, Oracle has outperformed the S&P 500 by over 20%, with the stock yielding more than 35% compared to the S&P 500's 17% increase.

The company's expanded partnership with Microsoft and other cloud computing providers is expected to enhance the expansion and reach of its leading database management services. Given its smaller scale compared to Microsoft Azure, Amazon Web Services and Google Cloud, Oracle must capitalize on multi-cloud adoption opportunities to justify its premium valuation.

Strategic moves

Oracle's transformation is certainly pushing the boundaries of what the company can achieve, with the primary growth constraint being the speed at which it can establish new data centers. Despite missing both top and bottom-line estimates in the fourth quarter, the stock surged over 13% post-earnings release.

This surge was driven by the impressive growth in Oracle's RPO, which grew 44% year over year to an astounding $98 billion and increased by $18 billion from the third quarter. Management expects 39% of this amount, or about $38.20 billion, to materialize in the next 12 months. The significant contracts signed in the third and fourth quarter, driven by the unrelenting AI demand, marked the largest sales quarters in Oracle's history.

Source: Oracle's Investor Relations

Throughout the year, the company secured pivotal deals with industry giants OpenAI, Google and Microsoft. These contracts are crucial as they involve leading names in the AI space that are poised to dominate in the coming years. OpenAI, the entity behind the AI revolution with ChatGPT, signed on to run deep learning and AI workloads on the Oracle OCI. Oracle reported that a total of 30 AI contracts were signed in the fourth quarter, valued at over $12 billion. For these projects, the company will utilize cutting-edge Nvidia chips, interconnect network solutions and liquid cooling to train neural networks. Management also announced the construction of four large data centers for this initiative, potentially incorporating Nvidia's new Blackwell GPUs.

Additionally, Oracle entered a partnership with Google to offer OCI database services through Google Cloud, planning to build 12 OCI data centers within Google Cloud. The company also advanced its collaboration with Microsoft, with 11 of the planned 23 OCI data centers within Microsoft Azure already operational. During the earnings call, there were hints of a potential future partnership with Amazon's (NASDAQ:AMZN) AWS. With the global shift towards multi-cloud adoption, a deal with AWS would not be surprising. These strategic moves demonstrate Oracle's strong positioning to capitalize on the AI boom through its data centers.

Flexibility and scalability in cloud services

Oracle is also offering private OCI for enterprises looking to leverage its cloud services within their own data centers. As outlined in the earnings call, customers will not pay for hardware, but only for consumption costs, with the ability to scale services as needed for training large language models and neural networks. This flexibility is expected to drive scalable revenue generation for Oracle. Its multi-cloud integration and adaptable cloud services position it as a versatile and comprehensive solution for various enterprise needs.

Further, its Gen2 AI Cloud Infrastructure currently faces demand that far exceeds supply. The company's legacy as a database provider gives it a competitive edge, allowing it to leverage its position in the cloud business. Oracle's capital expenditure guidance for 2024, ranging between $7 billion and $7.50 billion, reflects the increasing demand for Oracle Cloud. This includes growing demand in national security and European Union sovereign regions. While Oracle's infrastructure as a service is in growth mode, its profitable legacy platform supports its overall profitability, enabling competitive pricing for its cloud offerings.

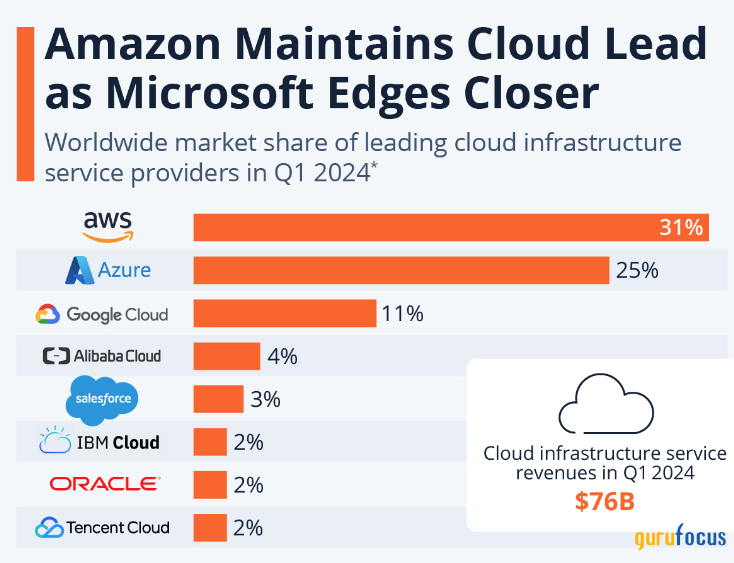

Source: Statista

With only a 2% market share in the cloud market, Oracle has substantial room to grow and capture share from competitors like Amazon, Microsoft and Google, the top three players in the field. Recent quarters have seen the company growing its cloud revenue at a faster pace than its main competitors, indicating a strong growth trajectory.

Business performance and outlook

Despite the quarterly earnings misses, Oracle's standout performer was the cloud infrastructure segment, which saw revenue jump 42% year over year. The Cloud Application segment also registered growth, reaching $3.30 billion, a 10% increase. Non-GAAP operating margins showed significant strength, increasing 47%.

For the full year, Oracle reported total revenue of $53 billion, a 6% increase, with non-GAAP operating margins at 44%. It generated $5.56 in non-GAAP earnings per share.

Source: Oracle's Investor Relations

Looking ahead to fiscal 2025, I anticipate exceptional top-line growth as Oracle continues to build out regional AI factories and expand embedded OCI services in Azure data centers. The company has carved out a niche with its automated OCI services, which are poised to grow as quickly as data centers can be constructed. Management projects strong sequential growth for the year as OCI capacity scales to meet demand, with cloud infrastructure services expected to increase 50%. They also reiterated their fiscal 2026 revenue goal of $65 billion, though they now believe this target may be conservative given the accelerated growth momentum seen in 2024. This target seems achievable given the rapid growth across OCI infrastructure and services.

Margin analysis

There has been some tightening on the margin side due to significant investments to meet the surging demand for Oracle's second generation AI Cloud infrastructure. I expect margins to improve as the company works through its backlog of orders. As the top-line growth continues, I foresee margins scaling and expanding due to the company's automated, modular data center capacity. Additionally, given the recent data breach by one of Oracle's cloud database competitors, there may be opportunities to capture additional market share that were previously unavailable.

Capital expenditures and free cash flow

A key takeaway from the fourth-quarter earnings report was the management's update on capital expenditure spending. For the year, capital expenditures amounted to nearly $6.90 billion. During the earnings call, management stated they expect capex spending to double in fiscal 2025, reaching nearly $14 billion, significantly higher than the earlier prediction of $10 billion.

While this figure is substantial, Oracle's cash flow statement shows it has become a free cash flow-generating machine. In 2024, Oracle generated $11.80 billion in free cash flow, a 39% growth. Although FCF growth slowed compared to 2023's 68%, the absolute magnitude of the cash flows should alleviate concerns about the company's capital expenditure.

Investors should keep an eye on capex spending, but Oracle's ability to generate significant free cash flows, combined with its focus on major AI players as customers, mitigates some of the concerns surrounding the high figure.

Valuation analysis

Oracle currently trades at a forward price-earnings ratio of about 22, aligning with some peers such as Salesforce (NYSE:CRM) (22.30) and Alphabet (22.10), but more attractively priced compared to others like Microsoft (33) and Workday (NASDAQ:WDAY) (28.40).

Historically, Oracle has traded at lower multiples, but the recent surge in positive developments, particularly partnerships with AI giants like OpenAI, Alphabet and Microsoft, has justified a higher multiple. These strategic partnerships have significantly boosted the company's growth potential, particularly in the AI and cloud infrastructure space. Given the company's trajectory, I believe a forward earnings multiple of 22 is appropriate. The company has demonstrated robust earnings per share growth, recording an 8.60% increase, which is close to its fiscal 2026 target of over 10%.

With a forward PEG ratio of approximately 1.80 and considering management's earnings growth target of 10% by 2026, we can adjust our valuation assumptions accordingly. This adjustment yields an adjusted PEG ratio of around 2. If Oracle achieves this growth target in 2025, the projected EPS would be around $6, aligning closely with the analyst consensus of $6.30. Using a forward price-earnings ratio of 22, this would result in a price target of $135, roughly matching the current trading levels and implying a potential downside of about 5%.

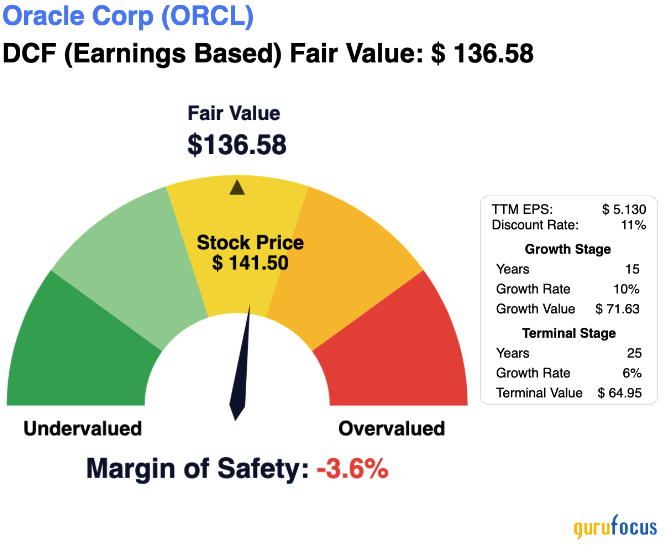

To further validate the valuation derived from the price-earnings multiple approach, a discounted cash flow analysis can be employed. Using a discount rate of 11% and aligning with management's 10% growth estimate through 2026, the DCF valuation also does not provide a sufficient margin of safety to recommend the stock at current levels.

While Oracle's growth is commendable, particularly in cloud infrastructure and AI, it faces stiff competition from companies like Microsoft, whose Azure and intelligent cloud offerings are better positioned. Microsoft's superior growth in these areas highlights the competitive challenges the company must navigate. Given that Oracle's stock has already surged over 15% following its impressive earnings release and is up over 35% year to date, the current valuation reflects much of the positive developments.

Given the little to no upside potential at the current price levels, I am maintaining my hold rating on Oracle. The stock has already incorporated significant gains, and while its partnerships and growth in AI and cloud infrastructure are promising, the current valuation does not present a compelling entry point for new investors.

Final thoughts

Oracle stands at the forefront of the AI and cloud computing revolution, leveraging its legacy as a database provider to drive growth in these burgeoning sectors. The company's strategic partnerships with key players in the AI space, coupled with its robust financial performance and free cash flow generation, position it well for future expansion.

However, given the current valuation levels, which already account for much of the anticipated growth, the stock appears fairly priced with limited immediate upside potential. Thus, while Oracle's long-term outlook remains strong, I advise investors to watch for more attractive entry points in the future.

This article first appeared on GuruFocus.