Yahoo Finance

Yahoo Finance Pension choice for 130,000 Tata steel workers

Last week, 130,000 current and former steelworkers received letters asking them to make a tough decision about the future of their pensions.

The letters, seen by Telegraph Money, ask savers to pick between sticking with the existing British Steel scheme, which will fall into the Pension Protection Fund (PPF), the “lifeboat” scheme for “final salary” plans, or moving to an entirely new arrangement.

While there is a helpline, phone handlers are not allowed to tell savers which option is better for them. If they choose to do nothing, their pensions will default into the PPF.

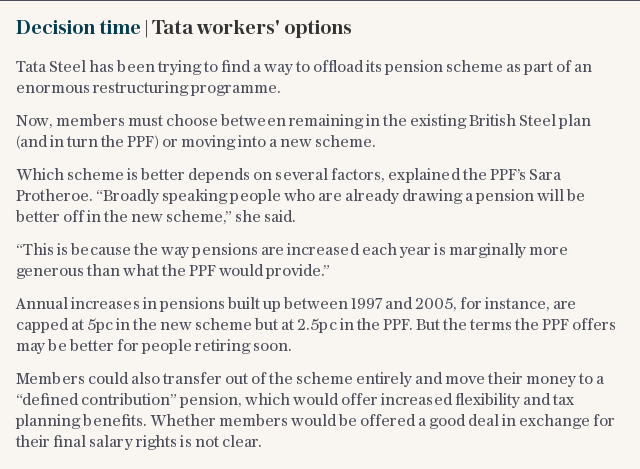

But the PPF itself admits that some groups, including around 90,000 retired members, are likely to get a better deal by opting for the new steel scheme. Which option is better for staff is determined by their personal circumstances and retirement plans (see box, below).

The decision facing steelworkers comes fast on the heels of a similar question asked of former staff of BHS, the failed retailer.

After months of talks between the Pensions Regulator, the PPF and former owner Sir Philip Green, who was called the “unacceptable face of capitalism” by MP Frank Field, staff had to choose between the PPF and a new scheme without an employer behind it.

Britain’s thousands of final salary schemes have been under intense pressure as rising life expectancy and falling bond yields have caused funding deficits to balloon over recent years.

High-profile cases such as Tata Steel and BHS forced politicians and regulators to intervene. In the vast majority of cases, when a company collapses, its pension fund falls into the PPF and staff are not given an alternative. There have been only two other comparable cases where major restructuring deals have given members a choice: the photography firm Kodak and the engineering company Halcrow.

As final salary pensions become increasingly unaffordable, experts fear that more savers will be forced to make a choice.

“This won’t be the last time that pension scheme members are presented with unpalatable choices involving benefit cuts,” said Tom McPhail of Hargreaves Lansdown, the investment firm.

“It is unrealistic to expect all final salary pension schemes to pay out all promised pensions to all their members. The challenge is to manage these situations in a way that is fair to everyone and secures the maximum possible payout to members.”

What is the Pension Protection Fund?

Before the PPF was established in 2005, savers could find themselves left with nothing if the employer behind their final salary scheme went bust.

The PPF also runs the Financial Assistance Scheme, which helps some members of schemes that began to wind up between January 1997 and April 2005. The PPF works like an insurance plan, with schemes paying a levy to cover members in the event that the scheme can no longer pay out.

If your scheme falls into the PPF and you are already retired, your pension will be paid at exactly the same level. If you are yet to retire, payments are capped at 90pc of the promised rate.

However, high earners – not yet retired – face a substantially bigger loss. There is an overall cap on compensation, currently £38,505 for a 65-year-old, or £34,655 where the 90pc cap applies. Savers with long service get special protection: the cap is increased by 3pc for each full year of service above 20 years, up to a maximum of double the usual cap.