Yahoo Finance

Yahoo Finance Questor: Hargreaves is the investment platform to buy as the Neil Woodford effect lingers

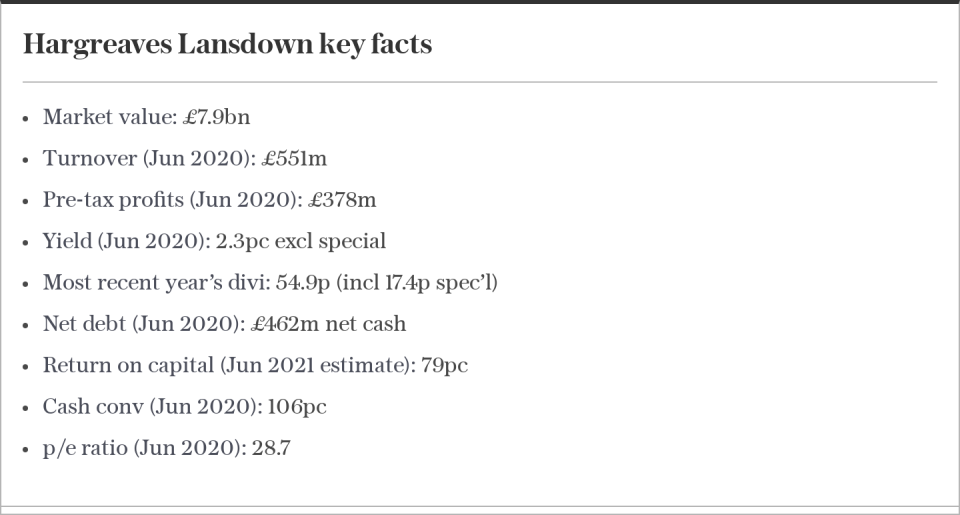

Hargreaves Lansdown’s shareholders cared more about its involvement with Neil Woodford than its customers did, it seems.

Shares in the investment shop stand 27pc below their level just before the suspension of the Woodford Equity Income fund in June 2019, while shares in rival firms AJ Bell and IntegraFin have risen by 10pc and 39pc respectively. But Hargreaves still managed to attract 220,000 new customers last year to take its total to 1.4m.

Despite this vote of confidence by the people who matter, investors’ apparent anxiety about the Woodford connection has meant that readers who followed Questor’s advice to buy Hargreaves shares in January 2017 have made only a modest 24pc, whereas IntegraFin has gained 82pc since our tip in December 2018 while AJ Bell’s shares have risen almost threefold over the same period, annoyingly for this column in view of our decision to bank a quick 50pc profit just weeks after our “buy” advice.

We did so on the grounds of valuation, although these three companies fall into the enviable category of businesses that can grow sustainably with minimal need for capital and at very high profit margins. This is a potent mix that offers the opportunity for long-term compounding of returns – and there is no better way for patient readers of this column to grow rich. It also means that, within reason, a high multiple of earnings is no reason to avoid the shares.

The key attribute of these businesses is that their revenues can grow while their costs remain broadly fixed. Once they have built the platform that allows customers to trade and hold shares and funds, their costs are little more than those of running a call centre.

Meanwhile, there are several avenues to rapid growth. These firms make a percentage of the value of the assets that their customers own on their platforms, so signing up more customers, more investment from existing ones and investment growth when markets rise all contribute.

Sign up to our Business Briefing newsletter for a snapshot of the day’s biggest business stories

Read Questor’s rules of investment before you follow our tips

There is every reason to expect more customers to sign up. With each year that passes, fewer workers benefit from final salary pension schemes and are forced to save for their own future. Many existing customers naturally pay in more money to their Isas and pensions on these platforms every year, while fewer cash in their pensions in their entirety for annuities following the introduction of the pension freedoms in 2015.

America is ahead of Britain in this respect and gives some idea of the scope for growth in personal investment here.

“About 3m DIY savers invest via platforms in Britain now, whereas in America Charles Schwab has 30m and Fidelity something similar,” said Ben Needham of Ninety One, who owns stakes in Hargreaves and AJ Bell in his UK Equity Income fund, while other funds run by his firm invest in IntegraFin.

“Probably one in five or six Americans invest, whereas here it is one in 20. So there is evidence that the market in the UK is only in its embryonic stages.”

Platforms can also make money from share dealing commission and from new lines of business such as “active savings” services, which allow customers to move money from one bank to another in search of higher interest rates with the same ease with which they can switch from one fund to another.

Share dealing and the savings services both offer ways to attract new, younger customers – customers who will often in time invest in Isas and pensions and start to accumulate large sums.

The three firms, two of which, AJ Bell and IntegraFin, update on trading next week, have different mixes of clients. Hargreaves concentrates on individuals who look after their own money while IntegraFin services financial advisers; AJ Bell does both.

AJ Bell’s shares are most highly valued at a forecast price-to-earnings ratio in the low 40s. Hargreaves is in the high 20s and IntegraFin is in between. AJ Bell’s rating reflects greater growth prospects both for the assets it looks after and for its profit margins.

Although we sold far too early we don’t see a compelling reason to go back into the stock at a much higher price; IntegraFin is a hold but for new money our pick is Hargreaves, whose shares still seem unfairly punished by the lingering association in investors’ minds with Mr Woodford.

Questor says: buy Hargreaves Lansdown, hold IntegraFin

Ticker: HL., IHP

Share price at close: £16.59, 540p

Read the latest Questor column on telegraph.co.uk every Sunday, Tuesday, Wednesday, Thursday and Friday from 5am.