Yahoo Finance

Yahoo Finance Is Rapala VMC (HEL:RAP1V) Using Too Much Debt?

Warren Buffett famously said, 'Volatility is far from synonymous with risk.' It's only natural to consider a company's balance sheet when you examine how risky it is, since debt is often involved when a business collapses. As with many other companies Rapala VMC Corporation (HEL:RAP1V) makes use of debt. But should shareholders be worried about its use of debt?

When Is Debt Dangerous?

Generally speaking, debt only becomes a real problem when a company can't easily pay it off, either by raising capital or with its own cash flow. Ultimately, if the company can't fulfill its legal obligations to repay debt, shareholders could walk away with nothing. However, a more frequent (but still costly) occurrence is where a company must issue shares at bargain-basement prices, permanently diluting shareholders, just to shore up its balance sheet. Of course, the upside of debt is that it often represents cheap capital, especially when it replaces dilution in a company with the ability to reinvest at high rates of return. When we think about a company's use of debt, we first look at cash and debt together.

View our latest analysis for Rapala VMC

How Much Debt Does Rapala VMC Carry?

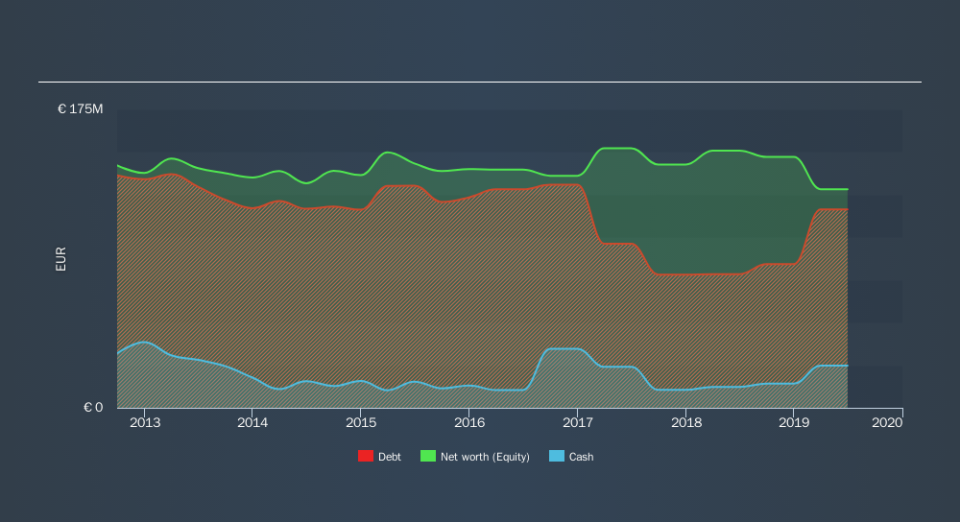

As you can see below, at the end of June 2019, Rapala VMC had €116.3m of debt, up from €78.4m a year ago. Click the image for more detail. However, it does have €24.7m in cash offsetting this, leading to net debt of about €91.6m.

A Look At Rapala VMC's Liabilities

According to the last reported balance sheet, Rapala VMC had liabilities of €122.8m due within 12 months, and liabilities of €66.4m due beyond 12 months. Offsetting these obligations, it had cash of €24.7m as well as receivables valued at €61.4m due within 12 months. So its liabilities total €103.1m more than the combination of its cash and short-term receivables.

This deficit is considerable relative to its market capitalization of €111.1m, so it does suggest shareholders should keep an eye on Rapala VMC's use of debt. Should its lenders demand that it shore up the balance sheet, shareholders would likely face severe dilution.

In order to size up a company's debt relative to its earnings, we calculate its net debt divided by its earnings before interest, tax, depreciation, and amortization (EBITDA) and its earnings before interest and tax (EBIT) divided by its interest expense (its interest cover). The advantage of this approach is that we take into account both the absolute quantum of debt (with net debt to EBITDA) and the actual interest expenses associated with that debt (with its interest cover ratio).

Rapala VMC's net debt is 4.8 times its EBITDA, which is a significant but still reasonable amount of leverage. But its EBIT was about 12.4 times its interest expense, implying the company isn't really paying full freight on that debt. Even if not sustainable, that is a good sign. Unfortunately, Rapala VMC's EBIT flopped 17% over the last four quarters. If earnings continue to decline at that rate then handling the debt will be more difficult than taking three children under 5 to a fancy pants restaurant. The balance sheet is clearly the area to focus on when you are analysing debt. But it is future earnings, more than anything, that will determine Rapala VMC's ability to maintain a healthy balance sheet going forward. So if you want to see what the professionals think, you might find this free report on analyst profit forecasts to be interesting.

Finally, while the tax-man may adore accounting profits, lenders only accept cold hard cash. So we always check how much of that EBIT is translated into free cash flow. Over the last three years, Rapala VMC actually produced more free cash flow than EBIT. There's nothing better than incoming cash when it comes to staying in your lenders' good graces.

Our View

We feel some trepidation about Rapala VMC's difficulty EBIT growth rate, but we've got positives to focus on, too. For example, its interest cover and conversion of EBIT to free cash flow give us some confidence in its ability to manage its debt. When we consider all the factors discussed, it seems to us that Rapala VMC is taking some risks with its use of debt. While that debt can boost returns, we think the company has enough leverage now. Above most other metrics, we think its important to track how fast earnings per share is growing, if at all. If you've also come to that realization, you're in luck, because today you can view this interactive graph of Rapala VMC's earnings per share history for free.

If, after all that, you're more interested in a fast growing company with a rock-solid balance sheet, then check out our list of net cash growth stocks without delay.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned. Thank you for reading.