Yahoo Finance

Yahoo Finance Reasons Why Investors Should Avoid Illinois Tool Stock Now

Illinois Tool Works Inc. ITW seems to have lost its sheen due to weakness in auto production, high debts, forex woes and other company-specific headwinds.

The manufacturer of highly engineered products and specialty systems currently carries a Zacks Rank #4 (Sell).

The company belongs to the Zacks Manufacturing – General Industrial industry, which is at the bottom 25% (with the rank of 191) of more than 250 Zacks industries. We believe that the industry is suffering from adverse impacts of global uncertainties, unfavorable movements in foreign currencies, weakness in industrial production in the United States, and cost escalation due to tariffs, commodity inflation, high labor costs and freight charges.

It is worth noting that Illinois Tool’s second-quarter 2019 results were better than expected, with earnings surpassing estimates by 1.5%. However, the bottom line suffered from weak revenues, high restructuring expenses, forex woes and divestiture-related loss.

A glance at the company’s price trend in the past six months shows that it has lost nearly 4% compared with the industry and S&P 500’s declines of 5.8% and 0.3%, respectively.

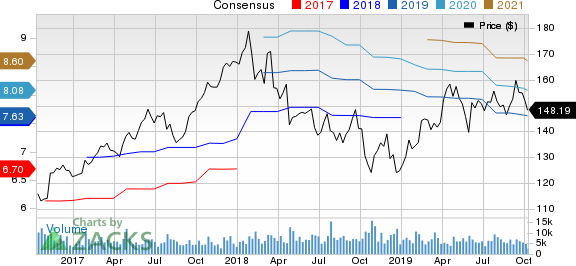

Its earnings estimates were lowered, reflecting bearish sentiments. Over the past 90 days, the Zacks Consensus Estimate for Illinois Tool’s earnings has declined 3% to $7.64 for 2019 and has moved down 3.5% to $8.10 for 2020.

Illinois Tool Works Inc. Price and Consensus

Illinois Tool Works Inc. price-consensus-chart | Illinois Tool Works Inc. Quote

Factors Hurting the Stock’s Performance

Top-Line Weakness: Illinois Tool is bearish about its organic sales performance for 2019 mainly due to concern over demand level. It predicts organic sales to decline 1-3%, down from growth of 0.5-2.5% mentioned previously. Total revenues are believed to be $14.3-$14.5 billion, down from previously stated $14.5-$14.8 billion.

Notably, the company’s Automotive OEM organic sales in the second quarter of 2019 suffered from the fall in auto builds in China, North America and Europe. Also, businesses were weak in Food Equipment, Test & Measurement and Electronics, Polymers & Fluids, Welding, Construction Products, and Specialty Products segments.

Poor Bottom-Line Projection: Illinois Tool’s concerns related to its organic sales had adverse impacts on the bottom-line projection too. For 2019, the company predicts earnings of $7.55-$7.85 per share, with $7.70 as the mid-point. The guidance is below the previously mentioned $7.90-$8.20, with $8.05 as the mid-point.

The company noted that the revised earnings guidance accounts for adverse impacts of 35 cents related to organic sales weakness as well as 25 cents of higher restructuring and forex-related headwinds.

Forex Woes: Geographical diversification exposed Illinois Tool to headwinds arising from geopolitical issues, macroeconomic challenges and unfavorable movements in foreign currencies. In second-quarter 2019, forex woes hurt sales by 2.7% and earnings by 6 cents per share. Also, the company suffered from weak business in China, Europe and the Asia Pacific.

For the second half of 2019, Illinois Tool predicts combined auto builds in China, Europe and North America to decline roughly 5%. Forex woes are predicted to adversely influence 2019 results.

Highly-Leveraged Balance Sheet: High debts can be concerning for Illinois Tool as it raises financial obligations and might adversely impact profitability.

The company’s long-term debt rose 0.3% (CAGR) in the last five years (2014-2018). Exiting second-quarter 2019, its long-term debt was approximately $ 7,809 million, up 29.5% from the 2018 level.

Also, it is worth mentioning here that the company is more leveraged than the industry, with respective long-term debt-to-capital ratios of 71.6% and 45.3%.

Stocks That Warrant a Look

Some better-ranked stocks in the industry are Crawford United Corporation CRAWA, Mitsubishi Heavy Industries, Ltd. MHVYF and Kadant Inc. KAI. While Crawford United and Mitsubishi Heavy currently sport a Zacks Rank #1 (Strong Buy), Kadant carries a Zacks Rank #2 (Buy). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Current-year earnings estimates for Crawford United and Kadant have improved in the past 60 days. The same for Mitsubishi Heavy suggests year-over-year growth of 17.2%.

5 Stocks Set to Double

Each was hand-picked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2020. Each comes from a different sector and has unique qualities and catalysts that could fuel exceptional growth.

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>

Want the latest recommendations from Zacks Investment Research? Today, you can download 7 Best Stocks for the Next 30 Days. Click to get this free report

Illinois Tool Works Inc. (ITW) : Free Stock Analysis Report

Kadant Inc (KAI) : Free Stock Analysis Report

Mitsubishi Heavy Industries, Ltd. (MHVYF) : Free Stock Analysis Report

Hickok Inc. (CRAWA) : Free Stock Analysis Report

To read this article on Zacks.com click here.