Yahoo Finance

Yahoo Finance Recent 13% pullback isn't enough to hurt long-term Autolus Therapeutics (NASDAQ:AUTL) shareholders, they're still up 157% over 1 year

Autolus Therapeutics plc (NASDAQ:AUTL) shareholders might be rather concerned because the share price has dropped 33% in the last month. Despite this, the stock is a strong performer over the last year, no doubt about that. During that period, the share price soared a full 157%. So it is important to view the recent reduction in price through that lense. Investors should be wondering whether the business itself has the fundamental value required to continue to drive gains.

While the stock has fallen 13% this week, it's worth focusing on the longer term and seeing if the stocks historical returns have been driven by the underlying fundamentals.

Check out our latest analysis for Autolus Therapeutics

We don't think Autolus Therapeutics' revenue of US$1,698,000 is enough to establish significant demand. So it seems that the investors focused more on what could be, than paying attention to the current revenues (or lack thereof). For example, they may be hoping that Autolus Therapeutics comes up with a great new product, before it runs out of money.

Companies that lack both meaningful revenue and profits are usually considered high risk. We can see that they needed to raise more capital, and took that step recently despite the fact that it would have been dilutive to current holders. While some companies like this go on to deliver on their plan, making good money for shareholders, many end in painful losses and eventual de-listing. Of course, if you time it right, high risk investments like this can really pay off, as Autolus Therapeutics investors might know.

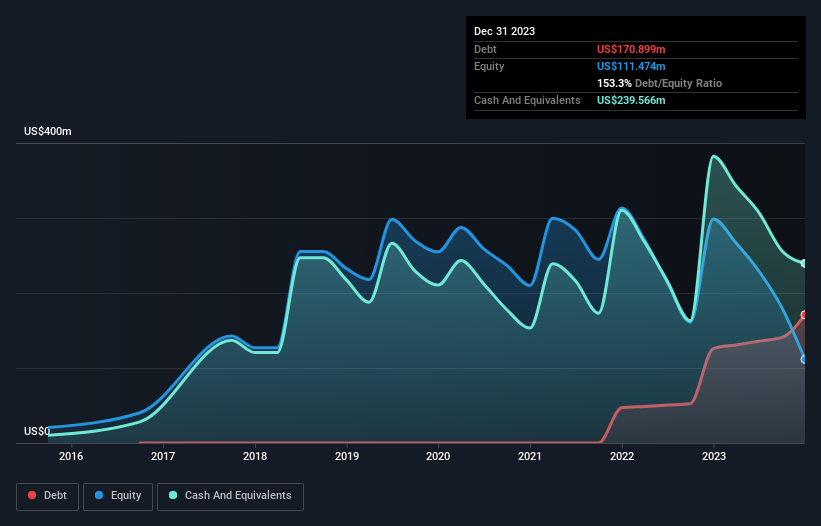

Autolus Therapeutics had liabilities exceeding cash when it last reported, according to our data. That made it extremely high risk, in our view. So the fact that the stock is up 83% in the last year shows that the cash injection was a welcome one. It's clear more than a few people believe in the potential. You can click on the image below to see (in greater detail) how Autolus Therapeutics' cash levels have changed over time.

In reality it's hard to have much certainty when valuing a business that has neither revenue or profit. However you can take a look at whether insiders have been buying up shares. It's usually a positive if they have, as it may indicate they see value in the stock. You can click here to see if there are insiders buying.

A Different Perspective

We're pleased to report that Autolus Therapeutics shareholders have received a total shareholder return of 157% over one year. Notably the five-year annualised TSR loss of 13% per year compares very unfavourably with the recent share price performance. This makes us a little wary, but the business might have turned around its fortunes. While it is well worth considering the different impacts that market conditions can have on the share price, there are other factors that are even more important. Like risks, for instance. Every company has them, and we've spotted 3 warning signs for Autolus Therapeutics (of which 1 is a bit concerning!) you should know about.

Of course Autolus Therapeutics may not be the best stock to buy. So you may wish to see this free collection of growth stocks.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on American exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.