Yahoo Finance

Yahoo Finance Record low interest rates until 2024 could deepen divisions between Australia's haves and have-nots

Super-low interest rates will remain for at least another three years, the Reserve Bank has said, increasing the likelihood of a continued surge in house prices exacerbating what one leading thinktank called the division of Australia into a nation of haves and have-nots.

After the central bank kept rates at the historic low of 0.1% at its monthly policy meeting on Tuesday, its governor, Philip Lowe, said the higher inflation needed to see a rise in rates would not return until “2024 at the earliest”.

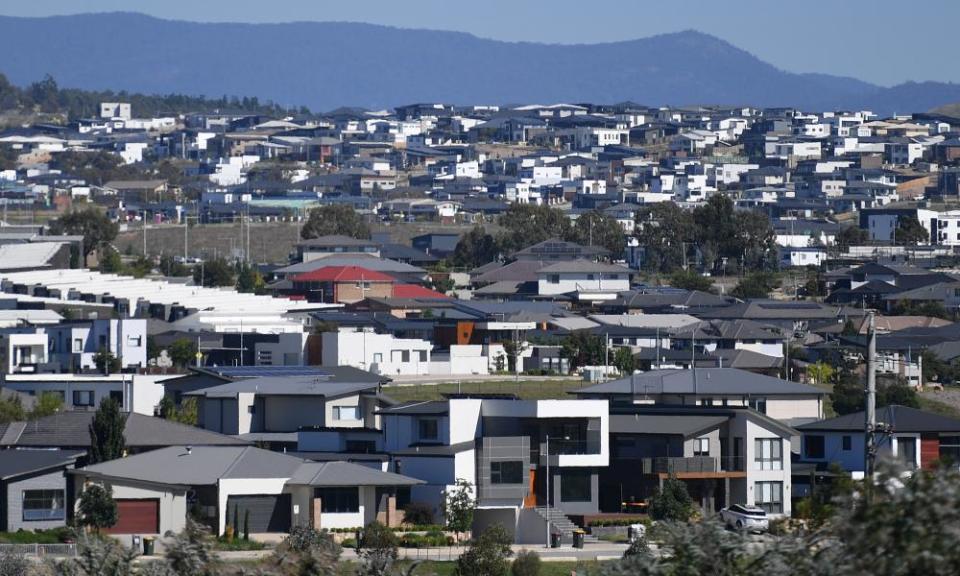

Record low borrowing costs have helped rejuvenate the property market in recent months after prices dropped around 10% at the height of the coronavirus pandemic last year. The research company CoreLogic said on Monday that national average prices rose 2.1% in February, the biggest increase since 2003.

Related: Australian house prices record largest monthly rise in almost two decades

Lowe’s post-meeting statement scotched suggestions in some quarters that the RBA might try to raise rates to dampen what real estate experts have called a “frenzy” in the market.

The governor said cheap borrowing costs were necessary to maintain the economic recovery, and suggested that the “sound” lending standards currently in place would guard against the surge in the property market leading to any financial instability.

“The board will not increase the cash rate until actual inflation is sustainably within the two to three per cent target range,” Lowe said, noting that wages would have to grow and unemployment fall before inflation could increase from its current 0.9%. “The board does not expect these conditions to be met until 2024 at the earliest.”

However, the RBA’s “concrete” guidance was likely to ensure that high house prices remain for the foreseeable future, bringing warnings about rising inequality.

Brendan Coates, the Grattan Institute’s director for household finances, said the biggest driver for prices was that borrowers expected rates to remain low.

The RBA’s own research reckons that a one percentage point reduction in mortgage rates lifts house prices by 28% in the long run. Average rates were around 5% in 2015 but are now around 2.5%.

But Coates warned the lack of affordability in Australia’s housing market meant the country was becoming increasingly divided between the “haves and have-nots”.

“People are being priced out, especially of homes close to jobs and transport,” he said. “If and where you buy a house is increasingly going to depend on who your parents are, because it’s getting to the point where if you don’t have parental financial support you will struggle to buy a house in those areas.”

Rates are not the only factor in rising prices. A shortage of supply has also found buyers scrambling to snap up whatever is being offered for sale. Agents in Sydney are reporting triple the normal amount of inspections and bidders, and in some cases properties going for several hundred thousands dollars above the asking rates.

As frustrated buyers worry about missing out before prices rise out of reach, sales of previously overlooked stock listed for months have also risen, leaving agents unable to keep up with demand.

“We’re in a bit of a frenzy,” says Blake Lowry, a real estate agent at Belle Property in Annandale in Sydney’s inner west. “Buyers are very concerned about prices going up so they are attacking them.”

Related: 'Clean air, an amazing house': pandemic tree-changers grab a slice of the Apple Isle

Owner-occupiers are still “leading the charge” towards higher prices as shown by the latest housing finance figures released by the Australian Bureau of Statistics this week, but investors are returning to the market after a couple of years of subdued activity and are making it even more competitive.

The total value of owner-occupier loans rose 10.9% in January to $22.11bn, which is a rise of 52% on the same time last year. The amount of borrowing arranged by investors did not rise as much but it was still up 9.4% to $6.54bn. That is a 22.7% increase compared with last January and nearly all of that gain has come in the last three months, according to analysis by Westpac.

Ben Udy, Australia economist for the consultancy Capital Economics, said the huge increases in lending, which was particularly pronounced for the purchase of existing rather than new property, came as supply of new housing remained tight. “It shows that there is a great amount of money chasing the same amount of housing. People are willing to pay a bit more.”

The urge not to miss out was a clear driver, according to Louis Christopher, the founder of SQM Research, and demand was simply “swamping” the new listings and eating up old listings as well.

Only a significant negative impact on people’s incomes from the phasing out of the jobkeeper allowance this month stood in the way of prices rising even further he said.

“If the market weathers that, then we might see an intervention by the regulators to curb lending like they did in 2017,” he said. But with the RBA giving lending standards a clean bill of health on Tuesday, there was little sign of intervention by the macro-prudential watchdog, the Australian Prudential and Regulatory Authority. “The market will have a big green light.”