Yahoo Finance

Yahoo Finance Repay Holdings (NASDAQ:RPAY) shareholders have endured a 56% loss from investing in the stock a year ago

While not a mind-blowing move, it is good to see that the Repay Holdings Corporation (NASDAQ:RPAY) share price has gained 18% in the last three months. But that isn't much consolation to those who have suffered through the declines of the last year. Like a receding glacier in a warming world, the share price has melted 56% in that period. The share price recovery is not so impressive when you consider the fall. You could argue that the sell-off was too severe.

Since shareholders are down over the longer term, lets look at the underlying fundamentals over the that time and see if they've been consistent with returns.

Check out our latest analysis for Repay Holdings

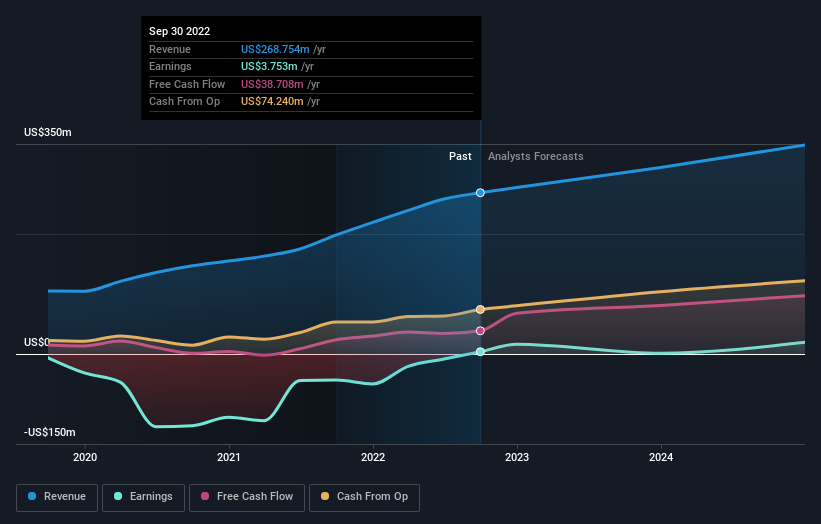

Given that Repay Holdings only made minimal earnings in the last twelve months, we'll focus on revenue to gauge its business development. As a general rule, we think this kind of company is more comparable to loss-making stocks, since the actual profit is so low. For shareholders to have confidence a company will grow profits significantly, it must grow revenue.

In the last year Repay Holdings saw its revenue grow by 35%. That's definitely a respectable growth rate. Unfortunately it seems investors wanted more, because the share price is down 56% in that time. It may well be that the business remains approximately on track, but its revenue growth has simply been delayed. To our minds it isn't enough to just look at revenue, anyway. Always consider when profits will flow.

You can see how earnings and revenue have changed over time in the image below (click on the chart to see the exact values).

It's probably worth noting we've seen significant insider buying in the last quarter, which we consider a positive. On the other hand, we think the revenue and earnings trends are much more meaningful measures of the business. So it makes a lot of sense to check out what analysts think Repay Holdings will earn in the future (free profit forecasts).

A Different Perspective

The last twelve months weren't great for Repay Holdings shares, which performed worse than the market, costing holders 56%. The market shed around 20%, no doubt weighing on the stock price. The three-year loss of 14% per year isn't as bad as the last twelve months, suggesting that the company has not been able to convince the market it has solved its problems. We would be wary of buying into a company with unsolved problems, although some investors will buy into struggling stocks if they believe the price is sufficiently attractive. It's always interesting to track share price performance over the longer term. But to understand Repay Holdings better, we need to consider many other factors. Even so, be aware that Repay Holdings is showing 4 warning signs in our investment analysis , and 3 of those shouldn't be ignored...

Repay Holdings is not the only stock insiders are buying. So take a peek at this free list of growing companies with insider buying.

Please note, the market returns quoted in this article reflect the market weighted average returns of stocks that currently trade on US exchanges.

Have feedback on this article? Concerned about the content? Get in touch with us directly. Alternatively, email editorial-team (at) simplywallst.com.

This article by Simply Wall St is general in nature. We provide commentary based on historical data and analyst forecasts only using an unbiased methodology and our articles are not intended to be financial advice. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. We aim to bring you long-term focused analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Simply Wall St has no position in any stocks mentioned.

Join A Paid User Research Session

You’ll receive a US$30 Amazon Gift card for 1 hour of your time while helping us build better investing tools for the individual investors like yourself. Sign up here