Yahoo Finance

Yahoo Finance Is Residential Secure Income plc (LON:RESI) At Risk Of Cutting Its Dividend?

Today we'll take a closer look at Residential Secure Income plc (LON:RESI) from a dividend investor's perspective. Owning a strong business and reinvesting the dividends is widely seen as an attractive way of growing your wealth. Yet sometimes, investors buy a popular dividend stock because of its yield, and then lose money if the company's dividend doesn't live up to expectations.

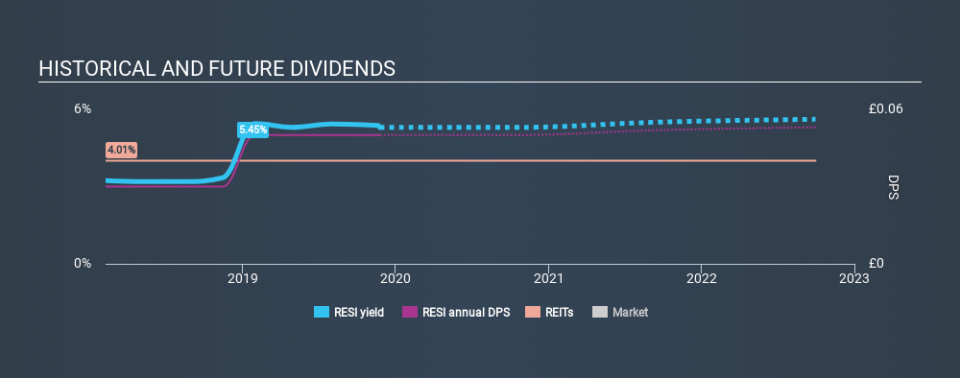

Residential Secure Income yields a solid 5.3%, although it has only been paying for two years. A 5.3% yield does look good. Could the short payment history hint at future dividend growth? During the year, the company also conducted a buyback equivalent to around 2.4% of its market capitalisation. There are a few simple ways to reduce the risks of buying Residential Secure Income for its dividend, and we'll go through these below.

Explore this interactive chart for our latest analysis on Residential Secure Income!

Payout ratios

Companies (usually) pay dividends out of their earnings. If a company is paying more than it earns, the dividend might have to be cut. So we need to form a view on if a company's dividend is sustainable, relative to its net profit after tax. Looking at the data, we can see that 118% of Residential Secure Income's profits were paid out as dividends in the last 12 months. A payout ratio above 100% is definitely an item of concern, unless there are some other circumstances that would justify it.

Another important check we do is to see if the free cash flow generated is sufficient to pay the dividend. With a cash payout ratio of 118%, Residential Secure Income's dividend payments are poorly covered by cash flow. Cash is slightly more important than profit from a dividend perspective, but given Residential Secure Income's payouts were not well covered by either earnings or cash flow, we would definitely be concerned about the sustainability of this dividend.

It is worth considering that Residential Secure Income is a Real Estate Investment Trust (REIT). REITs have different rules governing their payments, and are often required to pay out a high portion of their earnings to investors.

We update our data on Residential Secure Income every 24 hours, so you can always get our latest analysis of its financial health, here.

Dividend Volatility

One of the major risks of relying on dividend income, is the potential for a company to struggle financially and cut its dividend. Not only is your income cut, but the value of your investment declines as well - nasty. The dividend has not fluctuated much, but with a relatively short payment history, we can't be sure this is sustainable across a full market cycle. During the past two-year period, the first annual payment was UK£0.03 in 2017, compared to UK£0.05 last year. Dividends per share have grown at approximately 29% per year over this time.

The dividend has been growing pretty quickly, which could be enough to get us interested even though the dividend history is relatively short. Further research may be warranted.

Dividend Growth Potential

Dividend payments have been consistent over the past few years, but we should always check if earnings per share (EPS) are growing, as this will help maintain the purchasing power of the dividend. Residential Secure Income's earnings per share are up 7.0% on last year. It's good to see earnings per share rising, but one year is too short a period to get excited about. Were this trend to continue, we'd be interested. Although per-share earnings are growing at a credible rate, virtually all of the income is being paid out as dividends to shareholders. This is okay, but may limit growth in the company's future dividend payments. We do note though, one year is too short a time to be drawing strong conclusions about a company's future prospects.

Conclusion

When we look at a dividend stock, we need to form a judgement on whether the dividend will grow, if the company is able to maintain it in a wide range of economic circumstances, and if the dividend payout is sustainable. Residential Secure Income paid out almost all of its cash flow and profit as dividends, leaving little to reinvest in the business. Second, earnings growth has been ordinary, and its history of dividend payments is shorter than we'd like. There are a few too many issues for us to get comfortable with Residential Secure Income from a dividend perspective. Businesses can change, but we would struggle to identify why an investor should rely on this stock for their income.

Are management backing themselves to deliver performance? Check their shareholdings in Residential Secure Income in our latest insider ownership analysis.

Looking for more high-yielding dividend ideas? Try our curated list of dividend stocks with a yield above 3%.

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.