Yahoo Finance

Yahoo Finance Saga plc (LON:SAGA) Just Reported Earnings, And Analysts Cut Their Target Price

As you might know, Saga plc (LON:SAGA) recently reported its yearly numbers. It was an okay result overall, with revenues coming in at UK£799m, roughly what the analysts had been expecting. Earnings are an important time for investors, as they can track a company's performance, look at what the analysts are forecasting for next year, and see if there's been a change in sentiment towards the company. We've gathered the most recent statutory forecasts to see whether the analysts have changed their earnings models, following these results.

See our latest analysis for Saga

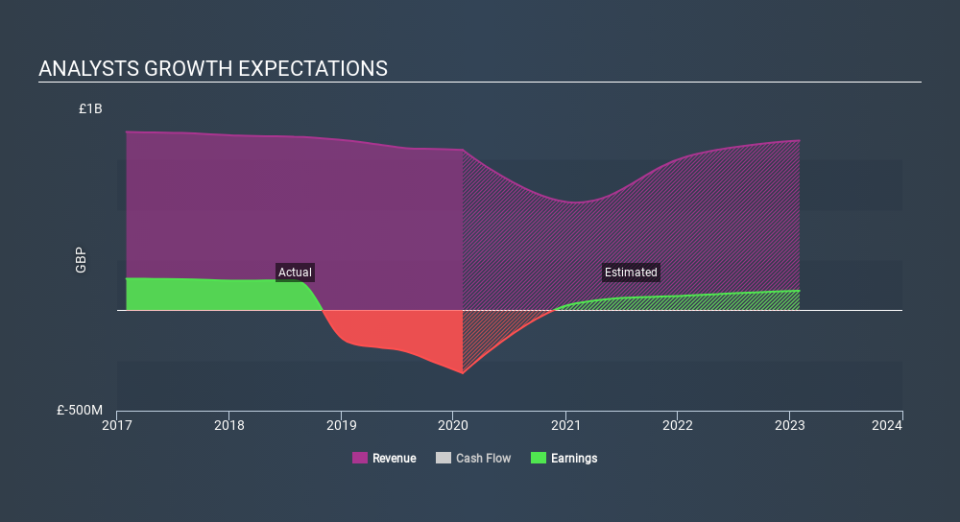

Following the recent earnings report, the consensus from three analysts covering Saga is for revenues of UK£535.8m in 2021, implying a substantial 33% decline in sales compared to the last 12 months. Saga is also expected to turn profitable, with statutory earnings of UK£0.03 per share. In the lead-up to this report, the analysts had been modelling revenues of UK£514.4m and earnings per share (EPS) of UK£0.035 in 2021. So it's pretty clear the analysts have mixed opinions on Saga after the latest results; even though they upped their revenue numbers, it came at the cost of a real cut to per-share earnings expectations.

The consensus price target fell 12% to UK£0.39, suggesting that the analysts are primarily focused on earnings as the driver of value for this business. Fixating on a single price target can be unwise though, since the consensus target is effectively the average of analyst price targets. As a result, some investors like to look at the range of estimates to see if there are any diverging opinions on the company's valuation. The most optimistic Saga analyst has a price target of UK£0.55 per share, while the most pessimistic values it at UK£0.19. Note the wide gap in analyst price targets? This implies to us that there is a fairly broad range of possible scenarios for the underlying business.

Of course, another way to look at these forecasts is to place them into context against the industry itself. By contrast, our data suggests that other companies (with analyst coverage) in the industry are forecast to see their revenue shrink 16% per year. While this is interesting, Saga's, revenues are still expected to shrink next year, and at a faster rate than the wider industry.

The Bottom Line

The biggest concern is that the analysts reduced their earnings per share estimates, suggesting business headwinds could lay ahead for Saga. They also upgraded their revenue estimates, with sales apparently performing well, although revenues are expected to lag the wider industry this year. The consensus price target fell measurably, with the analysts seemingly not reassured by the latest results, leading to a lower estimate of Saga's future valuation.

With that said, the long-term trajectory of the company's earnings is a lot more important than next year. We have estimates - from multiple Saga analysts - going out to 2023, and you can see them free on our platform here.

Plus, you should also learn about the 2 warning signs we've spotted with Saga (including 1 which is a bit concerning) .

If you spot an error that warrants correction, please contact the editor at editorial-team@simplywallst.com. This article by Simply Wall St is general in nature. It does not constitute a recommendation to buy or sell any stock, and does not take account of your objectives, or your financial situation. Simply Wall St has no position in the stocks mentioned.

We aim to bring you long-term focused research analysis driven by fundamental data. Note that our analysis may not factor in the latest price-sensitive company announcements or qualitative material. Thank you for reading.